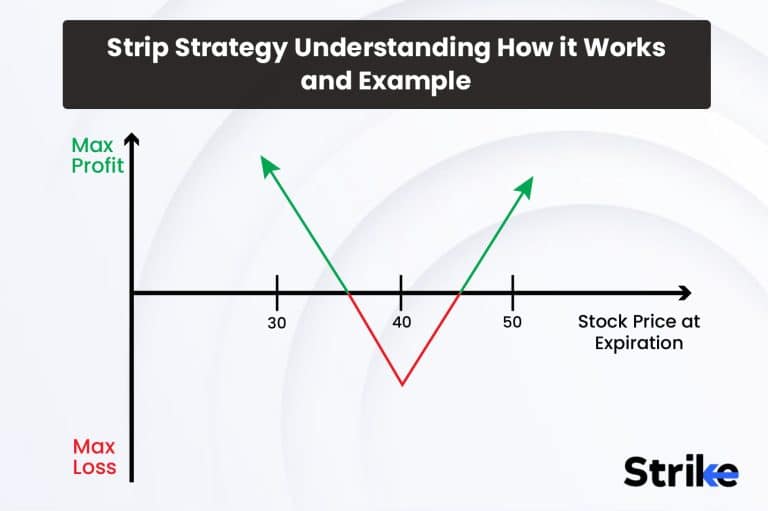

The strip strategy, also known as a strap strategy, is an options trading approach that involves buying both a call and put option with the same expiration date and strike price. Strip strategy creates a position that combines both long call and long put options. The goal is to profit from high volatility while minimizing the impact of the direction of the underlying asset’s price.

The strip strategy benefits from an increase in implied volatility. It aims to capture gains from the rise in the value of both the call and put options. The maximum loss is limited to the net premium paid for the options. The profit potential is unlimited to the upside if volatility rises sufficiently. The strip strategy allows traders to isolate and capitalize on volatility movements while remaining neutral on the directional outlook.

What is the Strip strategy?

The strip strategy, also known as a strap strategy, is an options trading approach designed to profit from rising implied volatility. It involves simultaneously buying both a call option and a put option on the same underlying asset with identical strike prices and expiration dates. This creates a long straddle position that combines both long call and long put options.

The goal of the strip strategy is to isolate and capitalize on increases in implied volatility while remaining directionally neutral on the underlying asset. Since higher volatility typically results in higher options premiums, owning both call and put options can lead to gains as volatility rises. The combined premium value of the long call and put tend to increase together when volatility goes up.

The maximum potential loss on a strip strategy is limited to the net premium paid to purchase the call and put options. The maximum profit is unlimited if volatility rises high enough to sufficiently lift both the call and put option values. The underlying asset’s price can move anywhere above or below the strike price without incurring additional losses beyond the original premium outlay.

The strip strategy is often used when a trader expects a major volatility event but is uncertain about direction. Earnings reports, economic data releases, and other binary events can cause sharp surges in implied volatility. Since the long call and put offset each other directionally, the trader isolates the volatility exposure. The strip strategy benefits from non-directional volatility expansion around the strike price chosen. Proper position sizing and risk management are key to utilizing this strategy successfully. The strip strategy is a purely volatility-focused trade that neutralizes directional bias.

Is the Strip Strategy similar to the Long Straddle strategy?

No, the Strip strategy and Long Straddle strategy are not similar. There are important differences between the two.

The Strip strategy involves buying an out-of-the-money put and selling an out-of-the-money call. This creates a range or strip between the strike prices where the trade can profit. The Long Straddle is different – it entails buying both an at-the-money put and an at-the-money call.

Rather than establishing a price strip, the Long Straddle seeks to profit from a larger move outside of the strike prices in either direction. The strip has defined risk, while the straddle has unlimited risk if the asset price moves significantly up or down.

The breakeven points also differ. For the Strip strategy, the breakevens are the strike prices of the put and call. The trade gains as long as the asset price is between the strikes at expiration. For the Long Straddle, the breakevens are above and below the strike price by the amount paid for the straddle. A larger move above or below the strike price is needed to profit.

While the Strip strategy generates income from the call sale to offset the put purchase, the Long Straddle requires paying premiums for both options. The strip has a lower net cost to establish than the straddle.

The risk/reward profiles differ as well. The Strip strategy has a variable payoff within the price strip resembling a long stock position. The maximum gain is capped at the call strike. The Long Straddle has uncapped profit potential above and below the strike prices. The risk is also different – the strip has defined risk limited to the net debit paid. The straddle has unlimited downside risk below the put strike.

In terms of expectations, the Strip targets range-bound price action or modest directional moves. The focus is on profiting within the boundaries. The Long Straddle relies on larger volatility in either direction to drive the asset price outside the straddle’s wings.

