A vertical spread is an options trading strategy that involves the simultaneous buying and selling of two options of the same underlying asset and expiration date but at different strike prices. The vertical spread’s goal is to profit from the difference in premiums between the two options while limiting risk.

There are two main types of vertical spreads: bull call spreads and bear put spreads. A bull call spread involves buying a call option with a lower strike and selling a call with a higher strike. It profits if the underlying stock rises in price. A bear put spread involves buying a put with a higher strike and selling a put with a lower strike. It profits if the underlying stock falls in price.

Vertical spreads have defined and limited risk/reward characteristics. The maximum loss is limited to the net premium paid for the two options, and the maximum gain is capped at the difference between the strike prices less the net premium paid. Traders utilize vertical spreads to take directional views on stocks while reducing cost and capping risk compared to buying options outright. It defines profit zones while minimizing capital outlay.

Key benefits of trading vertical spreads include reduced upfront costs compared to buying single options, defined and limited risk, the ability to profit from moderate moves in the underlying stock, and higher leverage than trading the stock itself. Downsides include limited profit potential capped by the difference in strikes and a more complex structure than simply trading stock or individual options. Overall, vertical spreads allow traders to implement risk-defined directional option strategies.

What are Vertical Spreads?

A vertical spread is an options trading strategy that involves the simultaneous buying and selling of two options of the same underlying security with the same expiration date but at different strike prices. The options are calls or puts, depending on the market outlook and goals of the options trader. The simultaneity of buying and selling puts this strategy in the class of spreads, which combine both long and short option positions to form a single trade.

The “vertical” descriptor refers to the fact that the options have different strikes but the same expiration date so that a profit graph would show the gain or loss within a defined vertical range on the graph. This differs from horizontal spreads, where the options have the same strike but different expirations, creating a horizontal profit/loss zone. Vertical spreads limit both risk and reward between the strike prices involved.

For calls, a vertical spread is created by buying a call option with a lower strike price while simultaneously selling a call with a higher strike. This is known as a bull call spread since maximum profit is attained when the underlying security rises in price. For puts, a vertical spread entails buying a put at a higher strike while selling a put at a lower strike, termed a bear put spread, since it profits when the underlying security falls in price.

Traders utilize vertical spreads to speculate on price moves in the underlying security while strictly defining both risk and profit potential. By combining the purchase and sale of options at different strikes, the cost outlay is lowered, and the loss amount is reduced if the underlying fails to move as anticipated. The defined maximum gain is also capped at the difference between the strike prices.

The spread limits risk due to the locked-in net credit or debit taken when initiating the trade. For bull call spreads, there is a net debit paid, and the maximum loss is that amount. Forbear put spreads, there is a net credit gained, and the loss is no more than the difference between strike prices and the initial credit. The difference between strikes for either spread type also defines gains.

Reasons traders implement vertical spreads include directional speculation, reduced cost and lower capital requirements compared to buying options outright, risk management by capping loss, and leveraged profit potential compared to just trading the underlying security. The trade-off is limited upside versus just buying a single option. Vertical spreads allow precision in risk-reward profiling.

How do Vertical Spreads work?

Vertical spreads work by combining the purchase and sale of calls or put at different strike prices to both lower the cost of entry and precisely define the maximum potential profit or loss. Traders deploy these spreads when expecting moderate, directional moves in the underlying asset rather than substantial trending price action. The simultaneous long and short options positions reduce upfront capital requirements while capping risk and reward.

Bull call spreads work when the trader forecasts a moderate upside in the underlying asset. They buy a lower strike call to benefit from rising prices. But to offset the cost, they simultaneously sell a higher strike call to collect premium income, limiting gains if the stock rises beyond that upper strike. The maximum loss is the net debit paid if shares stay below the long call strike. Profits accrue up to the difference between strikes.

Bear put spreads work when the trader expects a moderate downside in the underlying asset. They buy a higher strike to benefit from falling prices. But to reduce cost, they simultaneously sell a lower strike put to collect premium income, capping gains if the stock drops below that lower strike. The maximum loss is now the difference between strikes less the initial net credit received. Gains accrue up to that defined spread between strikes.

