The Last In, First Out technique, often known as the LIFO approach, is a system of accounting for the selling of stocks that requires the securities to be sold in the order in which they were obtained, with the most recently acquired shares being sold first. Last In, First Out indicates that the securities that have been held for the shortest length of time are sold first, followed by those securities that have been kept for the longest period of time.

The LIFO technique is only one of numerous options available to choose from when it comes to accounting for the sale of securities. There are also other methods, such as the FIFO method (first in, first out), in which the securities that were purchased first are the ones that are sold first, and the average cost method, in which the cost of the securities that are sold is based on the average cost of all of the securities that have been purchased. Both of these methods are examples of alternative methods.

The tax obligation that is incurred and the reporting that is done for the sale of securities might be affected by the method that is used. It is essential to discuss the matter with a tax expert or a financial consultant in order to ascertain which approach is the most suitable for a particular circumstance.

Last in first out is also used for inventory valuation that works on the assumption that the products that were added to your stock the most recently will be the ones that are sold first. In the cost of goods sold (COGS) calculation that your company performs, the LIFO method requires that the costs of the most recent models that your company has purchased (or produced) be deducted as an expense first. This means that you’ll disclose the cheaper price of the previous models as a stockpile, which can ultimately lead to reduced taxes on the overall transaction.

Let us see an example of LIFO to understand the same better. Let us assume that you bought 10 shares of Amazon on Monday, three shares of Apple on Tuesday and five shares of Tesla on Wednesday. Here, you will choose the 10 shares of Amazon first, followed by the three shares of Apple and five shares of Tesla.

