Theta is one of the main Greeks used to measure an option’s sensitivity. Theta is expressed as the amount the option price reduces per day all else equal. Theta represents the rate of time decay priced into an option contract. Theta quantifies the loss in option value due to the passage of time alone as expiry approaches.

Time decay impacts the extrinsic value or time premium of an option. As expiry gets closer, uncertainty is reduced making the option less valuable. Theta decay benefits the option seller who collects premium upfront. But it works against option buyers since purchased contracts lose time value.

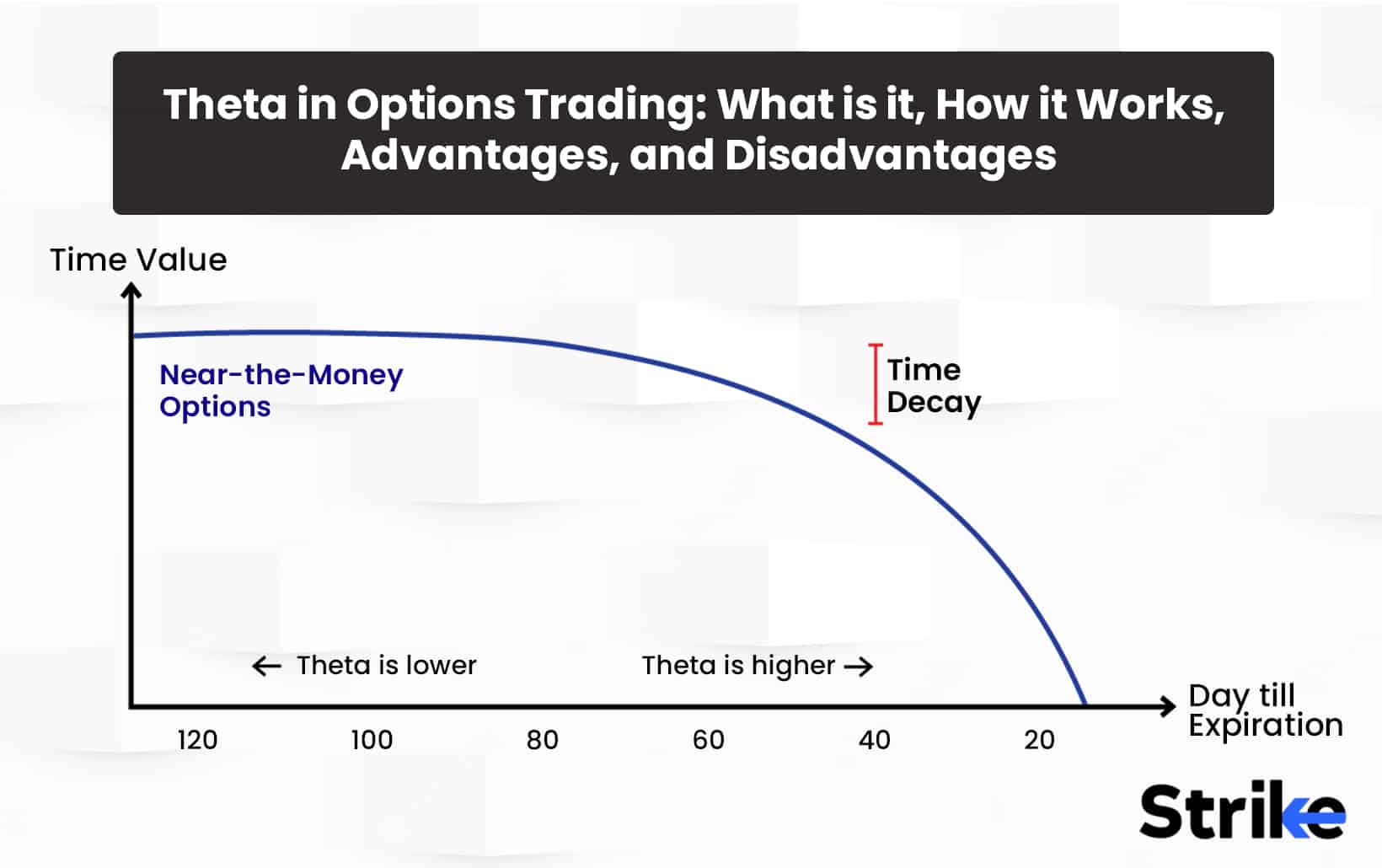

Theta is highest for at-the-money options close to expiration as time value erodes most rapidly then. Deep in-the-money and far out-of-the-money options have lower theta. Longer dated options also exhibit lower theta decay rates.

