The time value of an option refers to the portion of an option’s price that is not intrinsic value. Time value exists because there is still time remaining until the option expires, during which the option has the potential to become further in-the-money.

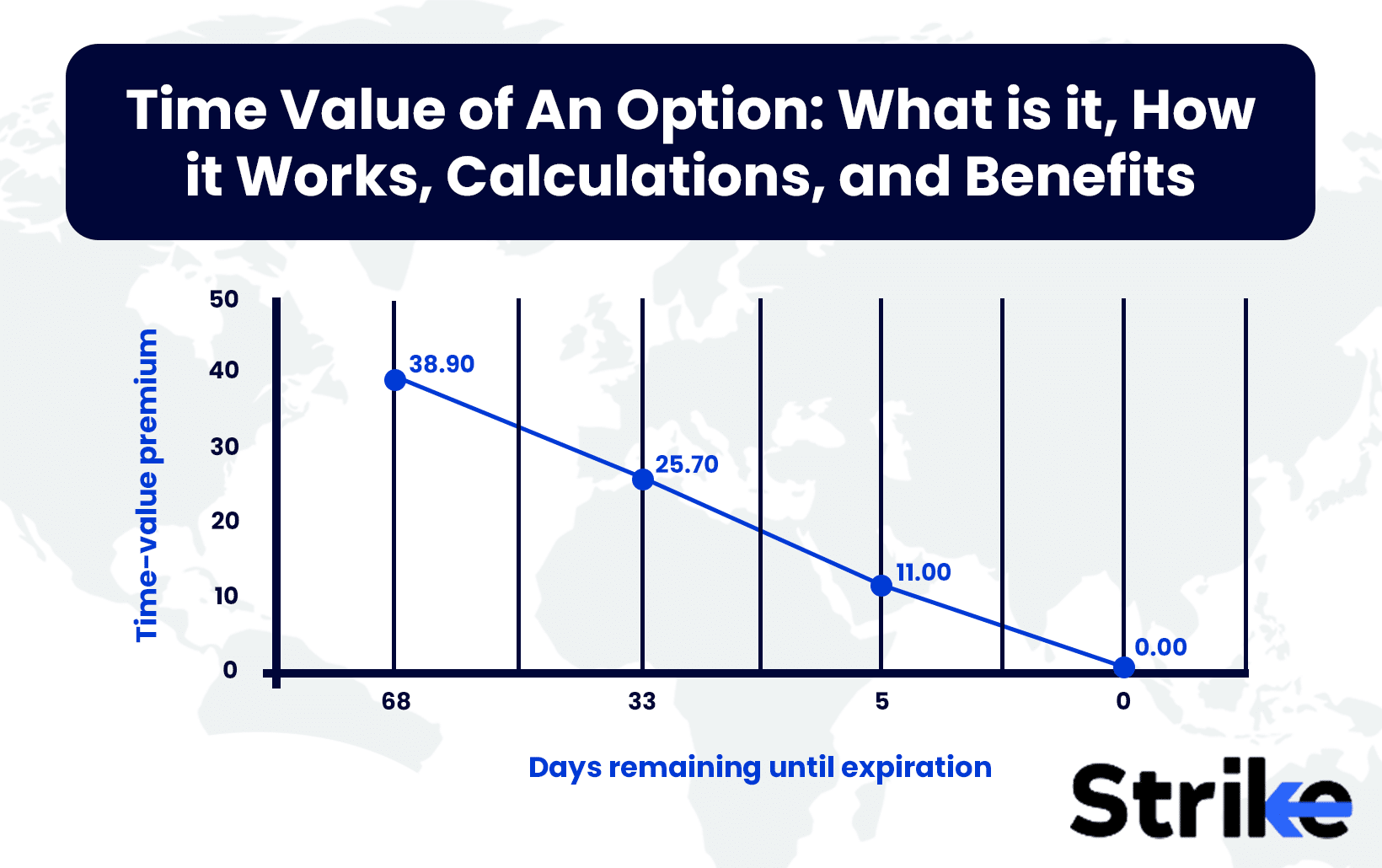

The longer the time until expiry, the greater the time value of the option since there is more time for the stock price to move favorably. As the option approaches expiry, time value decays rapidly. On the expiration date, time value drops to zero and only intrinsic value remains.