Traders use vertical spreads when anticipating directional moves in the underlying price rather than major trending price action. The sale of the secondary option reduces cost and risk but limits profit potential versus buying a single option outright. This structure exchanges defined, capped gains for lower capital needs and risk control.

For either spread type, the trader’s account sees a net credit or debit based on the premiums of the long and short legs. Often, the short-sold option heavily offsets the cost of the long option purchase, resulting in a net credit received for the spread. This lowers capital requirements but caps the upside at the difference between the long and short strikes.

Vertical spreads allow traders to implement risk-defined directional options strategies with lower cost and capped risk compared to naked long calls or puts. The maximum gain and loss are clearly defined based on the strikes chosen relative to the current price of the underlying asset. The upside is limited, but capital needs and risk decreases.

What is the importance of Vertical Spreads in Options Trading?

Vertical spreads are important in options trading because they allow traders to take directional views on underlying securities while precisely defining risk and reward. By combining long and short positions, capital requirements are reduced, and traders implement strategies with a favorable risk-reward asymmetry. The simultaneous long and short options structure is key to both lowering cost and capping the maximum potential loss.

Buying calls or puts outright exposes the trader to substantial risk if the anticipated price move in the underlying does not materialize prior to option expiration. However, with vertical spreads, the sale of a secondary option against the primary position limits risk. While the upside is also capped, the cost savings and risk reduction make vertical spreads an essential component of prudent options trading.

For example, a bull call vertical spread allows participation in upside price action while strictly defining maximum loss if the underlying security fails to rally sufficiently. The short call strike caps gains but also lowers the debit required to establish the trade. The maximum risk is quantified at the outset. Without the short call, potential losses on just the long call purchase are unlimited if the rally does not occur.

Similarly, a bear put vertical spread allows the trader to benefit from the downside with risk strictly capped by the difference between the strike prices. The sale of the lower strike put offsets the cost of the primary higher strike put while also defining the maximum loss if shares do not fall as anticipated. Buying the put alone leaves risk undefined.

Beyond risk management, the net credit or debit taken when initiating the trade has implications for capital efficiency. Often, the short call or put heavily subsidizes the cost of the primary long position call or put. This means the required outlay is lowered substantially compared to outright long calls or puts. Lower capital requirements allow trading larger size and diversification.

Vertical spreads also allow traders to implement contingent orders for risk control. For example, a bear put spread is legged into initially selling a put and then waiting to buy the higher strike put when the underlying security declines to a specified level. This structure further optimizes the risk-reward scenario.

What are the 4 Basic types of Vertical Spreads?

The four basic types of vertical spreads are the Bull Call Spread, Bear Put Spread, Bull Put Spread, and Bear Call Spread. Below are more details

1.Bull Call Spread

A bull call spread is a vertical spread strategy used when a moderate rise in the underlying asset is expected. It involves buying a call option at a lower strike price and selling a call option at a higher strike price, both with the same expiration date.

The profit potential is limited to the difference between the strike prices minus the net debit paid to open the position. The maximum loss is capped at the net debit if the underlying asset finishes below the long call strike at expiration. This strategy offers leveraged upside exposure with reduced cost and defined risk versus buying a call alone.

To implement a bull call spread, the trader buys a lower strike call and sells a higher strike call, collecting a net credit that lowers the cost basis. The trade profits if the asset price rises above the breakeven point up to the short-call strike. This strategy carries maximum risk if the asset finishes below the long call strike at expiration.

Key calculations for a bull call spread include determining the maximum profit, maximum loss, and breakeven point and assessing the risk-reward profile. For example, buying the Rs.30 call and selling the Rs.35 call for a net debit of Rs.2.00 would have a maximum profit of Rs.3.00 if shares finish above Rs.35 at expiration. The maximum loss is the Rs.2.00 debit paid.