A key advantage of theta for option sellers is consistent decay leading to predictable income. By selling options to collect premium, theta becomes a reliable source of gains. Theta also accelerates near expiry, boosting odds of profit.

However, theta also works against option buyers. Purchased options losing time value leads to erosion in position profits over time. Buyers need directional moves in the underlying stock to offset theta decay.

What is Theta in Options Trading?

Theta in options trading is a measure of the rate of decline in the value of an options contract due to the passage of time. Theta represents the amount by which the value of an option will decrease for each day that passes. Options contracts have an expiration date, and the underlying principle behind theta is that options lose their value as that expiration date approaches.

The theta for an option is typically represented as a negative number, indicating the amount of value loss per day. For example, an option with a theta of -0.05 would lose Rs. 0.05 in value for each full day that passes. Theta tends to accelerate as expiration approaches, so the daily value decay gets larger as time goes on.

Theta exists because options have what is known as time value or extrinsic value. This represents the amount of premium that is priced into the option above its intrinsic value, which is tied to how much the option is in-the-money. Time value exists because there is uncertainty ahead until expiration, so an option has a chance of moving deeper into profitable territory. However, as time passes, there are fewer days remaining until expiration for this to occur, so uncertainty declines along with the option’s time value.

Theta is one of the main Greek risk metrics used in options trading, along with delta, gamma, vega, and rho. Of these, theta is most closely linked to the passage of time until the option’s expiration date. The rate of time value decay, as represented by theta, accelerates particularly rapidly in the last month before expiration, as the window for favourable price moves narrows.

Traders use theta to gauge how much they expect an option’s value to decline each day and assess the amount of time value remaining. Longer-dated options tend to have higher theta values, while short-dated options have lower theta. Deep in-the-money and deep out-of-the-money options will have relatively low theta values, as intrinsic value does not decay while extreme options are unlikely to make major moves into the money ahead of expiration.

Traders want to select contracts with relatively low theta when buying options so that the position loses less value each day. High theta is preferred when selling options so that the short option position benefits more from time decay. Theta is favourable for options sellers rather than buyers.

Managing positions as expiration approaches is an important aspect of trading options with a focus on theta. Traders look to roll positions to a later expiration to reset theta if they want to maintain exposure. Alternatively, positions are closed out as short theta options near expiration.

How does Theta in Options work?

Theta in options works by representing the amount an option’s value is expected to decline due to the passage of time. At expiration, options only retain their intrinsic value, not time value or extrinsic value. This means theta works by steadily eroding the time value priced into an option contract. The key drivers that impact the rate of theta decay are the current time to expiration, implied volatility, and how deep in/out of the money the option is.

As expiration approaches, theta acceleration increases because time value decays at its fastest speed in the last 30-60 days. With less time remaining, there are fewer chances for the option to move into substantial profitability.

Higher implied volatility increases theta decay because volatility adds to an option’s time value. As this volatility component declines, it boosts the speed of time value erosion. Low volatility reduces theta decay.

Deep in-the-money and deep out-of-the-money options have lower theta because higher intrinsic value is not impacted by time decay. Options at-the-money or closer to it exhibit more rapid theta burn.

Theta is not linear but rather exponential, accelerating as expiration nears. It will be slower when the option has 6 months to expiration versus 2 months. The last month sees a very rapid theta burn, as time value disappears.

Traders use theta to gauge how much value they expect an option to lose each day. But theta only represents the expected daily time value erosion – in practice, other factors like underlying price moves will impact the option’s price.

For sellers of options, theta works in their favour as it enables the short option position to benefit from daily time decay. As each day passes, the short option loses value, allowing the options seller to potentially buy it back cheaper and pocket the difference as profit.

Buyers of options are negatively impacted by theta decay working against their long position. The theta metric guides traders on when to close out long options to avoid holding into rapid time value erosion near expiry.

As an example, consider a deep in-the-money call option.