Time value is affected by several factors – the underlying stock’s volatility, time to expiration, and interest rates all impact time value. Higher volatility stocks have greater time value since there is higher potential for price movement. Longer dated options have higher time value with more time for favorable moves. Higher interest rates increase time value as well.

The key benefit of time value is it allows option buyers to obtain leverage. For a small premium, they control a much larger amount of stock. However, time value also presents a risk, since it decays rapidly and causes options to expire worthless if the stock price does not move enough. Traders look to balance the leverage benefits and decay risks when assessing time value.

What does the Time Value of An Option mean?

The time value of an option refers to the portion of an option’s premium that exceeds the option’s intrinsic value. An option’s premium is the total price paid for the option, while intrinsic value is defined as the amount by which the strike price of an option is in-the-money.

For call options, intrinsic value is the amount by which the underlying asset’s price is above the strike price. For put options, intrinsic value is the amount by which the strike price exceeds the underlying asset’s current market price.

Time value represents the additional value of an option beyond merely the intrinsic value. It is essentially the amount by which the premium exceeds the intrinsic value, if any. Time value exists because there is remaining time until option expiration, during which the option has the potential to become further in-the-money due to movements in the underlying asset’s price. The longer the time until expiry, the greater the time value of the option since there is more time in which the asset price move favorably.

As the option contract approaches its expiration date, time value decays rapidly. This is because there are fewer days remaining for the asset price to move advantageously. On the actual expiration date, time value drops to zero and only intrinsic value remains. An option never trade for less than its intrinsic value at expiration.

How does the Time Value of An Option work?

The time value of an option is derived from the uncertainty over the underlying asset’s price during the remaining life of the option.

The most common method for estimating an option’s time value involves using pricing models like Black-Scholes and Binomial Trees. These models take into account variables like the underlying price, strike price, time to expiration, volatility, interest rates and dividends to calculate the probable value of the option.

The models produce an estimated fair value for the option, with the difference between the fair value and intrinsic value being the time value. The inputs and assumptions of the pricing models directly impact the time value produced.

The models demonstrate how specific influencing factors affect an option’s time value. For instance, higher volatility of the underlying asset increases time value as it indicates wider potential price swing and greater odds of an advantageous finish for the option buyer. Longer duration to expiration also increases time value due to higher uncertainty over a longer period.

Higher interest rates used for discounting in the models boost time value slightly as well. Changes in these input factors cause the models to adjust the fair value and time value higher or lower accordingly.

As expiration approaches, the pricing models show time value decaying at an accelerating rate. With fewer days remaining, there are diminishing odds of substantial price moves that would further increase the option’s intrinsic value. Time value decay accelerates because uncertainty is rapidly declining as expiration nears. On the last trading day, time value converges to zero, leaving only intrinsic value.

Time value also impacts early exercise decisions. Models demonstrate it is typically not optimal to exercise an option prior to expiration while substantial time value still exists. It is better to sell the option and capture remaining time value rather than exercise and forfeit this. Only at expiration when time value is zero does early exercise become optimal.

Time value considerations are vital in options trading strategies. For example, sellers of options aim to capture time value premiums, so maximizing decay by shorting closer dated contracts while volatility is high is ideal. Hedging strategies like spreads also aim to take advantage of time value differentials between two or more options contracts.

An option’s “Greek” sensitivities – Delta, Gamma, Theta, Vega, Rho – indicate how time value responds to moves in input variables. For example, Theta indicates how much an option’s time value decays per day. Vega shows sensitivity to volatility. Greeks help traders manage the impact of time value fluctuations.

Timme value emanates from a complex web of uncertainty about the future path of the underlying asset’s price. Pricing models distill this uncertainty into a quantifiable estimate of time value subject to influencing factors. As uncertainty declines into expiration, time value dissipates. Traders utilize time value concepts to maximize their edge. Whether looking to capture, avoid, or manage time value, its mechanics form a key building block of options trading strategies.

Which Option has the highest Time Value?

At-the-money options possess the highest time value because they provide the greatest potential payout with odds close to 50/50, exhibit favorable Gamma and Delta attributes, are optimally traded in delta neutral strategies, provide optimal early exercise utility, benefit from volatility skew, and see inflated value from psychological bias. Their unique flexibility and probability profile make at-the-money options the time value maximizing choice for options traders.

