A put option is a type of options contract that gives the owner the right, but not the obligation, to sell a certain amount of the underlying Asset at a predetermined price called the strike price within a specified time period. Put options work the opposite of call options, which give the owner the right to buy at a specified strike price.

Put options allow investors to speculate on downward price movement or hedge their portfolio against a decline in a stock or index. The buyer of the put option pays a premium upfront to the seller for obtaining the right to sell the underlying at the strike price. The strike price is the predetermined price at which the buyer sells the Asset. Put options are “in the money” if the market price of the underlying falls below the strike price. At expiration, the buyer exercises the put option and sells the Asset at the strike price if the option is in the money. Put options that are not exercised by expiration become worthless. The maximum loss for the buyer is limited to the premium paid.

Put options provide insurance against downside risk in the underlying Asset. They allow investors to profit from declining stock prices or hedge existing long stock positions. Put options are used by investors to speculate on declining markets or individual stocks. Puts form part of trading strategies like covered puts, bear put spreads, protective puts, etc.

What is a Put Option?

A put option is a financial contract that gives the holder the right, but not the obligation, to sell an agreed quantity of an underlying asset at a predetermined price (the strike price) within a specified time period. The buyer of a put option is betting that the price of the underlying Asset will fall below the strike price before the expiration date. It is important to understand certain terms to understand the working of the put option.

The underlying Asset is the security or Asset that will be sold if the put option is exercised. It can be stocks, bonds, currencies, commodities, etc. Strike Price is the agreed price at which the holder can sell the underlying Asset if they exercise the put option. It is also called the exercise price.

Premium is the price paid by the buyer to the seller (writer) of the put option for the rights granted by the contract. It represents the maximum profit possible for the seller.

Expiration Date is the last date on which the put option can be exercised. If unexercised by this date, the contract expires worthless.

Contract Size refers to the quantity of the underlying Asset covered by a single options contract. For stock options, it is usually 100 shares.

A put option allows the holder to sell the underlying Asset at the strike price. It is a bearish strategy used to profit from a fall in the Asset’s market price or hedge an existing long position. The buyer pays a premium for this right.

Why is it called a Put Option?

The term “put” in the put option refers to the right granted to the option holder to “put” or sell the underlying Asset at the specified strike price prior to the expiration date. The buyer acquires the possibility to “put” the underlying Asset onto the option seller or writer by paying a premium for a put option if it is profitable to do so.

More specifically, the origin of the “put” terminology traces back hundreds of years. In the 1600s, the Dutch pioneered the trading of stock options that gave holders the choice to “put up” or deliver stock shares at a set price over a time period. This allowed speculation on falling stock prices. These original options were thus named “puts” because the buyer could “put upon” the seller the obligation to take delivery of shares if the stock fell below the contracted strike.

Some etymologists theorize the term “put” is derived from old English slang meaning “to put up with” or “to accept.” This referred to the option seller having to accept delivery of the stock from the buyer under the agreed terms. Another theory suggests that “put” options get their name from the action of the buyer “putting up” the premium fee to purchase the contract from the seller. In any case, The term “put” focuses on the option buyer’s right to “put” shares onto the seller and compels them to “put up with” buying the stock at the set strike price if exercised.

This name contrasts with a call option that grants the buyer the right to “call away” or purchase shares from the seller. So, the “put” and “call” terminology highlights which party initiates the underlying asset transfer if exercising the option is profitable.

The value of a put option stems from it granting this favorable “putting” right to the option holder. The put buyer only faces the known, limited risk of the premium paid to acquire the choice to “put” shares onto the seller at the strike price. Put options offer leveraged profit potential without needing to short-sell the Asset directly when the underlying security falls in value.

The “put” terminology reflects the nature of this one-sided arrangement favoring the option buyer. For a small premium, the buyer “put” considerable downside price exposure on the seller. The word “put” succinctly captures this transfer of potential obligation based on the relative future value of the underlying Asset.

How does Put Options work?

A put option works by giving the buyer the right, but not the obligation, to sell an underlying asset at a predetermined strike price prior to or on a specified expiration date.