Finally, the strip is often held to expiration to attain maximum gain. The straddle is more often traded earlier to capture volatility spikes. The strategies employ different timing considerations.

How does the Strip strategy work?

The Strip strategy aims to profit within a price range determined by the strike prices of a long put and short call position. It works by utilizing these options to form boundaries where the trade acts similarly to owning the underlying asset while limiting the risk.

There are five key steps to implementing a Strip strategy.

First, identify range-bound price expectations: The Strip aims to generate gains from relatively stable or consolidating price action. Technical and volatility analysis identify situations where prices are likely to remain range bound or move modestly in one direction without major swings. The strip works best when markets lack clear directional bias.

Second, select appropriate strikes: Appropriately setting the put and call strike prices defines the price strip. Typically, choosing strikes out-of-the-money but reasonably close to the current asset price creates a realistic range. The put strike represents the maximum downside, and the call strike sets the upper limit before profits begin decreasing. Wider strips cost more but allow greater price movement. Narrower strips are less expensive but have less room before hitting the break-even points.

Third, buy put, sell call simultaneously: Executing the put and call legs together initiates the Strip position. Selling the call generates premium income to offset some of the debit required to purchase the put. The net cost represents the maximum loss if both options expire worthless.

Fourth, manage position over time: As time passes, the strip may be adjusted to retain the protective put or roll the call strike higher/lower depending on price action. Widening or narrowing the strip changes the range of prices captured. The goal is to keep the asset price within the strip to expiration.

Fifth, close at expiratio: The Strip strategy typically holds both options to expiration to maximise gains. At expiration, if the asset price is within the strip, the put expires worthless, while the call premium is retained as profit after covering the initial debit. The put is exercised, and the call expires worthless if the price falls below the put strike.

Within the strip boundaries, the payoff resembles a long position in the underlying. Below the put strike, losses are limited to the amount paid for the strip. Above the call strike, some upside is sacrificed, but net gains are still possible up to the call strike. This defined risk/reward profile makes the strip attractive for directional exposure.

Here is an example of how a Strip strategy might work.

Stock XYZ is trading at Rs. 50 currently. After analysis, a trader determines prices are likely to remain between Rs. 48 and Rs. 53 over the next two months.

The trader buys a 2-month 48 put for Rs. 2 and sells a 2-month 53 call for Rs. 1, establishing a Strip between 48-53 for a net debit of Rs. 1.

Over the next 6 weeks, XYZ fluctuates between Rs. 49 and Rs. 52, remaining inside the strip.

At expiration, XYZ closes at Rs. 51. The 48 put expires worthless, while the 53 call premium is profit. The trade gains Rs. 1 – the difference between the Rs. 2 call sale and Rs. 1 put purchase.

This example shows how the strip allowed benefiting from XYZ’s price movement within the range while strictly defining maximum loss. The boundaries provided directional exposure under Rs. 53 and downside protection below Rs. 48 for a net Rs. 1 outlay.

How important is the Strip strategy in Options Trading?

The Strip strategy occupies an important niche within options trading strategies. While not necessarily the most widely used technique, the strip serves key purposes that make it a valuable addition to a trader’s repertoire in the right situations. Seven reasons why the Strip strategy is an important options tool are the following.

Flexibility: The Strip provides flexibility in crafting risk/reward profiles to match a trader’s market outlook and risk tolerance. Varying the strike widths and quantities used allows customising the range of prices captured. Wider strips widen the profit zone but cost more. Narrower strips are more affordable but have tighter breakeven. The adaptability makes Strips useful across diverse trading plans.

Range Trading: The Strip strategy is uniquely designed for range bound or consolidating markets. Many options strategies rely on volatility or directional moves. Strips allow traders to benefit from prices oscillating within predictable boundaries rather than swinging widely above/below. This tactical edge makes Strips valuable when range trading.

Limited Risk: The long put in a Strip strategy strictly defines maximum loss, while allowing uncapped profit potential up to the short call strike. For traders uncomfortable with unlimited risk in long stock or call option positions, the strip provides directional exposure with peace of mind from defined downside risk.

Cost Efficiency: Selling the call to fund buying the put lowers the net debit required to establish a Strip position versus owning the stock outright. This structure offers efficient use of capital to achieve directional market exposure under the call strike at a lower cost than buying the equivalent number of shares.

Hedging: The protective long put provides insurance against declines below its strike price. This hedge element allows Strip strategies to be incorporated into portfolios or long stock holdings to guard against market corrections. The hedging ability increases the utility of Strips.

Simplicity: The Strip structure of a long put plus short call is straightforward and accessible even for newer options traders. The easily visualized risk graph and defined profit zone simplify the application. The relative simplicity makes Strips a good introductory multi-leg strategy.

Sensitivity Management: Once established, Strips are sometimes adjusted to mitigate time decay or optimize exposure. Rolling the call strike, widening the strip, or modifying the position structure allows for managing the trade’s sensitivity to changing conditions. This adaptability enhances the strategy’s usefulness.