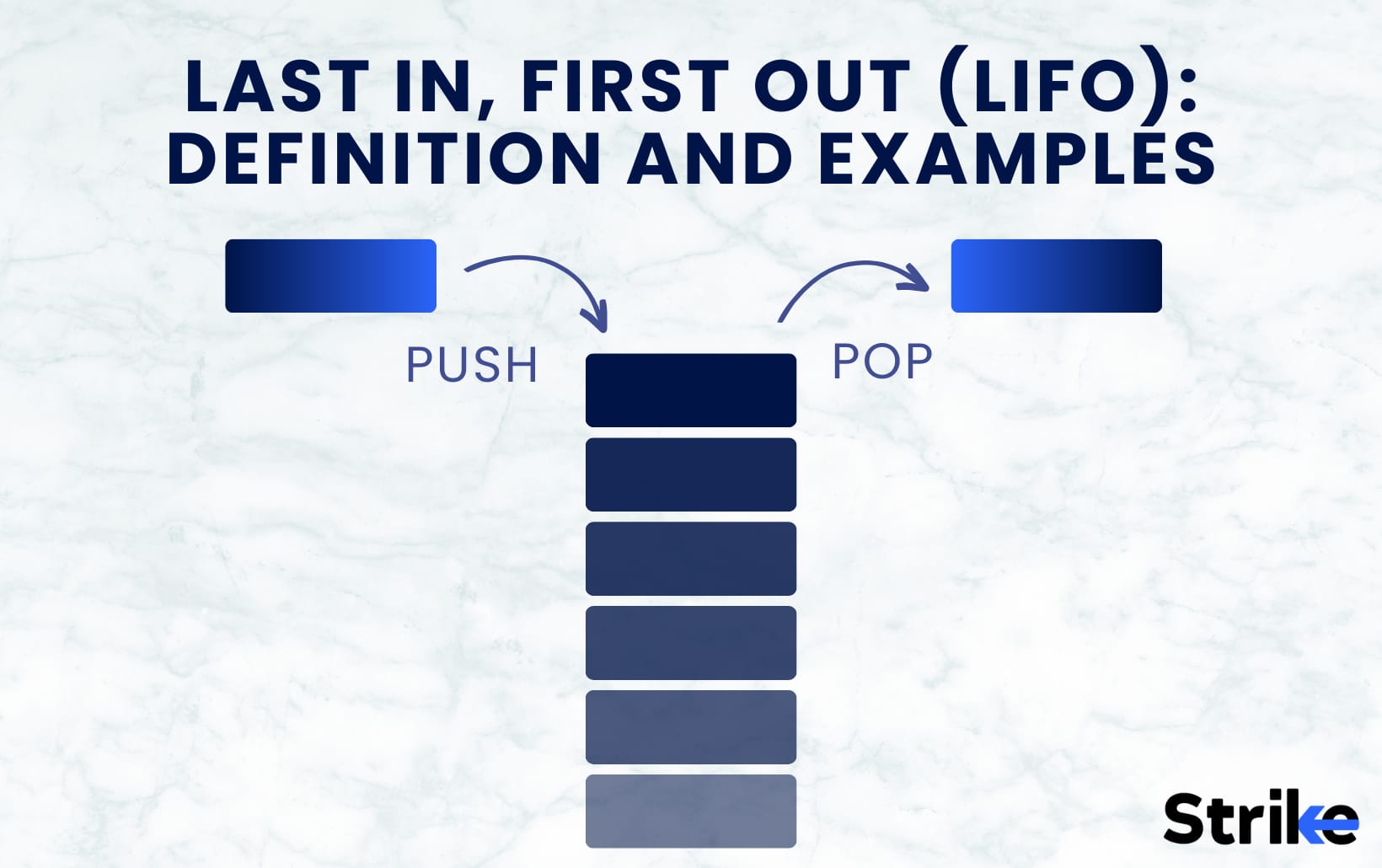

What is Last In, First Out (LIFO)?

Last in, first out (LIFO) is a system of inventory method where assets that are bought or acquired last are disposed of first. Last in, first out (LIFO) refers to a specific strategy for managing a portfolio of equities that entails selling the stocks that were most recently purchased first. LIFO strategy is founded on the presumption that the most recent acquisitions are likely to be the ones that are most overvalued and are thus the ones that are most susceptible to price drops.

Investors are able to better control risk with the LIFO approach because it lessens their exposure to companies that can be overvalued. This is one of the method’s primary Investors are able to better control risk with the LIFO approach because it lessens their exposure to companies that can be overvalued. This is one of the method’s primary advantages.

An investor has a better chance of mitigating their losses in the event that the market experiences a decline If an investor begins selling the stocks they have most recently purchased, they have a better chance of mitigating their losses in the event that the market experiences a decline.

Nevertheless, the LIFO approach is not without its potential downsides. For instance, it is possible that this method of selling equities is not necessarily the most tax-efficient way to do so, given that it may result in greater capital gains taxes on the sale of the stocks that were most recently purchased.

In addition, there is a possibility that the LIFO method, which entails selling equities that may still have the potential for gain in value, is not always the most effective strategy for maximizing returns.

One further thing that investors who use the LIFO approach need to think about is how it will affect the diversification of their portfolio. When selling the stocks that were most recently purchased, selling them all at once can result in a shift in the general makeup of the portfolio, which could potentially result in less diversity and increased risk.

In spite of these possible limitations, the LIFO approach can be a helpful tool for investors who are wanting to control risk and potentially decrease potential losses in a market that is volatile. Nevertheless, it is essential for investors to carefully analyze both their overall investing plan and the potential ramifications that the LIFO approach may have on their portfolio before making any commitments.

It is also important to note that the LIFO method is just one of many strategies that can be used to manage a portfolio of stocks, and investors should give careful consideration to their own financial objectives and level of risk tolerance when making a decision regarding which strategy is appropriate for them.

It may be good to contact a financial counsellor or professional portfolio manager in order to examine the benefits and drawbacks of the various strategies that are available, as well as to evaluate which strategy is the most suitable for your individual requirements and conditions.

What are the impacts of LIFO on Financial Statements?

LIFO has a substantial impact on financial statements when companies use it for their accounting. LIFO refers to a certain accounting approach that is used to determine the value of inventory as well as the cost of goods sold on the balance sheet of a corporation when it comes to company accounting.