2. Bear Put Spread

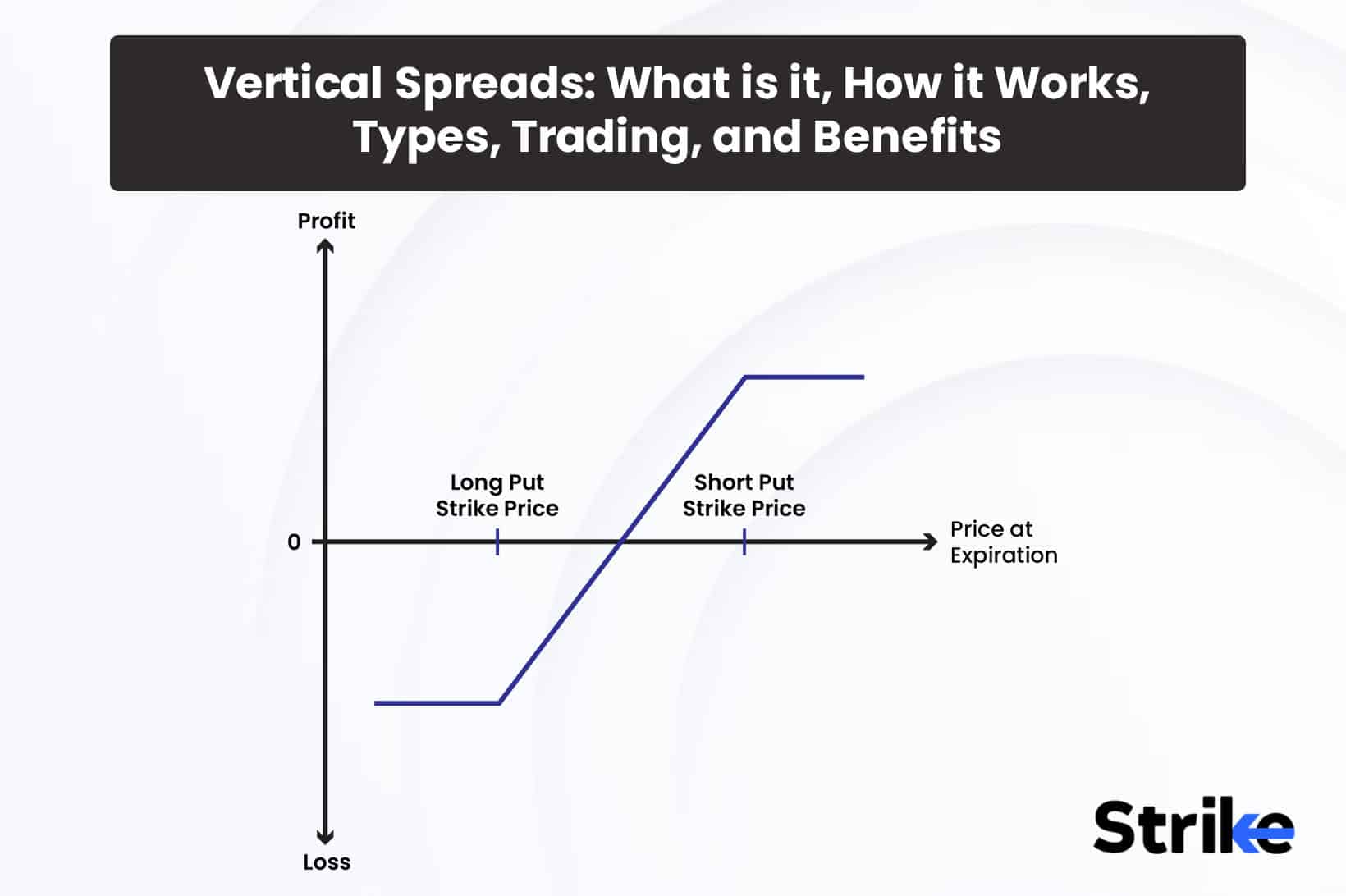

A bear put spread is a vertical spread strategy used when a moderate decline in the underlying asset is expected. It involves buying a put option at a higher strike price while selling a put option at a lower strike price, both with the same expiration.