How commonly do Traders use the Strip strategy?

The Strip strategy is not one of the most widely used options trading techniques overall, but it does see meaningful application among certain types of traders and within specific strategies.

Novice Traders: Strips serve as an introductory multi-leg options trade for newer traders. The straightforward structure of buying a put and selling a call is easy to visualize and comprehend. The clearly defined risk parameters and directional exposure also lend themselves to educational purposes. These factors make Strip strategies a relatively common starting point for options newcomers.

Directional Traders: For traders looking to express directional views with limited downside risk, Strips are preferable to simply buying calls or stock alone. The long put creates built-in protection while the call sale lowers cost. Directional traders unable to stomach the open-ended risk of long calls or stock may turn to Strips for efficient exposure.

Income Traders: The short call leg of a Strip generates premium income that is attractive for options income strategies. The call sale offsets the put purchase debit, lowering the cost of the position. The income helps achieve directional exposure for less capital outlay. Income-oriented traders find utility in Strips to monetize option time decay.

Range Traders: Strip strategies are especially popular among range-trading options strategies. The clearly defined upper and lower profit boundaries make Strips ideal for capitalizing on consolidating or oscillating price action. Technical traders adept at identifying support/resistance levels where prices are likely to remain range bound often utilise Strips in their trading.

Portfolio Hedgers: Investors seeking to hedge portfolios or long stock positions without completely eliminating market exposure will sometimes use Strips. The protective put limits the downside, while the short call offers partial funding. Strips allow maintaining partial upside exposure despite hedging the downside.

Retail/Individual Traders: Strip trades appeal to retail traders’ preferences for straightforward strategies with defined risks. Their directional exposure and limited downside align well with many individuals’ risk tolerances. Though institutions utilize more complex strategies, Strips find popularity in the retail world.

How to create a Strip strategy?

Constructing a Strip strategy involves a few key steps.

1. Identify Market Outlook

- Analyse technical indicators to determine if the market is trending or range-bound. Strips perform best in range-bound or moderately bullish markets.

- Examine volatility metrics like historical volatility to gauge expectations for consolidation or directional swings. Lower volatility environments suit Strips.

- Form a view of the asset’s expected trading range over the desired timeframe. This helps select appropriate strike prices.

2. Choose Strike Prices

- Select a strike below the current underlying price, targeting support levels or downside price objectives.

- Pick a call strike above current prices, aiming for near-term resistance or upside targets.

- Really, strikes will be reasonably close to the money but still out of the money. This balances premium costs versus setting wider strips.

- Wider strike separation increases the cost but allows greater price movement within the boundaries.

- Narrower spreads cost less to initiate but provide tighter buffers before hitting breakevens.

3. Determine Position Size

- Consider account size, risk tolerance and capital allocation to determine appropriate trade size.

- Bigger position sizes increase profit potential but also risk. Start small when first implementing Strips.

- Strips allow greater exposure with less capital than buying stock outright due to funding from call sales.

4. Place Orders for Put and Call Legs

- Enter the orders simultaneously to initiate the long put and short call together as a package.

- Legging into Strips sequentially sometimes exposes the trade to timing risks.

- Use combo/spread orders if available to enter both sides in one trade ticket.

5. Manage Trade Over Time

- Monitor price trends relative to strip boundaries. As needed, adjust strikes or size to retain favorable risk/reward.

- Widen strips by rolling call strike higher or put strike lower if more range leeway is desired.

- Close call early to lock profits if asset price moves below put strike, converting to long put position.

6. Hold to Expiration

- Ideally, maintain Strip position through expiration to maximise gains.

- Benefits are maximized by asset price closing within strip boundaries at expiration per the original strategy intent.

Strip construction involves matching technical outlooks, smart strike selection, appropriate position sizing, paired entry, active management, and holding through expiration when able. Proper crafting and execution of the Strip legs promote achieving the desired risk-managed directional exposure.

Is it expensive to set up a Strip strategy?

No, Strip strategies are generally inexpensive to establish compared to other options strategies or outright purchasing the underlying asset. There are five reasons why Strip setup costs are low.

Premium Funding: The proceeds from selling the call option help fund buying the put. This offsets some of the debit required to purchase the put, lowering the net cash outlay. Essentially, the short-call premium subsidizes the long-put position.

Out-of-Money Strikes: Strip strategies often utilise out-of-the-money strikes which carry lower premiums than at or in-the-money options. The lower premiums on the put and call legs keep costs down.

Less Capital Intensive: Strip strategies provide exposure similar to owning the asset outright but require less upfront capital. The defined risk parameters allow controlling a large dollar amount of the underlying for a smaller cash trade size.