Say a stock is trading at Rs. 50 and the Rs. 40 strike call option has a price of Rs. 11 and theta of -0.05. This means the call option has Rs. 11 of time value above the Rs. 10 intrinsic value (Rs. 50 stock – Rs. 40 strike price). The theta of -0.05 indicates the call option is expected to lose Rs. 0.05 in value each day. The call option price would decay to approximately Rs. 10.50 if the stock price holds at Rs. 50 for 10 days (starting at Rs. 11 and decreasing by Rs. 0.05 theta for 10 days). The call would retain most of its intrinsic value but lose time value due to theta decay over those 10 days. The call price rises to reflect higher intrinsic value despite the impact of theta if the stock rallies to Rs. 60.

As this example illustrates, theta represents the isolation of time decay’s expected effect. But in practice, other factors like underlying price moves outweigh theta in the short run. Yet over time, theta grinds away at an option’s extrinsic premium.

How does Theta differ from other Option Greeks?

The Greeks all , including theta function as risk measures, but theta has certain special qualities which differs from other option greeks.

Delta measures the sensitivity of an option’s price to a Rs. 1 change in the underlying asset price. It represents the option’s price leverage. Theta is purely time focused – it quantifies the expected time decay irrespective of underlying price moves.

Gamma gauges how much delta itself changes when the underlying price moves. It indicates the acceleration of delta. Theta does not change or accelerate – it represents a steady daily erosion of time value at an increasing rate into expiration.

Vega quantifies an option’s price sensitivity to a 1% change in implied volatility. Theta conversely focuses on time sensitivity not volatility. However, higher implied volatility boosts an option’s time value, which does mean larger theta decay. But theta measures value erosion due to time alone.

Rho indicates how much an option’s price changes based on a 1% shift in the interest rate. Theta is completely unrelated to interest rate sensitivity or investment returns.

Delta, gamma, and vega reflect how outside forces like price and volatility impact option value. Theta represents the internal time decay of the option itself.

Delta, gamma, and vega are positive or negative depending on option type. Theta is always negative to indicate time value erosion. Delta, gamma, and vega are focused on relative value change. Theta quantifies an absolute value expected to be lost daily. Delta, gamma, and vega are relevant no matter if an option is long or short. Theta decay impacts long options, but benefits short options. Delta, gamma, and vega fluctuate up and down with market movements. Theta steadily becomes more negative as expiration nears.

Delta and gamma are key for directional option trades betting on larger price moves. Theta aligns with non-directional strategies relying on time decay. Vega is most relevant for volatility-focused option trading strategies like straddles or strangles. Theta relates to maximising time decay across multiple legs. Rho matters most for highly interest rate sensitive strategies like bond or rate options. Theta is applicable to any option expiring in a given time frame.

What does Theta do in Options Trading?

Theta do represent the rate of decline in an option’s value due to the passage of time in options trading. It quantifies the erosion of time value as the option moves closer to expiration. Theta exists because options have a defined life and uncertainty ahead of expiry. The roles theta plays in options pricing and trading strategies are vital to understand.

At expiration, options only retain intrinsic value – the difference between the stock price and strike price. All extrinsic value or time value decays to zero as expiry approaches. Theta encapsulates this concept of time decay priced into options. It expresses the expected loss in option value per day due to this erosion of time premium.

Theta indicates how much urgency or “speed” an option holder faces before time value disappears. Higher theta means faster time decay, lowering the chance the option remains profitable. Theta is always negative since time value only decreases, not increases as expiration nears. It accelerates exponentially in the last month before expiry.

Traders use theta to evaluate if an option still holds enough time value to meet a profit target from an anticipated price move. Long option holders want to exit before theta ramps up drastically near expiration. Sellers Benefit from theta eating away at the value of short options positions.

Theta exists because options have defined expiration dates. Unlike stocks which trade indefinitely, options cease to exist after expiry. This lends options a finite window to reach profitable price points. Time value compensates sellers for uncertainty until expiry. But as that uncertainty declines closer to expiration, so does time value through theta decay.

Is Theta used in Stock Trading?

No, theta is not directly used in stock trading.. Stocks have no defined term and trade indefinitely, so the concept of theta does not apply to stock price analysis.

What is the importance of Theta in Options Trading?