The maximum profit is limited to the difference between the strike prices minus the initial net credit received. The maximum loss is defined as the difference between the strike prices if the underlying asset finishes above the short put strike at expiry. This structure provides leveraged downside exposure with reduced cost and capped risk versus just buying a put.

To implement a bear put spread, the trader sells a lower strike put and buys a higher strike put, collecting a net credit which lowers the cost basis. The trade profits if the asset price falls below the breakeven point down to the long put strike. The maximum risk is if the asset stays above the short put strike at expiration.

Key calculations for a bear put spread include determining the maximum profit, maximum loss, breakeven point, and assessing the risk-reward asymmetry. For example, selling the Rs.30 put and buying the Rs.25 put for a net credit of Rs.2.00 would create a maximum profit of Rs.3.00 if shares drop below Rs.25 at expiration. The maximum loss is Rs.3.00 if shares are above Rs.30 at expiry.

3. Bull Put Spread

A bull put spread is a vertical spread strategy used when a moderate rise in the underlying asset is expected. It entails buying a put option at a lower strike and selling a put at a higher strike, both with the same expiration date.

The maximum profit is limited to the net credit received at the outset. The maximum loss is defined as the difference between the strike prices minus the initial credit if the asset finishes below the long put strike price at expiration. This structure offers leveraged upside with reduced cost and capped downside risk.

To implement a bull put spread, the trader sells a higher strike put and buys a lower strike put, collecting a net credit which lowers the cost basis. The trade profits if the asset price rises above the breakeven point up to the short put strike at expiry. The maximum risk is if the asset drops below the long put strike price.

Key calculations for a bull put spread include assessing the maximum profit, maximum loss, breakeven point, and overall risk-reward scenario. For example, selling the Rs.35 put and buying the Rs.30 put for a net credit of Rs.2.00 would create a maximum profit of Rs.2.00 if shares are above Rs.35 at expiration. The maximum loss is Rs.3.00 if shares fall below Rs.30.

4. Bear Call Spread

A bear call spread entails buying a call option at a higher strike price while selling a call option at a lower strike, both with the same expiration date. It is used when a moderate decline in the underlying asset is expected.

The maximum profit is limited to the net credit received at the outset. The maximum loss is defined as the difference between strike prices minus the initial credit if the asset finishes above the short call strike at expiration. This structure provides leveraged downside exposure with reduced cost and quantified risk parameters.

To implement a bear call spread, the trader sells a lower strike call and buys a higher strike call, collecting a net credit, which lowers the cost basis. The trade profits if the asset price falls below the breakeven point down to the long call strike by expiration. The maximum risk is if the asset rises above the short call strike at expiry.

Key calculations include assessing the maximum profit, maximum loss, breakeven point, and overall risk-reward profile. For example, selling the Rs.30 call and buying the Rs.35 call for a net credit of Rs.2.00 would produce a maximum profit of Rs.2.00 if shares are below Rs.30 at expiration. The maximum loss is Rs.3.00 if shares rise above Rs.35.

What are the factors to consider when trading Vertical Spreads?

Traders must evaluate factors related to risk management, profit potential, probability, cost of entry, and expiration mechanics when assessing potential vertical spread trades. The most critical considerations include the below seven.

1. Risk-Reward Profile

The risk-reward profile is foundational when considering vertical spreads. The maximum potential gain and loss are predefined based on the strikes chosen relative to the current underlying price. Analyze the upside profit potential versus the maximum loss amount to ensure agreeable asymmetry. Favor spreads with a larger profit upside versus the capital at risk.

2. Probability of Profit

The statistical probability of achieving a successful profit by option expiration is critical. Assess the chance the underlying finishes within the strike prices are based on volatility. A high probability of exceeding the breakeven intrinsic value improves the statistical edge. Probability analysis informs whether the structure aligns with the directional forecast.

3. Cost of Entry

The net debit or credit taken when initiating the spread has implications for both loss exposure and potential return on capital. The total cost in relation to maximum profit provides guidance on upside versus capital risk. Lower cost basis spreads allow higher leverage and return potential but define risk taken.