No Margin: Since Strips open both a long and short option, there is no margin requirement. This avoids financing costs that leveraged stock buying would incur.

Customizable Cost: Wider strips with greater separation between the put and call strikes allow more price movement at the expense of higher premium costs. Narrower strips cost less but have tighter risk parameters.

When to enter a Strip strategy?

Identifying the right conditions to deploy strip strategies is crucial to maximizing their profit potential. The best times to enter strip trades include the following.

Periods of Low/Declining IV: With IV falling, option premiums grow cheaper, lowering the cost to establish strips. Low IV also signals diminishing volatility ahead, ideal for range-bound strips.

Trading Near Support/Resistance: Key technical levels on the chart suggest the stock may oscillate between zones rather than trending. Strips perform well in channeling price action.

Earnings Announcements Approaching: Uncertainty spikes before earnings as investors avoid directional bets. Post-earnings range-bound action is common.

Indexes/Sectors Rotating: Rotation between indexes and sectors indicates swinging back and forth rather than a strong trend emerging.

Consolidation After Large Move: Markets digesting overbought/oversold moves often trade sideways, creating opportunity for strips once directional momentum stalls.

Curve or Term Structure Flattening: A flattening yield curve points to expectations of slower growth and uncertainty ahead, which is beneficial for non-directional strip trading.

Alternatively, entering strips too late increases risks and reduces profit potential.

High/Rising IV Environment: Higher volatility boosts option premiums across all legs, increasing debit costs and leading to larger losses if a breakout emerges.

Breaking Support/Resistance: Once key levels are breached, a new trend often emerges rather than range-bound action. Strips will underperform on trending moves.

Immediately Post-Earnings: Fast price swings are common as the market reacts to results. Range Bound expectations may be invalidated.

Start of Strong Trend: Strips function poorly if entered right as a strong bullish or bearish trend kicks off since they limit upside/downside profits.

Index/Sector Breakouts: Strips become misaligned without range-bound circumstances when indexes or sectors start to surge in one direction.

Steepening Yield Curve: A steep yield curve reflects expectations for accelerating growth and inflation – an environment less supportive of stagnant trading.

When to exit a Strip strategy?

Knowing the right time to exit strip trades is essential to locking in profits and avoiding unnecessary losses. Eight signs it may be time to exit a strip position include the ones mentioned below.

Reaching Profit Target: Once the trade reaches the predefined profit goal based on the maximum gain, it makes sense to close the position and pocket the returns. No need to be greedy beyond the planned upside.

Approaching Expiration: It’s usually best to close strips a week or more before expiration to avoid risks from assignment, volatility spikes, and illiquid options.

Increase in Implied Volatility: Rising IV indicates greater volatility ahead, which sometimes blows through the expected trading range and causes strip losses.

Breaking Support or Resistance: The predicted trading range may become invalid if important support or resistance levels are crossed, necessitating a stop loss.

Earnings Announcement Risk: Uncertainty from an upcoming earnings report could bring volatile moves outside the range. Better to exit before the event.

Lopsided Position: A directional move may have started if the put or call side has started to become significantly more profitable than the other leg.

Index/Sector Rotation: Evidence of indexes or sectors starting to trend higher/lower suggests oscillation is ceasing in favor of a directional bias.

Loss Reaches Predefined Stop: Respecting stop loss levels preserves capital rather than hoping for the trade to recover.

Alternatively, holding onto strip positions for too long is costly if conditions change. Six of the risks include the following.

Missing Opportunity: Continuing to hold during a breakout wastes a chance to lock in larger gains from directional options positions.

Expiration Volatility Spikes: Surges in IV into expiration sometimes blow through wings and multiply losses.

Trapped in a Losing Position: Hope should not replace discipline. Letting losses run too deep cuts into capital.

Assignment Risks: Holding short options too close to expiration raises the chances of early exercise and delivery obligations.

Liquidity Dries Up: Thin trading on expiring options makes rolling or adjusting positions more difficult.

Opportunity Cost: Keeping capital tied up in stagnant strip trades prevents allocating toward better opportunities from arising.

How does implied volatility influence the Strip strategy?

Implied volatility represents the market’s expectation for volatility of the underlying security over the life of an option contract. It is derived from the current option premiums in the market and illustrates the annualised expected price movement. Higher implied volatility translates to greater expected volatility and more expensive option premiums.

Implied volatility significantly impacts the pricing and attractiveness of Strip strategies. Seven key influences are explained below.

Higher implied volatility makes put options more expensive since the market is pricing in greater odds of downside volatility. More expensive puts increase the debit cost to establish long put positions in Strips.

Higher implied volatility also raises call premiums as greater upside volatility is expected. More expensive calls mean less credit received for short-call sales used to fund long-strip puts.

The net effect is higher implied volatility increases the net debit required to construct new Strip positions. The greater cost makes Strips less efficient.