Understanding and managing theta is critically important for options traders given its role in strategy, risk management, and profit potential. Theta quantifies a defining characteristic of options – their finite lifespan. Unlike stocks, options cease to exist after expiration so time until expiry is intrinsically linked to an option’s value. Theta encapsulates the sensitivity of an option’s price to this expiry date.

Theta dictates urgency and trade duration for options positions. Higher theta means faster time decay, indicating less time to hit a profit target before expiration. Traders evaluate theta to determine optimal options contract duration.

Time decay benefits options sellers. Theta decay steadily erodes the value of short options positions, allowing sellers to potentially realise that decay as profit without relying on directional price moves in the underlying.

Time decay hurts options buyers. The power of theta means the underlying must make directional moves just to offset an option’s time value erosion before expiration. Analysing theta helps set profit targets.

Theta impacts risk-reward evaluation. An option appears to offer large profit potential but also have substantial theta that drastically lowers expected return on capital over a given hold period.

Theta influences strategy selection. Strategies reliant on time decay like credit spreads, iron condors, and covered calls all require assessing Theta. Directional trades prefer managing other Greeks.

As a quantitative measure unique to options, theta provides an invaluable risk management tool for traders. It represents the omnipresent force of time working against options positions. Mastering theta is required to improve probability of profit, maximise potential returns, and strategically offset time decay – factors essential to options trading performance.

How is Theta calculated for Options Trading?

The theta calculation process revolves around using the Black-Scholes options pricing model. A differential equation called the Black-Scholes model is used to price options depending on five important inputs – Underlying stock price, strike price of the option, time to expiration of the option, risk-free interest rate, implied volatility of the underlying stock.

The Black-Scholes model computes a theoretical fair value for an option by incorporating these parameters. Greek risk metrics like theta are derived from this pricing model as well.

Specifically, theta is calculated by taking the partial derivative of the Black-Scholes formula with respect to time. This means assessing how the model’s theoretical option value changes based solely on a decline in the time to expiration variable, holding the other inputs constant.

The partial derivative leads to the following general formula for theta:

Theta = -[Spot Price x Volatility x (d1) x exp(-r x T)] / [Square root of T]

Where:

Spot Price = Current price of the underlying stock

Volatility = Implied volatility of the stock

d1 = The standard normal probability variable in the Black-Scholes model

r = Risk-free interest rate

T = Time to expiration

This formula quantifies the instantaneous rate of change in the option price due to time decay. The negative sign indicates declining value as time passes.

In practice, traders approximate theta values using a discrete approach. Estimated future prices over a series of short time intervals leading to expiration are modelled.

For example, the closing price today and estimated prices at the market close over the next 5 days might be projected. Theta is then calculated as:

Theta ≈ [Current Option Price – Projected Price in 1 day] / 1

This discretizes theta to a daily time interval that is more practical than an instantaneous rate. Traders evaluate the expected price change per day rather than per instant.

Based on this discretized approach, theta values are typically quoted at the projected decay over a 1 day period, but also be annualised to a yearly rate.

How does volatility affect Theta?

Volatility has an inverse effect on theta decay. Higher volatility boosts theta while lower volatility reduces the impact of time decay. Time value exists because of uncertainty in the underlying price ahead of the option expiry date. Volatility is a proxy for this uncertainty – high volatility means wider potential price range and more uncertainty ahead.

As volatility rises, time value expands to compensate for greater uncertainty. However, as time passes, there are fewer days remaining until expiry for that uncertainty to play out favourably. So the time value boosted by higher volatility decays faster through accelerated theta.

A call option has a theta of -0.05 when implied volatility is 25%.Theta increases to -0.07 with 35% implied volatility, suggesting a greater rate of daily temporal value loss.

The higher volatility added extra time value, but that additional premium decays quicker.

Conversely, lower volatility shrinks time value and hence reduces theta. With less uncertainty priced in, each day has less impact on the probabilistic outcome ahead of expiration.

From a strategy perspective, high volatility enhances theta’s role for short options positions. The accelerated decay allows sellers to realise greater gains as the short calls or puts lose value faster with each day passed.

For options buyers, high volatility presents a double-edged sword. The added time value provides more profit potential, but also leads to faster depletion through theta decay. Managing the trade before this accelerated erosion becomes severe is key.

Options have less time premium to begin with when volatility is low. While this reduces profit potential for buyers, it also diminishes the daily bite of theta decay. Positions are held longer without substantial loss of time value each day.