4. Implied Volatility

Implied volatility impacts options pricing and probabilities. Analyze IV levels on the spread strikes to identify mispricings to exploit. IV skews between strike prices widen spreads artificially. A lower IV on spread entry is preferable for clearly defined risk profiles. Monitor for IV spikes that alter the outlook.

5. Time Decay Dynamics

Time decay behavior affects options pricing over the life of the trade. The arc of time value erosion impacts profit potential. Analyze time decay between the spread strikes and favor those providing advantage related to the forecasted move and expiration.

6. Early Exercise Risk

Early option exercise alters vertical spread profits if the short leg is assigned before expiration. Assess the dividend schedule and interest rates to gauge early exercise risk on the short call or put. Avoid spread structures with heightened early assignment risk.

7. Liquidity Considerations

The ability to efficiently enter and exit positions is key. Evaluate open interest and bid-ask spreads at the strikes considered to ensure adequate liquidity exists, especially on the short strike. More liquidity raises trading costs and impedes managing trades.

Analyzing risk metrics, probability of profit, cost basis, volatility, time decay, early exercise risk, and liquidity provides the quantitative framework for identifying optimal vertical spread trading opportunities across potential market scenarios. These factors help traders deploy these structures with precision and alignment to their market outlook.

Do you need a margin for Vertical Spreads?

Yes, vertical spreads do require a margin account and are subject to margin requirements. Vertical spreads involve both buying and short-selling options, so they cannot be traded in a cash account and require a margin account. However, the short-sold option acts as collateral for the long-purchased option, so a regulatory margin is only required on the net difference between the long and short strike prices.

This means lower margin requirements than buying or selling options outright. The maximum margin is the difference between the strikes minus any net credit received. So verticals allow options leverage with lower capital at risk versus naked options.

When to close Vertical Spreads?

Determining the optimal time to close is a key but complex consideration when trading vertical spreads. While many traders hold spreads to expiration to maximize profits, early exits are often prudent to capture gains, limit losses, or adjust to changing conditions. Closing spreads before expiry involves balancing upside potential versus risk management.

The simplest exit strategy is holding verticals until expiration, letting time decay fully erode the remaining premium to realize the maximum possible profit. However, closing positions ahead of expiry allows for locking in profits and avoiding unforeseen events that could erase gains prior to expiration. Potential reasons to exit early include the spread hitting its maximum profit target, the underlying price moving adversely, implied volatility spiking, liquidity drying up, upcoming dividends or corporate actions altering the outlook, or new information causing a forecast change.

Traders employ quantitative and qualitative triggers to optimize early closure timing. Price targets involve closing when the underlying asset hits pre-determined levels based on technical or fundamental analysis. Technical indicators like moving average crossovers or overbought/oversold conditions also prompt early exits. Closing at a target percentage of maximum profit, such as 75%, allows banking most upside before time remaining introduces volatility risk. Specifying days to expiration thresholds for closing lock-in gains as time value decays. Changes in implied volatility are also used, exiting on extreme IV expansion or contraction.

The decision to close spreads early requires balancing risk versus reward. Traders aim to capture sufficient profit while also protecting capital from adverse developments prior to expiration. Both quantitative rules and qualitative assessments of changing conditions are utilized to maximize returns and minimize late surprises. Determining optimal early closure timing is a nuanced but critical aspect of trading vertical spreads.

When to roll a Vertical Spreads?

Rolling or adjusting vertical spreads involves closing the current position and opening a new spread for a credit or debit while maintaining market exposure. Traders roll verticals when the existing spread structure is compromised or suboptimal, given changing market conditions. Reasons include the underlying price moving out of the profit zone, upcoming dividends or earnings, time decay effects, and volatility shifts.

Rolling to a different strike profile allows for maintaining the directional outlook while adjusting the risk-reward scenario. This may entail rolling up the short strike for more upside potential while risking additional premium. Rolling down the long strike brings in credit while defining a new loss limit. Adjusting one or both strikes adapts the position for the new price range or outlook.