Conversely, lower implied volatility reduces the premiums of puts and calls as the market foresees less volatility risk. Cheaper puts decrease the debit cost of Strip setups. Higher call credits further reduce net cash outlays.

Lower implied volatility is beneficial for Strip strategy efficiency and cost effectiveness. The lower premium expense allows position sizes to be increased for the same capital outlay.

Since Strips involve both long puts and short calls, they exhibit negative vega overall – meaning they are structured to lose value if implied volatility rises after entry. Rising IV boosts put premiums but hurts call income, eroding Strip value.

Falling implied volatility after Strip entry is beneficial, enhancing value by reducing put costs faster than call income. Strips gain from falling IV environments.

Higher implied volatility works against Strip strategies by increasing the net cost to establish new positions and reducing potential value. Lower IV reduces setup costs and creates positive vega exposures if IV declines further.

Careful Strip construction when IV ranks near the low end of historical levels provides an edge. Monitoring implied volatility trends intra-trade spotlights helpful timing for adjustments or exits to maximise value.

What is the impact of time decay on the Strip strategy?

Time decay, or theta, measures the rate of decline in an option’s value towards expiration due to the passing of time. The impact of time decay on Strip strategies contains nuances:

On the short call leg, time decay is beneficial to the Strip trader. As time passes, the value of the call decays which allows repurchasing it at a lower price to close the position. The quicker the call premium deteriorates, the better for the strip.

However, on the long leg, time decay harms the strip. As the put loses value over time, it provides less downside protection. Faster time decay erodes this key risk management aspect of the trade before expiration.

Since Strip strategies have a net short options bias from the short call, overall time decay provides a modest positive impact on the total position value. However, this is sometimes misleading.

While the short call decays favorably, the diminishing put protection over time leaves the trader exposed to growing downside risk as the expiration date approaches.

Having a severely degraded put hedge from theta might result in significant losses even as the call decays towards worthlessness if the asset price drops significantly near expiry.

Rolling the long put leg out further in time before too much decay occurs helps maintain downside protection as expiration nears. This helps rebalance the total time decay effects.

While the net short theta exposure from the short call creates modest positive time decay, the declining put protection over time poses a threat. Careful management of the put leg is required to retain hedging as expiration approaches.

The ideal scenario is for the asset price to remain within the strip boundaries as both the put and call bleed value from theta. Letting both options mostly decay out-of-the-money leads to maximum profits. But the trader must be vigilant of accelerated put time decay, exposing the downside before expiration arrives.

On balance, Strip traders aim to benefit from short call time decay but must actively mitigate the negative impact of long put time decay to avoid expiration exposure. Thoughtful management of both sides allows collectively harnessing theta’s advantages.

How to hedge the risks associated with a Strip strategy?

The primary risks of strip strategies include volatility expansion, trend breakouts, and early assignment on the short call. Traders use hedging strategies, such as the 10 listed below, to reduce these risks.

Leg In Gradually: Build the strip position in stages rather than all at once. This allows time to reevaluate conditions between adding legs.

Use Wider Strikes: Buying further OTM call/put wings provides more cushion against volatile price swings.

Purchase Longer Dated Options: Choosing back-month expiries gives more time for the expected range-bound action to play out.

Trade Smaller Size: Right-sizing strips to a small portion of the portfolio limits damage if the trade moves against the trader.

Set Stop Orders: Automatically exiting strips at predefined loss levels contains drawdowns before losses accumulate.

Hedge With Low Correlation: Consider pairing strips with negatively correlated products like bonds to diversify risk.

Buy Protection: Buying cheap OTM put protection below the strip’s put wing protects against downward trending action.

Collar With Covered Call: Holding the stock and overlaying a covered call hedges upside risk if assigned early on the short call.

Barbell Strikes: Constructing a barbell strip with wider outer strikes reduces probability of breakouts breaching the range.

Calendarize Wings: Using back-month options for the wings provides more time for the expected trading range to play out.

Proper position sizing is also key for risk control. The maximum loss on a strip should represent a small percentage of overall capital. This minimizes the portfolio impact if the trade loses money.

Setting clear loss limits and acting quickly once those levels breach aid in defending the capital. Traders should avoid rationalizing or hoping losing strips recover. Timely hedging and mitigation responses are essential.

How to make adjustments to a Strip strategy?

The most common adjustments for strip trades involve responding to trend breakouts volatility changes, and defending against early assignment on the short call. Eleven adjustment tactics include the following.

Roll Short Call Down: Close the short call and sell a fresh call at a lower strike to earn an additional premium if the stock falls below the lower end of the range.

Roll Short Call Up: Close the short call and sell a fresh higher strike call to generate more money if the stock rises over the top end of the range.

Roll Long Wings Closer: Close the long wings and repurchase at closer strikes to lower cost basis if volatility decreases.