At-the-money options have the highest probability of being profitable at expiration. They have roughly a 50% chance of finishing in-the-money since even a small price movement upward or downward will carry the underlying’s price across the strike price. Out-of-the-money options have lower profit odds since the asset price must move further favorably to cross the strike. Higher likelihood of a payout boosts an at-the-money option’s time value.

An option’s Gamma measures sensitivity of Delta to price changes. Delta indicates the option’s price movement compared to the underlying asset. At-the-money options exhibit the highest Gamma because even small moves in the underlying rapidly shift their Delta. Higher Gamma signifies greater odds of becoming deeper in-the-money before expiry, increasing time value.

Many advanced options traders construct delta neutral portfolios to solely capture time value. This involves balancing positive and negative Deltas to maintain zero directional bias. Since at-the-money options offer deltas closest to neutral at ~0.50, they are best suited for delta neutral trading that maximizes time value harvesting.

Early options exercise prior to expiration typically destroys time value. However, due to their unique profit profile, at-the-money options are most optimally exercised early when opportunities arise. The minimal time value lost is offset by higher odds of capturing intrinsic value. Thus at-the-money options retain maximum time value at any given moment.

Volatility skews on options chains cause out-of-the-money options to exhibit lower implied volatility than at-the-money options. This further depresses time value on out-of-the-money options. At-the-money options sit at the peak of the volatility skew, boosting their time value.

Options traders tend to overestimate the likelihood of substantial price moves and therefore overpay for the time value of out-of-the-money options. Conversely, they underestimate odds of smaller swings that would benefit at-the-money options. This psychological bias pushes at-the-money time value even higher relative to out-of-the-money alternatives.

What is the importance of the Time Value of An Option?

Time value is important as it facilitates leverage, efficient risk management, pricing model insights, trading strategies, exercise timing, downside protection cost benefit analysis, liquidity incentives, and limits on arbitrage.

Time value allows options traders to pay relatively small premiums upfront in order to control much larger exposures to the underlying asset. This provides leverage and efficiency. Without time value, traders would have to outlay cash equal to the full value of the underlying position. Time value unlocks leverage because uncertainty is priced into premiums.

In addition to upside leverage, time value also enables more efficient downside risk management. Investors hedge downside risk at a fraction of the cost of owning the underlying asset itself. Options allow tailoring of risk-reward profiles through time value. Portfolios are constructed to eliminate downside exposure beyond a desired point.

Time value represents a market-derived output of options pricing models like Black-Scholes. The models demonstrate how time value reacts to changing inputs like implied volatility, interest rates, dividends, strike prices and expiration dates. Time value enables estimating the probabilities of different price outcomes underlying an option’s value.

Time value provides opportunities for options traders to generate profit through its fluctuation and decay. Short sellers and credit spread traders look to capture time value. Methods like delta-hedging involve offsetting directional risks to isolate time value exposure. Without time value, many options strategies would be rendered unprofitable or pointless.

Since exercising options extinguishes remaining time value, assessing time value is essential for determining optimal exercise timing. Models demonstrate how much time value remains across various dates and price points. This helps investors avoid the mistake of exercising too early when significant time value remains on the option.

Time value sets the market cost of downside protection and leverage for an option position. Investors evaluate whether the time value premium is a worthwhile cost relative to the protection afforded by a given strike price and expiration. This aids in evaluating risk-reward payoffs across different option contracts.

Time value premiums compensate market makers and other liquidity providers for offering bids and offers on option contracts. Time value represents their potential reward for bearing the risks of holding short option positions as part of their function. Without time value profits, liquidity would be reduced.

Time value diminishes opportunities for arbitrage between an option and the underlying asset. Only at expiration when time value disappears perfect arbitrage exist. In the interim, time value ensures option prices differ from pure intrinsic value, preventing full arbitrage. This maintains orderly markets.

Does Time Value Affect the Option Contract?

Yes, time value significantly affects options contracts. The time value component is a major determinant of an option’s overall value and the factors influencing it directly impact the pricing and behavior of the option contract. Time value determines the premium price of an option, with higher time value leading to greater premium costs for traders looking to buy or sell the contract. As time value rises and falls, it alters the actual price paid for an option.