Rolling to a further expiration date is done to maintain directional Exposure when more time is needed. This may involve closing spreads nearing expiry and opening new ones several months out. Traders roll to later expiries when the price action has not developed as anticipated, but more time could see the move occur.

Rolling for a credit involves closing the current spread and opening a new one where the credit received exceeds the prior debit, lowering the cost basis. Collecting a net credit when rolling adjusts the risk profile favorably by reducing the maximum loss amount. The new position has lower breakeven points.

Volatility changes often necessitate adjustments. Rolling when implied volatility declines allow selling expensive options and replacing them with lower valued positions efficiently. When volatility spikes, upside Exposure is maintained while capturing inflated credit from elevated premiums.

Upcoming earnings releases, economic data, or other news events bring uncertainty that impacts spreads. Rolling to later expiries after the event risk passes allows maintaining directional Exposure under a clearer outlook. The new position has a higher probability of profitability.

Are Vertical Spreads profitable?

Yes, Vertical spreads are profitable trading strategies when used properly, but they do not guarantee profits. Their main advantage is defining risk, so losses are limited to the debit paid or difference between strike prices while maintaining leveraged Exposure to directional moves.

However, vertical spreads cap the profit potential at a distance between the long and short strikes, so while they limit risk, the upside is also limited.

What is the best way to trade Vertical Spreads?

The best way to trade vertical spread is through proper position sizing. It is critical when trading vertical spreads. Since defined-risk vertical spreads cap both your maximum profit and loss, you will be able to calculate your risk/reward ratio for each trade. Most experts recommend risking at most 1-2 % of your account on any single vertical spread trade. This ensures you have capital left to continue trading if the trade moves against you. Trade small enough so that a string of losing trades won’t cripple your account.

With vertical spreads, time decay works in your favor. The ideal scenario is for the underlying asset to move towards your target price as expiration approaches. Give yourself enough time to be right by selling options with at least 45 days until expiration. 30-60 days until expiration is generally optimal. Avoid weekly options that decay too fast. Giving yourself time allows the intrinsic value of the options to increase in your favor.

To maximize returns, have a plan in place to take profits at 50% of the maximum gain. For example, if you collected Rs.1 credit on a vertical spread, look to close at Rs.0.50. Managing winners at 50% helps lock in profits and frees up capital for additional trades. You worked hard to get the trade right, so take advantage when it moves in your favor.

Be sure to close out losing vertical spread before expiration. If a trade has moved close to your maximum loss around the 14-day expiration mark, close it out. Holding to expiration exposes you to assignment risk, and the chances of the trade reversing back in your favor are slim at that point. Take the small loss and free up that capital to put into a new trade with a better probability of success.

On vertical spread that drops value after entry, you will be able to “leg in” to the untested side of the trade to reduce your cost basis. For example, if you sold a call vertical for a Rs.1 credit initially, you will be able to buy the lower strike call if the spread value drops to Rs.0.50. Now your cost basis is only Rs.0.50 instead of Rs.1, giving the trade a better chance to profit.

Vertical spreads rely on high-probability trading setups. Delta of 20 or less on the short strike for bull call spreads or delta of 20 or greater on the short strike for bear put spreads. This indicates a 70% or greater chance the short strike will expire out of the money. Additionally, look for an attractive risk/reward ratio of at least 1:1.5.

What are the benefits of Vertical Spreads?

Benefits of vertical spreads include defined and limited risk, margin efficiencies, high probability of profit, time decay advantages, flexibility across market environments, and ease of management throughout the trade.

1. Defined and Limited Risk

The main advantage of vertical spreads is that they offer defined and capped risk. Maximum loss is limited to the net premium paid for the spread. This allows you to precisely calculate your potential risk/reward before entering the trade. With naked options, the risk is undefined and potentially unlimited. With verticals, you know the maximum downside ahead of time. This helps limit losses and promotes better risk management.