Roll Long Wings Further Out: Close the long wings and repurchase at farther OTM strikes to increase the range if volatility increases.

Repair With Ratio Spread: Sell more OTM calls at higher strikes if an upward breakout occurs in order to pay for more call protection that is payable if an upward breakout occurs.

Defend With Covered Stock: Buy shares of the underlying stock to limit your exposure to the gain if the short call’s early assignment risk exists.

Manage Time Decay:- Close the short call early and sell a fresh one at a higher strike to increase your revenue if IV rankings are very low.

Protect With Stop-Loss:- Set a stop-loss order to automatically cancel positions if losses surpass the maximum risk amount if the strip value declines.

Size Position: Reduce the size of your strip positions as volatility uncertainty rises to lessen your exposure to loss.

Hedge Delta: To maintain delta neutrality if strip deltas fall out of balance, trade stocks or futures.

Leg Out Early: Leg out of each position individually before expiry if technicals deteriorate to maximize exit pricing.

The key is monitoring conditions continuously for signs of degradation and being proactive in adjusting. Letting losses build up before responding magnifies downside. Disciplined adjustments preserve capital and let profits run.

Adaptability and vigilant management are critical with strips. Traders must judge when adjustments make sense versus simply exiting and redeploying capital elsewhere. The strip’s sound structural risk control provides flexibility to modify trades reactively. Executed prudently, adjustments become an active risk management tool.

What is the breakeven point for the Strip strategy?

The breakeven point for a strip strategy is the underlying stock price at which the trade breaks even or has zero profit/loss. It is calculated as stated below.

Breakeven = Strike Price of Sold Call + Net Debit

For example, if a trader sells an at-the-money 50 strike call for a net debit of Rs. 2, the breakeven point would be as stated below.

Break Even = Rs. 50 (sold call strike) + Rs. 2 (net debit paid) = Rs. 52

The sold call expires worthless, and the long put finishes in the money if the stock is below Rs. 52 at expiry, allowing the transaction to break even. Above Rs. 52, the assignment on the short call kicks in and creates a loss.

The breakeven point is a useful metric for evaluating the viability of a strip trade. Wider breakevens provide more room for the stock to fluctuate within the profitable range. The probability of profit increases when the distance between the breakeven and wings is greater.

Traders want to see the stock hold within the breakeven and wings at expiration to maximise the chance of profit. Time decay, lowering the breakeven over the life of the trade, is also favorable. The goal when constructing strips is to ensure breakevens align with the expected trading range.

What is the maximum profit for the Strip strategy?

The maximum profit potential for a strip strategy is capped and determined by the following formula.

Maximum profit = Strike of Long Call – Strike of Long Put – Net Debit

For example, if a trader buys a 40-strike put, sells a 50-strike call, and buys a 60-strike call for a net debit of Rs. 2, the maximum profit would be as stated below.

Max Profit = Rs. 60 (long call strike) – Rs. 40 (long put strike) – Rs. 2 (net debit) = Rs. 18

This Rs. 18 represents the trader’s maximum possible profit if the stock finishes between the put and call wings at expiration.

At that point, the 60 strike call expires in-the-money with Rs. 10 of intrinsic value. The 40 strike put also expires in-the-money with Rs. 10 of intrinsic value. Meanwhile, the sold 50 strike call expires worthless, allowing the trader to keep the entire premium collected.

The combined value of the long call and put legs less the net cost to enter the trade determines the maximum gain. This defined upside cap contrasts with spreads where maximum gains equal the distance between strike prices.

The key factor impacting potential profit is the width between the bought call and put. Wider distances allow for greater maximum gains before transaction costs. However, it also increases the net debit required to establish the position.

Traders calculate maximum profit scenarios when analysing new strip opportunities to ensure the potential payout adequately compensates for the defined risk taken. Assessing this risk-reward tradeoff helps determine proper position sizing as well.

What is the maximum potential loss for the Strip strategy?

The maximum potential loss on a strip strategy is equal to the net debit paid when entering the trade. Here is an explanation of how the maximum loss is calculated.

A strip strategy involves buying an out-of-the-money (OTM) call, selling an at-the-money (ATM) call, and buying an OTM put. The net debit represents the difference between the total premium collected from the short call and the premium paid for the long call and put options.

For example, if a trader buys a 40-strike put for Rs. 2, sells a 50-strike call for Rs. 5, and buys a 60-strike call for Rs. 3, the net debit would be as follows.

Rs. 2 (Long Put Premium) + Rs. 3 (Long Call Premium) – Rs. 5 (Short Call Premium) = Rs. 0 Net Debit

Since the short call premium exceeds the combined cost of the wings, this creates a net credit received rather than a debit paid.

The maximum loss occurs if the stock settles outside the strip’s boundaries at expiration. In that case, the short call and long put or call expire worthless, while the other wing retains a small amount of intrinsic value.