LIFO approach makes the presumption that the things in inventory that were purchased the most recently will be the first to be sold, while the items that were purchased the longest ago will remain in stock.

The usage of LIFO can have substantial repercussions for the financial statements of a business because it has the potential to influence a company’s cost of goods sold, gross profit, and net income. For instance, the cost of the company’s goods sold and the cost of the things in its inventory rises over time if a firm utilizes LIFO accounting.

This can lead to a decrease in the company’s gross profit as well as its net income. On the other hand, the cost of products sold will go down as well if the cost of inventory items goes down over time. This can lead to a better gross profit as well as a higher net income.

The Last-In, First-Out (LIFO) technique of inventory valuation is simply one of options available to businesses, and it is not always the one that is best suited for every company. The decision about which technique to use for inventory valuation can be influenced by a wide range of considerations, such as the kind of business being conducted, the kind of inventory being maintained, and the tax circumstances of the company.

Companies that operate in industries in which the cost of inventory has a tendency to increase with time, such as the oil and gas industry, frequently adopt a system known as the Last-In-First-Out (LIFO) strategy. The cost of raw materials and other inputs may be subject to considerable swings in various industries as a result of changes in market conditions; hence, the LIFO method may be able to assist in more accurately reflecting the current cost of items supplied.

Nevertheless, the LIFO approach has potential downsides. It is possible for it not to accurately reflect the real physical movement of inventory because it is based on the assumption that the most recently purchased items will be sold first. This can lead to a difference between the LIFO valuation of inventory and the actual value of the inventory.

Using LIFO often results in a higher cost of goods sold, which can lead a company to pay more in taxes as a result. This may be a disadvantage for businesses with low-profit margins or those trying to maximize their earnings.

Despite these potential drawbacks, the LIFO approach is still widely used as a method for valuing inventory in the stock market. It is important for investors to understand the implications of using this method and how it can impact a company’s financial statements.

Below are the impacts of LIFO on financial statements of a company.

- The LIFO method can have an effect on the cost of goods sold, which is an essential component in the calculation of gross profit and can be found on the income statement. To calculate the cost of goods sold, first subtract the cost of inventory at the beginning of the period from the cost of inventory at the end of the period. Next, add any additional inventory purchases that were made during the period. Finally, divide this total by the number of units that were sold during the period. A company that utilizes the LIFO technique will base it on the most recent inventory purchases when calculating the cost of goods sold. This can lead to a higher cost of goods sold and a lower gross profit overall for the company.

- The LIFO approach has the potential to have an impact on the valuation of inventories on the balance sheet. In the last-in, first-out (LIFO) approach of inventory valuation, the value of the inventory is determined not by the actual cost of the inventory but rather by the most recent purchases. As a consequence of this, there is a possibility of a disparity developing between the LIFO valuation of inventory and the inventory’s real cost.

It is essential for investors to have a solid understanding of how the LIFO method is reflected in a company’s financial statements because it can have an effect on a company’s profitability and financial situation. Even while the LIFO method may be good for some businesses, it is possible that it is not the strategy that is best suited for every organization.

The decision about which technique to use for inventory valuation can be influenced by a wide range of considerations, such as the kind of business being conducted, the kind of inventory being maintained, and the tax circumstances of the company.

- Balance sheet valuation is of poor quality

The balance sheet valuation in the LIFO method does not use both the old and the new asset statements. Once the first set of goods are accounted for, they are not even much attention hence. This means that in the LIFO method, the earlier bookings or updation of the older goods will sit collecting dust for a long time before it gets to a point for it to be sold.

- Excellent income statement matching

This is true in regard to the LIFO method because they consider the newest statement of goods and assets. There will be slim chances of making an error since it is the most recent income statement that they look into.

What are the examples of Last In, First Out (LIFO)?