2. Margin Efficiencies

Vertical spreads require significantly lower margins compared to naked options plays. Rather than posting the full margin requirement on each leg, the net margin considers the offsetting nature of the long/short strikes. The reduced margin allows you to hold more contracts and diversify across multiple positions. More capital efficiency means better leverage for your trading account.

3. Higher Probability of Profit

Properly structured vertical spreads have a high statistical chance of earning credit or profit at expiration. Since you are combining a short option that expires worthless with a long option to hedge, market movement only has to be moderate to gain an advantage. The probability of profitability typically exceeds 70-80% on verticals. Much better odds than 50/50 naked options.

4. Time Decay Advantages

Vertical spreads take advantage of time decay as the options move closer to expiration. The goal is for the short option to expire worthless so the intrinsic value of the long option is retained as profit. The defined window before expiration allows time premium erosion to work in your favor compared to naked long options.

5. Requires Less Direction Precision

You don’t need perfect timing or precise directional forecasts to profit from vertical spreads. As long as the underlying stays between the spread strike at expiration, the short leg expires worthless for maximal gain. Only requires a moderate move or stagnant price action. It’s easier than predicting major breakouts and outsized swings.

6. Flexibility in Market Environments

Verticals are tailored to bullish, bearish, or neutral market conditions. Call verticals for bullish outlooks, put verticals for bearish, and iron condors/butterflies for range-bound. Provides multiple strategies to adapt to shifting market conditions and volatility regimes.

7. Better Leverage Than Cash Instruments

The outlay to control 100 shares of stock buy several vertical contracts controlling hundreds of shares. This provides greater upside leverage for the same dollar amount invested. With options, you gain big-picture Exposure with smaller account balances.

8. Easy to Adjust and Manage

Verticals have built-in adjustments to defend and manage the position. You are able to roll, widen/tighten the strikes, or leg into the untested side to alter risk/reward. It is much easier to adapt verticals to changing conditions than naked long options. The flexibility helps protect profits and repair losing trades.

A properly constructed vertical spread combines the power of options with carefully managed risks and high reward potential. Learning to trade verticals effectively boosts performance and consistency for options traders.

What are the risks of Vertical Spreads?

While vertical spreads cap risk, they also limit reward. Assignment/exercise risks remain, bid-ask slippage is sometimes problematic, time decay accelerates, volatility changes have a magnified impact, and constant monitoring is imperative.

1. Capped Profit Potential

While vertical spreads limit downside risk, they also cap upside profit potential. Maximum gain is limited to the net premium received at the trade’s inception. Even if the underlying asset price surges past the upper strike price, no additional profits are made. The built-in hedge from the long leg means a missed opportunity if the move is larger than anticipated.

2. Assignment and Exercise Risk

While unlikely, early assignment of the short option leg is possible before expiration if the option goes deep in the money. This leads to early unwinding of the spread at undesirable prices. Additionally, spreads left unmanaged into expiration week face greater exercise and assignment risk. Pay close attention to option settlement procedures to avoid surprises.

3. Bid-Ask Spread Slippage

Entering and exiting vertical spreads requires careful attention to bid-ask spreads. If the spread between the bid and ask price is too wide, excessive slippage on each leg significantly reduces the net credit received. Illiquid options with wide markets make verticals less advantageous. Slippage turns an intended credit into a debit.

4. Implied Volatility Changes

Since vertical spreads contain both long and short vega, changes in implied volatility reduce profits or increase losses. Volatility expansion benefits naked long option positions and hurts short options. Monitor shifts in implied volatility across different expirations and adjust position sizing accordingly.

5. Time Decay Acceleration

While vertical spreads benefit from time decay as expiration approaches, the effect accelerates rapidly in the last 30 days. This works against you if the underlying price trend changes direction late in the trade. Rollover or early unwinding may be required to mitigate accelerating time decay risk.

In addition to these major risks, there are other subtle challenges to effectively trading vertical spreads, like legging into spreads requires diligent tracking of entry and exit prices. Entering each leg separately raises execution concerns. Dividends and stock splits on the underlying asset alter expected outcomes. Plan adjustments around these events. Close monitoring is required as the trade moves closer to expiration. Active management may be needed to avoid exercise.