The buyer of a put option pays an upfront premium to the seller and receives the right to sell shares of the underlying Asset at the strike price. The premium and strike price terms are agreed upon when the put option is traded.

The put buyer obtains possible downside protection by paying the premium in the event the asset price declines below the strike. The put option will have intrinsic value that is captured by exercising the put to sell shares at the higher strike versus the lower market price if the asset price falls below the strike at expiration.

For example, say a trader buys put options on XYZ stock with a Rs.50 strike price and Rs.1 premium per share.

XYZ falling to Rs.45 at expiration means the put buyer exercises the option to sell XYZ stock at Rs.50 rather than the market price of Rs.45, capturing Rs.5 per share of intrinsic value. After deducting the Rs.1 premium paid, this gives a net Rs.4 per share gain.

The maximum loss for the put buyer is limited to the premium paid. The potential profit is the strike price less the current market value of the shares when exercised. The put payoff at expiration is:

Profit = Strike Price – Stock Price – Premium

The seller (writer) of a put option receives the premium payment upfront from the option buyer. They take on the obligation to buy shares of the underlying Asset at the strike price by selling the put if the put buyer chooses to exercise the option.

So, selling a put option generates income from the premium but results in potential downside exposure if the asset price declines below the strike. The seller is “short” the put option and hopes for it to expire worthless, so they keep the full premium.

For example, using the Rs.50 strike put above, XYZ is trading for Rs.60 at expiration, meaning the put option would expire worthless since there is no intrinsic value. The put seller would profit from the full Rs.1 premium amount collected when initially selling the option.

The payoff for the put option buyer and seller at expiration depends on where the asset price is relative to the strike price.

Asset price > strike price – Put expires worthless. The buyer loses the premium paid. The seller keeps the full premium.

Asset price \< strike price – Put has intrinsic value. The buyer exercises the option to sell at strike. The seller has to buy shares at strike per contract.

Asset price = strike price – Put option expires worthless with zero value.

So, the put payoff profiles are opposite for buyers and sellers – buyers profit from falling asset prices, while sellers profit from rising prices.

The premium on a put option, in addition to intrinsic value, also includes time value, which reflects the likelihood of the option finishing in the money based on the remaining time until expiration. More time remaining means a higher time value.

Additionally, higher implied volatility on the underlying Asset increases the put option premium because it indicates a wider potential distribution of returns and a greater probability of the put finishing in the money.

American-style put options allow early exercise before expiration if the option has intrinsic value. This is done to capture the intrinsic value earlier or to collect a dividend payment on the underlying Asset.

European-style puts cannot be exercised early and only have value at expiration if they are in-the-money based on the asset price versus the strike price.

What is the importance of the Put Option?

A major use of put options is to speculate on the decline of an asset’s price. The ability to purchase puts allows traders to profit from falling prices without needing to short-sell the underlying Asset. Speculating with puts offers defined and limited downside risk compared to shorting while providing leveraged returns if the asset price drops substantially. Puts are a critical tool for traders to implement bearish market views.

Put options are extremely important for hedging and mitigating portfolio risks. Buying puts against an existing long-term asset position provides insurance against declining prices. For example, an investor who owns shares of a stock purchase puts on that same stock to protect against the downside. Gains on the put offset losses on the stock holding if the stock price falls. Portfolio managers routinely use puts to hedge risks in equities, bonds, currencies, commodities, and other asset classes. It allows forPuts allow limiting drawdowns during market declines.

Selling (writing) put options generates income from the premium collected by the option seller. The premium provides compensation for taking on the obligation to buy the underlying Asset at the strike price if assigned on the short put at expiration. Put writing offers an income stream as the seller seeks to profit from the put expiring worthless due to the asset price remaining above the strike.

Put options provide an additional asset class to diversify an investment portfolio beyond just long positions. They produce profits during market downturns when most assets decline in value because puts gain value as the underlying drops. Including puts in a portfolio provides diversification since they offer returns that are inversely related or non-correlated to long positions in stocks, bonds, etc.

Compared to short-selling the underlying Asset directly, put options offer the possibility of leveraged percentage returns from a downward price move. Large gains are achievable with a small put premium investment if the asset price drops substantially below the option strike price at expiration. The built-in leverage effect makes puts attractive for speculators with limited capital.