LIFO refers to a certain accounting approach that is used to determine the value of inventory as well as the cost of goods sold on the balance sheet of a corporation when it comes to company accounting. We can find examples of LIFO in real-life to understand this better.

- A pile of books: If you already have a pile of books on your desk and you want to add a new book to the top of the pile, you would do so by positioning the new book on top of the pile. To remove one of the books from the stack, you should start by taking the book from the very top of the pile (i.e., the most recently added book). LIFO is demonstrated here since the book that was uploaded most recently is the one that will be withdrawn first.

- A stack of plates in a cafeteria: You have a stack of plates in a cafeteria and you want to add a new plate to the stack, you would do so by placing the new plate on top of the stack. This would be the correct method. When you are ready to remove a plate from the stack, you should start by taking the plate that is located on the very top of the stack (i.e., the most recently added plate). LIFO is demonstrated here since the plate that was most recently added is the one that will be withdrawn first.

- A software stack: A stack is a type of data structure that is utilized in the field of computer science. It is capable of storing multiple elements at once. It is possible to push additional items to the top of the stack, as well as pull items from the top of the stack (popped). LIFO is demonstrated here since the item that was inserted most recently is the one that will be removed first.

- Queue: A data structure known as a queue is one that can be employed for the purpose of storing a group of things in accordance with a predetermined hierarchy. In most cases, items are shifted from the front of the queue to the back of the line (a process known as enqueuing), and vice versa (dequeued). However, if a queue is implemented using a LIFO data structure (such as a stack), then items will be added to the front of the queue and removed from the front of the queue, making it a LIFO queue. This is because items are added to the front of the queue before they are removed from the front of the queue.

LIFO is also used in stock markets as a portfolio management technique where the stocks bought last are sold first.

What are the advantages of Last In, First Out (LIFO)?

Last in, First out is a method that is extensively used by countries in the United States. They are rarely seen in India or a majority of other countries. The most obvious reason why companies use the LIFO method to account their inventory is to reduce their tax liabilities. LIFO generates only less net income compared to the other methods, but it also means less taxable income. There are other advantages as well.

Give an introduction to why companies use the LIFO method

LIFO has four main advantages as an accounting system for companies.

1. The price of the materials that are distributed will either be brought closer to the current market price or will reflect that price. As a result, the trend of the market price of materials will have some bearing on the cost of the goods that are produced. A movement like this in the price of materials makes it possible to balance the costs of production with the revenues currently being generated from sales.

2. Utilizing this method during a time when prices are increasing does not result in an abnormally high profit being reflected in the income statement, as it would have if the first-in-first-out or average method had been used. In point of fact, the profit that is depicted here is relatively lower than it would otherwise be because the cost of production takes into account the general upward trend of the prices of the materials.

3. Businesses typically see an increase in profits due to lower material costs, despite the fact that their finished products are priced at market levels and appear to be more competitive when prices go down.

4. The application of LIFO over a period of time helps to smooth out the peaks and valleys in profits.

There are four main advantages of LIFO as a portfolio management method.

- The application of the LIFO method may, in some circumstances, enable investors to incur fewer taxes on capital gains. This is due to the fact that the most recent purchases are considered to be the first ones sold, which means that any appreciation in the value of the securities or assets will be taxed at the rate that is currently in effect rather than the rate that was in effect at the time that the purchase was made.

- The Last-In, First-Out (LIFO) approach is simpler to use than other ways, such as the First-In, First-Out (FIFO) method, which needs investors to keep track of the sequence in which stocks or assets were purchased. The LIFO method, on the other hand, requires no such tracking.

- By assuming that the most recent purchases will be the first ones sold, the LIFO method takes into account the current market conditions and has the potential to produce a more accurate representation of an investor’s portfolio. This is accomplished by considering the most recent purchases to be the first ones sold.

It is crucial to evaluate all of the potential tax ramifications as well as any other considerations that may come into play before choosing a technique to use. It is also important to note that the LIFO approach is not always the most favorable choice for investors.