What is a good number for Theta in Options?

There is no objectively “good” or “bad” level of theta – its implications depend on your trading strategy and goals. However, when analysing theta numbers, some general principles apply.

For shorter-term option trades, higher negative theta values are typically preferred. This indicates substantial decay each day which is beneficial over a short horizon for theta-positive strategies like credit spreads.

For longer-term option trades, lower negative theta values are favoured. Minimal daily time decay is advantageous for strategies seeking to maintain leverage over weeks or months.

Deeply in-the-money or out-of-the-money options tend to have relatively low theta values. Theta decay has less impact on intrinsic value.

At-the-money and near-the-money options exhibit the highest theta values since time value is maximised. Theta has the largest effect on these contracts.

Time to expiration greatly influences theta rate. The same option will have much higher theta during the last month to expiry versus many months out.

For buyers, lower/slower theta allows room for the underlying to move favourably and reduce loss of time value each day.

For sellers, higher/faster theta enables maximising gains from short options decaying quickly into expiration or early assignment.

Portfolio theta gives a net view. Many theta-positive positions offset by some theta-negative hedges balance risk well.

What is considered a high Theta in options?

A high theta in options generally refers to a theta value of 0.05 or higher. This value means the option is losing significant value from the passage of time each day, making it more advantageous for the seller and less ideal for the buyer as expiration approaches.

However, proper context is crucial. An option with -0.10 theta is low if expiration is tomorrow, but high if it is 6 months away. Time left until expiry is a key driver of expected theta.

For buyers, lower theta is typically preferable to delay time value erosion. But very low theta also means limited profit potential from volatility expansion. Moderately low theta balances these factors.

For sellers, higher theta allows maximising gains from short options decay. However, extremely high theta could signal volatility skew overpricing those options. Reasonably high theta balances time decay versus volatility risk premium.

Which Option Has the Highest Theta?

ATM options usually have the highest theta. An option is an ATM when the underlying price is trading right at the strike price specified in the options contract. For a call option, this means the stock price equals the call strike. For a put, an ATM is where the stock price matches the put strike.

The highest theta is seen in ATM choices for a seven of important reasons. ATM options have the greatest extrinsic or time value. Options only hold intrinsic value when in-the-money from the underlying trading above the call strike or below the put strike. ATM sits right at that pivot point. Maximum extrinsic value means ATM options have the furthest potential to move into the money.

This uncertainty ahead of expiration creates a large time value subject to theta decay over the option lifetime. Deep in-the-money or deep out-of-the-money options mostly or entirely consist of intrinsic value. There is minimal uncertainty about these options expiring in-the-money so little extrinsic value to erode through theta. Theta accelerates as an option moves toward the money.

ATM options already reside at that optimum pivot area with maximum sensitivity to time value erosion. Implied volatility used to price ATM options tends to be higher than for further out-of-the-money options. This volatility premium creates additional extrinsic value to decay through theta. With underlying prices centred at the strike prices, ATM options exhibit substantial delta and gamma, making their values highly sensitive to price movements of the stock. This magnifies the time value subject to theta.

Major price swings are required for deeply out-of-the-money options to ever reach ATM status. Limited time value means minimal theta while the position remains a low-probability bet relying on large directional moves.

Does ITM Option have a low Theta?

Yes, in-the-money (ITM) options tend to have relatively low theta values compared to at-the-money (ATM) and out-of-the-money (OTM) options. Theta represents the estimated amount an option loses per day from time decay. ITM options have lower theta because a substantial portion of their value consists of intrinsic value rather than extrinsic value.

An ITM call option is one where the current stock price is above the call strike price. For example, a Rs. 50 call option would be ITM if the stock trades at Rs. 55. An ITM put option is where the stock price is below the put strike. A Rs. 50 put would be ITM if the stock trades at Rs. 45

Is Theta the same for the put option and call option?

No, theta is not necessarily the same for put and call options on the same underlying asset and strike price. Implied volatility is different for puts versus calls, influencing the amount of extrinsic value subject to theta decay. Traders look at “skew” to identify volatility differences between strike prices. Interest rates impact theta calculations and could affect puts/calls differently based on individual risk-free rate inputs. The prices of the put and call is not equidistant from the strike price. This non-symmetry impacts moneyness and theta.