Time value also allows traders to obtain leverage by only having to outlay a fraction of the full price of the underlying asset when purchasing an option. More time value provides greater leverage for a given premium spent on a contract. This amplifies potential gains.

How is the Time Value of a Call Option calculated?

The time value of a call option is calculated as the difference between the current premium of the option and its intrinsic value.

The formula is

Time Value = Call Option Premium – Intrinsic Value

Where,

Call Option Premium = The full market price paid to buy the call option

Intrinsic Value = The amount by which the stock price exceeds the strike price of the call option

For example, say a call option has a strike price of Rs. 3,000 and the underlying stock is trading at Rs. 3,250. The call option premium is Rs. 200.

The intrinsic value is Rs. 3,250 – Rs. 3,000 = Rs. 250

Applying the formula:

Time Value = Call Option Premium – Intrinsic Value

= Rs. 200 – Rs. 250

= Rs. -50

In this case, the time value is negative Rs. 50. This occurs when the current premium is less than intrinsic value, meaning the option is trading at a discount to fair value.

The key steps are

Identify the call option premium based on current market price

Calculate intrinsic value by taking stock price minus strike price

Subtract intrinsic value from premium to derive time value

If time value is negative, it means the option is undervalued based on fundamentals

Time value will approach zero as the option nears expiry

This demonstrates how to derive the time value component of a call option premium based on fundamental factors like stock price, strike price and expiry. The premium can then be analyzed versus time value to assess if the call option is rich or cheap.

How is the Time Value of a Put Option calculated?

The time value of a put option is determined as the difference between the premium paid for the put and its intrinsic value.

For put options, the intrinsic value is calculated as:

Intrinsic Value = Strike Price – Stock Price

The strike price represents the fixed price at which the put option allows selling the underlying stock. The stock price is the current market price of the underlying security. Subtracting the stock price from the strike gives the in-the-money amount, if any, for the put option.

Once intrinsic value is calculated, time value is derived by taking the put option premium and subtracting intrinsic value:

Time Value = Put Option Premium – Intrinsic Value

Where put option premium is the full price paid to purchase the put contract on the open market.

For example, consider a put option with a strike price of Rs. 3,150 on a stock currently trading at Rs. 3,000. The put option premium is Rs. 175.

First, calculate intrinsic value:

Strike Price = Rs. 3,150

Stock Price = Rs. 3,000

Intrinsic Value = Strike Price – Stock Price\

= Rs. 3,150 – Rs. 3,000

= Rs. 150

Next, compute time value:

Put Option Premium = Rs. 175

Intrinsic Value = Rs. 150

Time Value = Put Option Premium – Intrinsic Value

= Rs. 175 – Rs. 150

= Rs. 25

In this example, the Rs. 25 time value represents the portion of the put premium not explained by in-the-money intrinsic value.

The time value is negative indicates the put option is undervalued in relation to its intrinsic value. A positive time value means higher premium than strict intrinsic value, indicating the put is likely overvalued based on current fundamentals.

As expiration approaches, time value converges to zero, leaving only intrinsic value in an option’s premium.

What are the factors affecting the time value of an Option?

The time value component of an option’s premium depends on key variables. volatility, time decay, interest rates, strike price, underlying price, and dividends all significantly influence the time value of an option.

Underlying Asset Volatility

Volatility measures how widely and rapidly the price of the underlying asset, such as a stock, fluctuates over time. Higher volatility translates to wider potential price swings and a greater range of possible outcomes before option expiration. This increased uncertainty boosts the time value of options. Options on assets with lower volatility have less uncertainty priced into time value.

Time to Expiration

The amount of time remaining until the option contract expires also strongly influences time value. More time until expiry allows for a greater likelihood of substantial price moves that would push the option deeper into profitability. Shorter dated options have less time for favorable price action to materialize, reducing time value. All else equal, longer expiration options will exhibit higher time value.

Interest Rates

Prevailing interest rates impact time value because the fair value of options is calculated using discounted cash flow models. Higher interest rates increase the present value of potential future profits. Lower rates reduce the present value of potential payouts. Rising rates tend to increase time value, while declining rates lower it.