The maximum loss on a put option purchase is limited to the premium amount paid for the option contract. The put buyer only loses what they invested initially, even if the underlying Asset becomes worthless. The defined and capped risk profile contrasts with shorting assets directly, where potential losses are theoretically unlimited. It allows for Puts to take bearish positions with minimal capital at risk.

Put options are sometimes customized with varied strike prices and expiration dates to match specific market views and risk parameters. Over-the-counter (OTC) offers complete flexibility in terms compared to standardized exchange-traded contracts. The ability to tailor puts to unique objectives makes them more useful and versatile trading vehicles.

Exchange-traded put options have become widely accessible to traders and investors. Online brokerages facilitate the cheap and efficient trading of puts. They do not require shorting, borrowing, or margin accounts. Transaction costs and commissions for puts are very low, making them feasible for retail traders and investors. Puts provide an easy way to gain bearish exposure without complexity.

What are the types of Put Options?

The two main types of Put Options are European Put Options and American Put Options.

1.European Put Options

A European put option is a financial derivative contract that gives the holder the right, but not the obligation, to sell the underlying Asset at a predetermined strike price on the expiration date. European puts cannot be exercised early and only have value at expiration if the asset price is below the strike.

European puts can only be exercised on the expiration date, not prior to expiration. This contrasts with American-style puts that allow early exercise. The specific date a European put option expires. This is the only day it is exercised. Expiry dates range from a few days to many months or years. The fixed price at which the put holder sells the underlying Asset if they exercise the option at expiration. Also called the exercise price. The upfront price paid by the buyer to the seller for the options contract. Factors like strike price, time to expiry, and volatility impact the premium amount. The number of units of the underlying Asset controlled per options contract. For stock options, this is usually 100 shares.

The buyer of a European put option profits when the price of the underlying Asset falls below the strike price at expiration. Exercising the put then allows selling the Asset at the higher strike price, capturing the intrinsic value.

For example, say a trader buys a 3-month put option on XYZ stock with a Rs.50 strike price for a Rs.2 premium. At expiration, XYZ is trading at Rs.45 means the put buyer exercises the right to sell XYZ at Rs.50 and make a Rs.3 per share profit. This offsets the Rs.2 premium paid.

The maximum loss on a long European put is the premium paid if the option expires out of the money. The maximum profit potential is the strike price less the asset value. The seller of a European put profits if the option expires worthless with the asset price above the strike at maturity. They keep the premium. The seller must buy the Asset at above market value if assigned at expiry with the Asset below the strike.

One major use is speculation, where traders buy puts to profit from anticipated downward moves in the underlying asset price. Another important use is hedging, as long as it protects against losses on existing asset portfolio holdings in the event that prices decline. Selling puts generates premium income but has downside assignment risk if exercised against at expiration. Buying puts allows volatility trading if implied volatility is relatively low and expected to rise. European puts also provide access to bearish positioning in assets or markets that are difficult or expensive to short. Downside protection is another key use, as long as it limits the risk of losses on a long stock position to the known premium paid.

There are various strategic uses of European puts in options trading. Long puts provide simple, direct bearish exposure with defined and limited risk. Protective puts involve holding long puts to hedge existing long positions in a portfolio or stock. A bear put spread entails selling a higher strike put and buying a lower strike put to profit from moderate declines. Risk reversals combine buying puts and selling out-of-the-money call options to hedge risks and are popular in forex trading. Put ratio spreads involve selling more puts at one strike than bought at a different strike and are delta-neutral. Put-back spreads consist of selling short-term puts and buying longer-term puts to profit from a downward move over time. Put calendar spreads, sell near-term expiration puts, and buy longer-term puts to monetize time decay.

The premium on a European put option is impacted by several key factors. Intrinsic value is the difference between the strike and current asset price if the option is in-the-money. Time to expiration also affects premiums, as more time value remaining means higher premiums. Higher implied volatility increases the value of puts due to the greater probability of finishing in the money. Finally, rising interest rates make puts more valuable by reducing the forward value of the underlying Asset.