The most common cause of put/call theta differences is divergent implied volatility. Certain events like earnings announcements increase upside or downside volatility disproportionately, affecting put and call extrinsic value and related theta differently.

What are examples of Theta in Options Trading?

Let us look at three expamples of how theta is used in options trading.

A common way traders look to generate income is selling covered calls against stock positions they own. This involves selling call options on the stock to collect the premium income.

Theta comes into play because the trader wants the short calls to expire worthless due to time decay. The trader selects call strikes above the stock’s current price so the calls start out-of-the-money.

As time passes, the time value of the short calls erodes.The calls expire worthless if the stock price stays below the strike at expiration. The trader pockets the full premium as profit from the calls’ theta decay.

Maximising income relies on selling calls with higher theta. The trader compares multiple strike prices and expirations to identify the calls with the most rapid theta burn and highest premium income relative to the upside risk.

With credit call spreads, the trader sells high strike short calls to fund buying lower strike long calls. The result is a net credit position.

Profitability depends on the short calls expiring worthless. The trader selects strikes where the underlying is expected to trade below the short call strike at expiry.

The theta decay in the short call enables gaining income as time passes without the stock rallying above the short call strike. The trader analyses the theta levels of the short/long call strikes to optimise the rate of decay over the holding period.

For example, a trader sells an 80 strike call for Rs. 2 and buys a 75 strike call for Rs. 1. This creates a Rs. 100 credit.The trader makes Rs. 10 per day as the short call theta erodes its premium if theta is -0.10.

Iron condors involve selling an out-of-the-money put spread and call spread to create a net credit position. Profitability relies on the short put and call expiring worthless.

Since the iron condor has 4 legs, managing the theta across the spread is crucial. The trader wants to construct the iron condor so the short option legs have the highest theta, enabling them to decay faster relative to the long option legs.

Analysing the theta differences across the multiple options allows the trader to maximise the daily time decay toward the credit received. The trader also evaluates rolling the spread to continue capturing theta if the underlying remains within the expected range.

What are the advantages of Theta in Options?

Theta options have ten main advantages including the fact that it quantifies daily time decay rate, enable active decay management etc.

Quantifies daily time decay rate: Theta provides precise quantification of the daily time value erosion. Traders know exactly how much an option’s value is expected to decline based solely on the passage of one day.

Enables active decay management: Traders use theta to actively manage time decay through strategic entry/exit timing and strike price selection to either minimise or maximise the impact of theta on a position.

Opens non-directional strategies: Theta enables options strategies that solely rely on time decay without needing favourable directional moves in the underlying. Credit spreads, iron condors, and covered calls target theta.

Magnifies income potential: Selling options to capture theta allows collecting premium income from time value erosion over the trade duration. High theta options maximise this income generation.

Defines holding periods: Theta helps traders calibrate optimal holding periods. Shorter durations target higher theta, while lower theta allows longer-term holding.

Signals late stage trades: Accelerating theta signals the final month before expiration when active management is required to avoid heavy time value erosion.

Identifies mispricing: Comparing similar options’ theta reveals mispricing such as unusual time value discrepancies between put/call on same strike.

Manages early assignment: High theta warns of aggressive early option assignment risk before dividends or mergers.

Calculates cost of carry: Debit strategies face theta declining value over holding periods. Theta quantifies this time cost of carry.

Balances intrinsic value: Low theta signals high intrinsic and low extrinsic value. Helps balance intrinsic vs time value risk.

By quantifying the unavoidable time decay in options, theta provides invaluable signals for position management, relative value identification, income generation, and strategic strike price selection across a variety of options trading approaches.

What are the disadvantages of Theta in Options?

Theta has eight main disadvantages that roots from reason that it causes value erosion. Below are the right main advantages listed in detail.

Causes value erosion: Theta results in the inevitable erosion of an option’s value over time even without price moves in the underlying asset.

Requires active management: Positions with high theta require close monitoring and management to avoid losses near expiry as decay accelerates.

Limits holding periods: Traders forced to close positions earlier than desired to avoid theta accelerating into expiration.

Reduces probability of profit: Time decay lowers the chance that option positions will reach profitable price points before expiry.

Generates carrying costs: Debit strategies face theta working as a cost of carry over the holding period as value slowly declines.