Strike Price

For a given underlying price, time value is maximized when the option strike price is at-the-money. In-the-money and deep out-of-the-money options will have lower time value. This is because at-the-money strikes provide the greatest odds of remaining profitable through expiration.

Underlying Price

Assuming other inputs unchanged, a higher underlying asset price will translate to greater time value for call options, while reducing time value for put options. The intrinsic value component expands for calls and shrinks for puts as underlying price rises, impacting the premium distribution.

Dividends

For options on dividend paying stocks, upcoming dividend payouts diminish time value. This is because dividends represent guaranteed pay outs that reduce uncertainty, unlike potential price appreciation. Bigger dividends require greater time value reductions.

Models like Black-Scholes capture how changes in these inputs alter time value based on the revised probability distribution of potential outcomes. Understanding the factors that drive time value is key for traders seeking to profit from its fluctuations.

What are the benefits of the Time Value of an Option?

Grasping the concept of time value and its impact on options pricing provides significant advantages for traders and investors. Ten main benefits include the below.

Assessing Value

Understanding time value allows determining if an option is rich or cheap relative to its intrinsic value. Comparing an option’s premium to its time value and intrinsic value composition indicates whether it is overvalued or undervalued based on current fundamentals.

Informed Entry/Exit

Knowing the factors that influence time value aids in deciding optimal entry and exit points for trades. Since time value fluctuates, traders time entries to coincide with periods of relatively low time value and higher intrinsic value composition.

Leverage Optimization

Time value provides leverage, as option buyers only pay a percentage of full price of the underlying asset. Comprehending what drives time value enables optimizing leverage for a given premium outlay. Higher time value equals greater leverage for the same capital.

Expiration Management

Time value considerations are key around option expiration dates. Holding too long risks losing entire remaining time value, while closing too early forfeits potential gains. Understanding time value decay aids expiration management.

Risk Management

Time value is a source of risk, as it erodes to zero resulting in losing the entire premium paid. Knowledge of time value behavior allows incorporating it into overall position sizing and risk management calculations.

Trading Strategy Development

Many advanced options trading strategies are designed around capturing time value, such as credit and debit spreads, straddles, and strangles. Time value principles inform strategies and trade idea generation.

Early Exercise Decisions

Since exercising options eliminates remaining time value, evaluating whether significant time value remains is crucial for early exercise decisions. This helps avoid leaving money on the table by exercising too soon.

Forecasting Moves

Fluctuations in time value help forecast potential moves in the underlying asset ahead of major events like earnings. Unusual changes in time value often presage price moves as traders position early.

Model Validation

Observing actual time value versus model prices helps validate the accuracy of pricing models like Black-Scholes. Consistent variances from model time values indicate opportunities to refine inputs and assumptions.

Cost/Benefit Analysis

Traders weigh time value paid versus downside protection provided for hedging decisions. Assessing whether time value is a worthwhile cost relative to the risk mitigation enables prudent hedging.

A solid understanding of time value provides diverse benefits spanning value assessment, entry/exit timing, leverage optimization, expiration management, risk control, strategy development, early exercise decisions, forecasting, model validation, and cost/benefit analysis. For options traders, time value mastery confers a significant edge.

What are the limitations of the Time Value of an Option?

While offering useful leverage and trading advantages, the time value component of options also carries inherent drawbacks and limitations including.

Time Decay and Premium Loss

The erosion of time value through time decay represents the largest risk to option buyers. Time value evaporates as expiration approaches, resulting in a declining option premium. Traders \lose 100% of the time value paid if the underlying asset price does not move favorably before expiry. Managing time decay is challenging.

Model Risk

Pricing models like Black-Scholes rely on estimates and assumptions to derive time value. However, actual market prices may diverge from model valuations. If models underestimate time value, traders may overpay. Errors in projecting time decay also exist.

Volatility Risk

Time value is highly dependent on implied volatility. Volatility contractions swiftly lower time value and premiums, leading to losses. Meanwhile, spikes in volatility raise time value, increasing hedging costs. Changes in volatility are challenging to predict.

Interest Rate Risk

While less substantial than other inputs, interest rate moves still impact time value. Rate declines reduce time value, while hikes raise it. Interest rate shifts may not be fully factored into model-derived time values, posing another risk.