What are the disadvantages of Last In, First Out (LIFO)?

The main disadvantage of LIFO is its limited flexibility. Below are some other disadvantages.

- LIFO structures have limited flexibility because they only allow the insertion and removal of items from the top of the stack, which can make it difficult to access items located in the middle or bottom of the stack.

- LIFO structures are not well-suited for operations that require access to items in the middle or bottom of the stack, as these operations can be time-consuming and require a significant number of steps to complete.

- The ability to prioritize certain items over others is limited in LIFO structures because items are always added to the top of the stack and removed from the top.

- LIFO structures have a fixed capacity, and once the stack is full, no additional items can be added until some items are removed. This can be a disadvantage in situations where the stack is frequently used and the capacity is frequently reached.

- LIFO structures may be inefficient in terms of space utilization because items are added to the top of the stack, but they may not necessarily be removed in a timely manner. This can result in a large amount of wasted space in the stack.

- This technique displays the inventory at the most recent market price; as a result, the data does not accurately represent the current circumstances. If the cost rule or the market rule is used to determine the value of the inventory, it is possible that a significant adjustment may be required since the value at the end of the period is inaccurate.

- The FIFO accounting method is particularly susceptible to flaws during times of hyperinflation since it often fails to provide an accurate picture of costs if there is a significant and/or quick rise in the cost of materials. In this kind of scenario, it would not be acceptable to match the oldest inventory with the most recent sales; doing so may inflate up earnings and provide a false view of the situation. The same thing is capable of occurring at times when there is a significant swing in price.

When is the best time to use the Last In, First Out (LIFO)?

Companies believe the best time to use the LIFO method is during times of price rise. It’s possible that businesses will find it more advantageous to utilize LIFO cost accounting rather than FIFO during periods of increasing pricing. When prices are going up, companies may take advantage of LIFO to lower their tax burden and better align their income with their most recent expenses.

One reason why businesses choose LIFO rather than FIFO is because with LIFO, there are less inventory write-downs required during periods of inflation. When it is determined that the current market price of an inventory item is lower than its carrying value, this is known as an inventory write-down.

According to generally accepted accounting principles (GAAP), the carrying amounts of an inventory are recorded on the balance sheet at either the historical cost or the market cost, whichever is lower.

The market cost is constrained between an upper and lower bound, which are respectively the net realizable value (which is the selling price minus reasonable costs of completion and disposals) and the net realizable value minus normal profit margins. Both of these bounds are based on the net realizable value.

The most conservative inventory values are those that are reflected by the carrying amount of the inventories on a balance sheet when inflationary circumstances are present. These are the older costs of holding the inventories. Because of this, write-downs of inventory are often unneeded and only sometimes carried out when using the LIFO method.

Additionally, due to the fact that write-downs have the potential to lower profitability (by raising the expenses of goods sold) and assets (by lowering inventories), solvency, profitability, and liquidity ratios may all be adversely affected. Reversals of write-downs are not permitted according to GAAP.

As a direct result of this, businesses that are required to comply with GAAP have the responsibility of ensuring that each and every write-down is completely essential. Write-downs may have long-lasting effects.

Can I use the Last In, First Out (LIFO) method in the Stock Market?

Yes, the Last-In, First-Out (LIFO) technique can be used in the stock market, despite the fact that this strategy is not one that is used very often. In the context of the stock market, the last-in, first-out (LIFO) strategy is selling the shares that were acquired the most recently first, irrespective of their current value or the amount of time they have been held.

In the context of the stock market, using a LIFO strategy might have unintended consequences. For instance, if the value of the shares that were most recently acquired has declined after they were purchased, selling those shares first would result in a loss. This would be the case even if the value of the shares has increased overall.

Additionally, if the value of the older shares has improved since they were bought, then selling them later (as would be the case with a LIFO strategy) might result in losing out on possible gains. This is because the LIFO approach prioritizes selling the oldest shares first.