However, after factoring in the net debit or credit from initiating the trade, the position nets to the maximum loss amount. Here, with a net credit received, the total loss is simply the original credit taken in.

Key Advantages of Strip Strategy Maximum Loss:

- Risk is strictly limited and predefined at entry.

- Loss is generally small relative to potential profit.

- Enables prudent position sizing based on fixed risk.

Maximum loss on a strip trade is not dependent on the strikes selected or stock movement. It is solely the net cost paid, or credit received when putting on the trade initially. Defining strict risk parameters is a key benefit of the strip strategy.

What are examples of Strip Strategy?

Here are two examples illustrating the use of Strip strategies.

1: Range Bound Stock

A trader identifies XYZ stock trading between support at Rs. 50 and resistance at Rs. 60. IV is low and technicals suggest continuing range bound action. They implement a Strip buying the 50 put for Rs. 2 and selling the 60 call for Rs. 1. The net debit is Rs. 1 per contract.

Over the next 6 weeks, XYZ oscillated between Rs. 52 and Rs. 58, finishing at Rs. 55 at options expiration. The 50 put expires worthless, while the 60 call premium decays to zero by expiration.

The strip creates a Rs. 1 profit since the Rs. 1 call sale exceeds the Rs. 2 put buy. The range-bound movement allowed benefiting from owning XYZ below Rs. 60 for just a Rs. 1 outlay. The Strip strategy functioned as intended.

2: Index ETF Strip

A trader forecasts the S&P 500 index trading in a consolidation range after a sharp selloff. They buy a 3-month put on the SPY ETF with strike Rs. 275 for Rs. 4 and sell a 3-month Rs. 285 call for Rs. 2.

The net debit entry of Rs. 2 establishes a Strip with Rs. 275 downside protection and upside profits up to Rs. 285. For two months the S&P pivots between weak rallies and retests of the low, remaining range bound.

As expiration approaches with SPY at Rs. 280, the trader closes the short call option to lock in a Rs. 2 profit and remove upside risk. The long Rs. 275 put expires worthless.

The strip allowed benefiting from the index ETF trading in a range for minimal cost. Closing the short call early secured gains from the established trading strip.

Why use a Strip instead of a Straddle?

Strip and Straddle strategies both aim to profit from significant price movement in the underlying asset. However, Strips have six advantages that may make them preferable in certain situations.

Defined Risk

The long put in a Strip establishes a defined maximum loss limited to the net debit paid. A Straddle involves buying a put and a call, exposing the trader to unlimited risk if the stock moves strongly up or down.

Lower Cost

Selling the call in the strip offsets the put purchase debit, reducing the capital outlay. Straddles require buying both sides, increasing the premium cost.

Uncapped Profit Potential

Strip profits are not capped on the upside until the short call strike price. Straddles cap profits at the breakeven points.

Higher Probability

A Strip benefits from low volatility range-bound action, which occurs more frequently than the explosive moves a Straddle requires.

Flexibility

The strip’s short-call revenue allows modifying the structure into spreads or collars. The straddle is less flexible since both legs are purchased.

Convexity

The strip’s short call creates positive convexity, giving larger exposure to the upside while limiting the downside. The straddle’s linear payouts have lower convexity.

The strip’s natural structural advantages, including defined and lower risk, uncapped upside potential, higher probability market scenarios, increased flexibility, and convex payouts, make it an attractive alternative to Straddles in the right situations.

Is Strip Safer than Straddle Strategy?

Yes, the Strip strategy is generally considered safer than the Straddle strategy. There are three key reasons why this is the case.

Defined Risk

The Strip strategy has defined limited downside risk capped at the net debit paid to establish the position. The long put provides downside protection and defines maximum loss exposure.

In contrast, the Straddle strategy has unlimited risk, as buying both a put and call means large losses sometimes occur in both directions. The straddle lacks an inherent loss limit like the strip’s long put.

Lower Cost

The Strip strategy involves selling a call option, which generates premium income to offset some of the put purchase cost. This lowers the capital outlay and cash tied up in the trade.

Straddles require buying both the put and call outright, increasing the overall cost burden and capital requirements. The greater cash allocation raises risk.

High Probability

Strip strategies benefit from range-bound, low-volatility market environments that occur frequently. The straddle relies on large, volatile directional price swings that materialize less often.

What are the advantages of the Strip strategy?

Here are the five main advantages of using the Strip options strategy.

1.Defined and Limited Risk

- The long put leg of the strip defines maximum potential loss, capping downside risk exposure to the net debit paid.

- Buying the put creates an inherent hedge that limits losses if the stock falls.

- Defined and contained risk provides greater control than unlimited risk strategies.

2. Lower Cost Structure

- Selling the call option generates premium income that offsets some of the debit to buy the put.

- This lowers the net cash outlay required to establish the Strip position.