Complicates planning: Theta acceleration near expiry makes it harder to precisely forecast value at future points in time close to option expiration dates.

Adds tracking complexity: Traders must constantly monitor theta across numerous contracts with differing expirations to optimise management.

Forces tradeoffs: Maximising theta often requires compromises between moneyness and days to expiration that limit optimal positioning flexibility.

Theta’s constant daily erosion of option value presents challenges requiring active mitigation through strategic trade sizing, timing, rolling, and strike price positioning. Traders must maintain vigilant focus on theta management across option portfolios to counteract its pernicious effects.

How fast does Theta decay?

Theta erosion gets faster exponentially as the option gets closer to expiration. The rate of theta decay speeds up in the last month before expiry, and very rapidly in the final two weeks.

This effect is seen visually in theta decay curves, which show the progression of how theta declines over the lifetime of an option contract. The curves demonstrate an exponential acceleration downward as expiration nears.

This accelerating pattern occurs because the greatest amount of uncertainty, and hence time value, exists the further out an option is from expiry. As expiration approaches, uncertainty declines parabolically, causing extrinsic value to decay at an increasing rate.

The precise theta at any given point depends on prevailing implied volatility levels in addition to time left to expiry. Higher volatility means greater time value subject to theta erosion. However, the general exponential acceleration pattern persists regardless of volatility conditions. theta exhibits the strongest nonlinear behaviour in the last 30-45 days to expiration.

One day’s theta is technically only “locked in” once that day passes and a full 24 hours of decay occurs. Intraday option value movements depend on various factors like underlying price changes, volatility, etc. After hours, some theta erosion occurs from one day’s market close to the next open. But the bulk of observable theta decay comes during active trading hours as liquidity focuses price discovery.

Does Theta Decay on Weekends?

No, theta decay does not actually occur over the weekends when the markets are closed. Theta represents the estimated amount an option loses in value for each day that passes as time value decays over the option’s lifetime. However, theta only truly erodes when the option is actively trading.

Since options do not trade over the weekend when markets are closed, theta decay does not happen over Saturday and Sunday. The next Monday opening prices will reflect two days of elapsed time, but only one day worth of actual theta decay from Friday’s close to Monday’s open.

This effect is also seen around market holidays. For example, with a holiday on Thursday and no trading Friday, the Monday opening will capture 3 days of time value erosion. But theta decay still only applies to the two trading days – Wednesday close to Monday open.

Does a higher Theta mean a faster option value decline?

Yes, a higher theta value usually does indicate a faster expected rate of decline in an option’s value due to time decay. Theta specifically represents the estimated amount an option is expected to lose in value for each day that passes as time value decays towards expiration.

Higher negative theta values, for example -0.10 versus -0.05, equate to a larger anticipated erosion of premium per day from the passage of time. Traders look at theta values to gauge the “speed” of time decay priced into a given option contract. The higher the absolute value of negative theta, the more rapidly the option’s value should decline on average each day, all else equal.

While underlying price moves outweigh theta impact in the short run, over the full lifetime of an option, higher theta implies more aggressive time value erosion.

What is the difference between Theta and Gamma in options trading?

Theta and gamma are two important risk metrics in options trading, but they differ significantly in what they represent.

Theta is the estimated amount an option contract loses in value for each day that passes due to time decay. Theta quantifies the erosion of time value as expiration nears. Gamma is the rate of change of an option’s delta. Gamma indicates how much delta itself changes in response to moves in the price of the underlying asset.

Theta focuses strictly on time sensitivity as it isolates the impact of time decay alone on an option’s value. It does not depend on price moves. Gamma focuses on price sensitivity. Gamma measures sensitivity to changes in the underlying price. It does not directly involve time decay.

Theta is always negative. It indicates declining option value from time erosion. Gamma is either positive or negative. Gamma values are typically smaller vs. theta. Gamma measures second order sensitivities while theta is primary sensitivity.

As expiration nears, theta exhibits exponential decay. Gamma impact remains more consistent over time. Theta becomes irrelevant at expiry. On the expiration date itself, only intrinsic value remains; theta cannot decay further. Gamma remains relevant into expiry.

Previous Article

Previous Article

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 34")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 35")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 36")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 40")

No Comments Yet.