In the stock market, it is often more popular for investors to utilize a First In, First Out (FIFO) method, in which the oldest shares are sold first. FIFO is an acronym for “first in, first out.” This strategy provides the potential benefit of realizing any prospective capital gains or losses on the shares that have been held for the longest period of time, which may be advantageous when considering tax implications.

However, it is essential to carefully assess the strategy that would work best for your particular circumstances and to get professional assistance in the event that you need it.

Why is the United States the only nation that uses Last In, First Out (LIFO)?

Yes, the United States of America is the only country in the world to manage its inventory using the LIFO system, which stands for the “Last In, First Out” approach. The Last-In, First-Out (LIFO) method guarantees that the products that have been manufactured the most recently are sold first, and that older products are only sold when the stock of newer products has been completely depleted.

There are several reasons why the United States of America is the sole country that employs the LIFO system. To begin, using LIFO to manage inventory is a method that is both straightforward and effective. The method is easy to understand and implement.

Second, the LIFO method makes certain that items are always offered in the freshest condition possible, which is essential for preserving quality control. Last but the most important reason is that LIFO cuts down the net total income which would in turn mean that there are less tax liabilities. This might be one of the major incentives for companies to adopt the LIFO method.

Why is Last In, First Out (LIFO) prohibited in nations other than the United States?

Although it is not illegal to employ the LIFO (Last In, First Out) approach in other nations, acceptance of this practice is not quite as widespread as it is in the United States. This is due to the fact that the International Financial Reporting Rules (IFRS), which are the standards for accounting that are used by the vast majority of nations outside of the United States, do not acknowledge LIFO as a procedure that is compliant.

In accordance with the International Financial Reporting Standards (IFRS), the First-In, First-Out (FIFO) approach is usually regarded to be the technique that is best suited for valuing inventory. The reason for this is that FIFO is reflective of the real flow of commodities, which is how the vast majority of organizations function. LIFO, on the other hand, does not represent the real flow of products and may lead to the presentation of financial information that is inaccurate as a consequence.

Although LIFO is not illegal in other countries, it is not often used since the International Financial Reporting Standards (IFRS) do not recognise it as a technique that is compliant. Because of this, businesses who utilize LIFO can have trouble creating financial statements that are in accordance with IFRS, and they might be compelled to make changes to their financial statements in order to conform to these standards.

What is the difference between Last In, First Out (LIFO) and First In, First Out (FIFO)?

LIFO and FIFO are two systems that may be used to manage inventories or to monitor the sale or purchase of financial assets like stocks. LIFO stands for “last in, first out,” while FIFO stands for “first in, first out.” Both of these approaches can be employed. The sequence in which objects are added to or deleted from the inventory or asset list is the primary distinction between the two methods.

- When using LIFO, the things that were added most recently are the ones that are deleted or sold first. This indicates that the products that have been included in the inventory or asset list for the longest period of time will be the very last ones to be withdrawn or sold. For instance, if a corporation is managing its inventory using the LIFO method, it would sell the products that were most recently acquired first, regardless of the items’ worth or the amount of time they have been kept in stock.

- On the other hand, if you use the FIFO method, the things that were removed or sold first were the ones that were put to the inventory or asset list in the first place. This indicates that the products that have been included in the inventory or asset list for the longest period of time are the ones that will be removed or sold first. For instance, if a corporation were managing its inventory using FIFO, it would sell the oldest things first, regardless of the products’ worth or how long they have been stored in stock. This would be the case even if the value of the item increased over time.

- Both the Last-In, First-Out (LIFO) and the First-In, Last-Out (FIFO) inventory accounting methods each have their own set of benefits and drawbacks. Determining which method to use is contingent on a wide range of considerations, such as the nature of the company’s products or assets, the accounting and tax implications, and so on. It is essential to carefully evaluate the strategy that will work best for your particular circumstances and to get professional assistance in the event that you have questions about your finances.

Previous Article

Previous Article

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 4")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 5")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 6")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 10")

No Comments Yet.