Early Exercise Risk

Exercising an option before expiration forfeits any remaining time value. Traders must closely monitor time value when considering early exercise. Otherwise, they may inadvertently give up uncaptured time value by exercising too soon.

Opportunity Cost

Initial time value paid is tied up capital that could have otherwise been allocated to other assets. There is an opportunity cost of allocating capital to time value rather than other investments.

Liquidity Constraints

Thinly traded options may have very wide bid-ask spreads, making precise time value calculations difficult. Low liquidity makes entering and exiting at optimal time value levels challenging.

Psychological Biases

Some traders overestimate very low probability events, overpaying time value on long shot options. Others underestimate likely moderate moves, underpaying time value on closer dated options. Behavioral biases distort time value analysis.

Transaction Costs

Given that most options expire worthless, transaction fees to repeatedly enter and exit options seeking time value gains become burdensome. This frictional cost erodes profitability over time.

Tax Optimization Constraints

Time value tax treatment varies by region and may not be optimal for limiting tax liability. This constrain time value trading strategies and exercise decisions for certain traders.

While time value enables leverage and hedging capabilities, it also carries risks surrounding decay, model pricing, volatility, interest rates, early exercise, opportunity costs, liquidity, psychology, transactions, and taxes. Traders must be cognizant of these limitations when deploying time value-based strategies.

Does the Time Value of an option decrease as the expiration date approaches?

Yes, the time value of an option decreases as it approaches its expiration date. This is because there is less time remaining for the underlying asset’s price to move in a favorable direction to further increase the option’s intrinsic value. Less time equals less uncertainty equals lower time value.

Is it possible to have a negative Time Value of an Option?

Yes, it is possible for an option to have negative time value. This occurs when the option’s premium is trading below the option’s intrinsic value. Reasons for negative time value include significant changes in volatility or lack of liquidity for the option contract.

Can the Time Value of an Option be zero?

Yes, the time value component of an option can be zero. This occurs when an option is at expiration, as time value converges to zero on the expiration date. At expiry only intrinsic value remains in an option’s premium.

Do Out of Money (OTM) Options have Time Value?

Yes, OTM options have time value since there is still a possibility of the underlying asset price moving across the strike price to bring the option into profitability before expiration. Even deep OTM options retain some time value for this probability.

Do In The Money (ITM) Options Have Time Value?

Yes, ITM options still have time value premium built into their price. While ITM options have non-zero intrinsic value, they also benefit from remaining time to expiration for additional value-boosting price movements.

What is the difference between the Intrinsic Value and Time Value of an Option?

The intrinsic value of an option is defined as the amount by which it is in-the-money. For call options, this is the difference between the underlying asset’s current market price and the option’s strike price when the market price is above the strike.

For put options, intrinsic value is the difference between the strike price and market price when the strike is higher than the current market value. Essentially, intrinsic value represents the theoretical profit built into the option if exercised immediately based on the spread between market price and strike price.

Intrinsic value serves as a lower bound on the price of the option. An option’s premium can never be less than its intrinsic value, as traders would otherwise execute arbitrage strategies buying the underpriced option and exercising to capture the locked-in profit.

At expiration, intrinsic value and the option premium converge as time value expires. Prior to expiry, intrinsic value fluctuates as the asset price moves relative to the fixed strike price. It represents the tangible value readily extractable from the option at any given moment.

In contrast, time value represents the amount by which the actual market price of an option exceeds its current intrinsic value. While intrinsic value is locked in and known, time value relates to uncertainty looking forward to expiration date. Time value compensates the option seller for taking on risk beyond just the present in-the-money amount. An out-of-the-money option has no intrinsic value, thus its entire premium consists of time value, also known as extrinsic value.

What creates this additional time value? Primarily the volatility of the underlying asset over the remaining life of the option. More volatility implies a greater range of possible outcomes ahead of expiration, some of which would further increase the option’s intrinsic value if realized.

Greater upside potential equals higher time value. Time value is also influenced by time remaining until expiry, interest rates, and other option Greeks like Delta and Gamma. As the option approaches expiry, time value decays exponentially since less uncertainty remains. Let us look at some other key differences.

Previous Article

Previous Article

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 4")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 5")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 6")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 10")

No Comments Yet.