- More affordable entry cost allows for allocating capital efficiently.

3. Uncapped Profit Potential

- Strip profits sometimes continue higher past the short call strike, up until stock assignment.

- No upside profit cap exists like with call credit spreads or other defined return strategies.

- Allows participating fully in upward trend moves beyond the short call strike.

4. Flexibility

- Strip structure allows modifying into spreads and collars to further refine risk parameters.

- Traders sometimes roll Strips wider or inverted to adjust to changing market conditions.

- Versatility in managing Strip strategies creates additional advantages.

5. Higher Probability Opportunities

- Strips perform optimally during low volatility range-bound environments that occur frequently.

- Strategies reliant on major breakouts have lower probabilities, which Strips avoid.

- Fitting more common market conditions gives Strips an edge.

The strip provides traders with an options strategy with built-in risk management, affordable entry costs, robust upside potential, structural flexibility, and scenarios catered to higher probability opportunities. The collection of advantages makes Strips an attractive choice under the right market outlook.

What are the disadvantages of the Strip strategy?

Here are five potential disadvantages or drawbacks associated with utilising the Strip options strategy.

1.Requires Accurate Forecast

- Strips rely on the stock staying within the price range defined by the put and call strikes.

- Losses may be more than anticipated if a breakout happens and the prognosis is off.

- Precise directional outlook is key, or Strips risk expiration out-of-the-money.

2. Time Decay Impacts

- Long-put time decay erodes downside protection as expiration nears.

- Requires active management to maintain hedge or roll put out in time.

- Unmanaged put time decay leaves the position unprotected on the downside.

3. Assignment Risk

- Short calls are at risk of early assignment if in-the-money with dividends approaching.

- Forced early call assignment would require unwinding the Strip position before planned.

- Monitoring dividends and managing assignments requires vigilance.

4. Unbalanced Greeks

- Strips have negatively skewed Greeks weight toward the short call.

- Vega, theta, and delta sensitivity primarily influence call side exposure.

- Sometimes, it creates challenges managing Greek risks on the put protection leg.

5. Capped Profit Potential

- Maximum gains are limited to the short-call strike price level.

- Upside truncated compared to just owning stock outright long-term.

- May miss large rally moves above the short call strike.

Strip strategies do carry disadvantages like forecast dependency, time decay management, assignment risks, unbalanced Greeks, and capped upside that require planning and awareness. Trading Strips successfully involves mitigating these drawbacks through strategic construction, active management, and risk monitoring. The drawbacks are successfully mitigated when they are adequately handled.

Is strip a bullish strategy?

No, the Strip strategy itself does not have a purely bullish or bearish directional bias. The strips are structured both ways to express different market outlooks.

The strip is somewhat bullish if it is built with a higher short call strike than a long put strike. The upside profit potential is greater to the call strike than the downside risk to the put strike.

For example, a Strip long the 50 put and short the 60 call is bullish from 50 to 60. The defined risk is lower than the uncapped return potential.

This structure benefits if the stock trends modestly upward or trades in a bullish range bound pattern during the options lifespan.

A bearish Strip is produced when the short call strike is below the long put strike. The downside protection exceeds the upside for a net bearish profile.

For example, a 60/50 Strip would be bearish overall. The put hedge offers larger exposure than the call upside.

This bearish structure wants the stock to trade mildly lower or consolidate in a bearish range between the strikes. The put offers greater leverage.

What is the difference between Strip and Strap?

Here is a comparison of eight key differences between the Strip and Strap options strategies.

The Strip strategy involves being long a put and short a call. The Strap strategy combines a long put and long call position, typically both at-the-money.

Strips use out-of-the-money put and call strikes to form a price range. Straps utilize at-the-money puts and calls seeking volatility expansion.

Strips have defined, capped risk limited to the net debit paid. Straps contain unlimited risk in both upside and downside directions.

The strip’s short-call credit income reduces net cost. Straps require paying premiums for both long sides, increasing cost.

The strip’s breakevens are the put-and-call strike prices. The Strap’s breakevens fall below and above the strike price by the amount paid.

Strips profit within the put/call strike range. Straps need larger breakouts past breakevens to profit.

Strips benefit from range bound environments that occur more frequently. Straps require rarer large volatile breakouts.

Strips often hold through expiration. Straps look to capture near-term volatility spikes earlier.

The key contrasts between Strip and Strap strategies include position construction, strike selection, risk parameters, cost factors, breakeven points, profit zones, probability, and intended hold duration. Understanding these differences allows traders to deploy the appropriate strategy for their market outlook, risk tolerance, and implementation objectives.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 28")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 29")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 30")

: Overview, 10 Types of Indicators, Settings for Different Markets 31")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

: How We Used This 70/30 Indicator in 6 High Win-rate Strategies 37")

No Comments Yet.