Weighing these risks against the advantages allows traders to deploy verticals successfully and manage their downsides. Astute risk control is vital to capture the benefits of vertical spread trading effectively.

Are Vertical Spreads Safe?

Yes, Vertical spreads are considered safe options trading strategies since they have defined and capped risk. The maximum loss is limited to the net debit or premium paid to open the vertical spread. This known and finite risk makes verticals safer than trading naked options, which have an unlimited downside. However, risks still exist, so proper position sizing and management are crucial.

Are Vertical Spreads worth it?

Yes, vertical spreads are generally worth trading because they limit downside risk while still allowing for upside profits. The high probability nature of verticals, when structured properly, also makes them attractive. The combined benefits of defined risk, margin efficiency, time decay advantages, and ease of management typically make vertical spreads a worthwhile options strategy.

Is a Vertical Spread the same as a Debit Spread?

Yes, a vertical spread and a debit spread are the same thing. They both involve the simultaneous purchase and sale of two calls or two puts on the same underlying with the same expiration but different strike prices. A net debit is paid to enter the spread position when the long option premium is more than the short option premium.

Is a Vertical spread bullish or bearish?

A vertical spread is structured to be either bullish or bearish. A call credit spread is bullish because you want the underlying price to rise. A put credit spread is bearish because you want the underlying price to fall. Debit spreads are directionally opposite – call debit spreads are bearish, while put debit spreads are bullish.

What is the difference between Vertical Spread and Iron Condor?

The most basic difference between vertical spreads and iron condors lies in how the options positions are constructed. A vertical spread involves buying and selling the same type of options (either calls or puts) on the same underlying asset. It combines one long strike and one short strike of the same option class.

An iron condor utilizes both calls and puts to create a position. It combines a bull put spread with a bear call spread on the same underlying. So, you are trading two different option classes simultaneously. The iron condor has four legs – a long and short put plus a long and short call.

The vertical spread is simpler with just a two-legged long/short position in calls or puts. The iron condor is more complex, with four separate option legs spanning calls and puts.

Vertical spreads have an asymmetrical risk profile, with maximum loss limited to the net premium paid. The upside profit potential is also capped at the credit or debit amount. There is a fixed margin requirement based on the individual broker.

Iron condors express market neutrality with a symmetrical risk profile. Maximum loss is defined on both sides, providing two profit windows. The iron condor requires posting margins on both the put and call verticals separately.

An iron condor presents a higher margin requirement and wider double-capped risk parameters. The vertical spread has single-sided capped risk and lower margin impact.

A vertical spread reaches max profit if the underlying price is above the short strike at expiration for calls or below the short strike for puts. It has a directional profit zone on only one side of the market.

Iron condors achieve maximum profit if the underlying price closes between the short strikes at expiration. So, the profit zone is dual-sided, bounded on either end by the short strikes. It benefits from range-bound rather than directional price action.

A vertical spread has a single-sided profit target, while the iron condor profits from prices between its two short strikes.

Vertical spreads have a directional bias depending on the positioning of the long/short strikes. Call verticals are bullish; put verticals bearish. Positioning determines the market outlook.

Iron condors are market-neutral with a non-directional bias. The short call and put strikes are equidistant from the current price. Their symmetry removes any directional tilt; the iron condor aims to profit from a lack of major price change.

Depending on positioning, vertical spreads have positive or negative values for the Greeks. Call verticals will show positive delta and negative theta, for example. The Greeks depend on the strikes chosen.

Iron condors express neutral values on the Greeks. The positive and negative deltas, gammas, theta, etc., offset each other, summing to values close to zero. This Greek profile matches the non-directional positioning.

Verticals are more actively traded, taking advantage of shorter time frames like daily or weekly options expirations. Their directional nature suits different bias positioning.

Iron condors are held for longer periods to allow the dual profit zones to work. They rely on time decay over months, not weeks. The structure suits passive position holding, not active trading.

Previous Article

Previous Article

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 64")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 65")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 66")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 70")

No Comments Yet.