2. American Put Options

An American put option is a financial derivative contract that gives the holder the right to sell the underlying Asset at the strike price at any time prior to expiration. American puts differ from European puts in that they are exercised early, not just at expiration.

American puts allow exercise at any point before and including the expiration date if the options are in-the-money. This early exercise creates opportunities and risks. The predetermined price at which the put holder sells the underlying Asset when exercising the option. Also called the exercise price. The date at which the put option expires. For Americans, this is the final date for exercise. The upfront price paid by the buyer to the seller to purchase the option contract. Factors like implied volatility impact premiums. The amount of the underlying Asset is controlled per option contract. For stock options, this is typically 100 shares.

The buyer of an American put option profits when the underlying asset price falls below the strike price either early or at expiration. Exercising the put then allows selling the Asset at the higher strike versus the lower market price.

For example, say an investor buys a 9-month American put on stock XYZ with a Rs.50 strike for a Rs.3 premium. XYZ falls to Rs.48 after 3 months, meaning the put is exercised early to capture Rs.2 per share of intrinsic value.

The maximum loss on a long American put is the premium paid if the option expires worthless. Profits are capped at the strike price, less the premium.

The seller receives the premium upfront but has an uncapped downside if the put buyer exercises with the Asset below the strike. Early exercise force assignment.

American put options have several key uses. They are purchased for speculation to profit from anticipated downward moves, with early exercise capturing intrinsic value sooner. American puts are also useful for hedging to protect against losses in the underlying Asset by exercising early to realize gains if the price drops. Writing American puts generates premium income but has the early exercise risk of having to purchase the Asset below market value. These options provide access to bearish exposure for assets or markets that are difficult or expensive to short. The leverage provided by American puts allows large percentage gains with a small premium investment if the asset price declines substantially below the strike. Buying puts enables volatility trading when implied volatility is expected to rise. Downside protection is another important use, as long as American puts limit risks on existing portfolio holdings with a known maximum loss amount.

American puts are used to structure various options trading strategies. Long puts provide outright bearish exposure to speculate or hedge. Protective puts involve holding long puts to hedge risks on current long positions or a stock holding. A bear put spread uses a higher strike sold put and a lower strike bought put to define risk while profiting from a moderate decline. A collar combines long puts and short calls to hedge risks on a long stock position within a price range. Married puts pair owning puts and stock to provide downside risk protection. Put ratio spreads sell more puts at one strike than bought at another and create a net credit. Put-back spreads sell short-term and buy longer-term puts to profit from a large downward move over time.

The premium on American put options depends on several factors. Intrinsic value is the difference between the strike and asset price; higher intrinsic value means a higher premium. Time remaining until expiry also impacts premiums, with more time meaning higher values. Implied volatility boosts premiums due to the increased probability of finishing in the money. Rising interest rates also increase premiums because of the reduced forward prices of the underlying Asset.

How to buy and sell Options?

The process of buying and selling options starts with selecting an online broker. Let us look at how to buy options.

Select an online broker that offers options trading. Look for low commissions and an intuitive trading platform. Many reputable brokers provide resources for learning about options, too.

Open a brokerage account if you don’t already have one. Make sure it is approved for options trading, which requires filling out an options agreement form.

Deposit funds into your brokerage account to cover the premium payments required for option purchases. Maintain sufficient buying power.

Use option chain tools to search for option contracts on the desired underlying Asset. Filter by expiration month, strike price, call/put type, bid/ask price, etc.

Choose the specific option contracts to buy. Consider the strike price, expiration date, and premium cost that aligns with your outlook and risk tolerance.

Determine the optimal order type (- market order, limit order, stop order, etc). Market orders are executed immediately at the asking price. Limit orders set a maximum premium you’re willing to pay.

Place the option buy order through your brokerage platform. Specify the option ticker, order type, number of contracts, and any special instructions.

Review the order confirmation and monitor the status. An immediate fill confirms execution. A working order waits for the limit price threshold to be reached.

Check your account positions to ensure the options contracts were purchased correctly. The options will be listed with their unique contract specifications.

Closely track the market price of the underlying Asset going forward. Evaluate whether to sell your option contracts or exercise in-the-money options at expiration.

Now let us look at How to Sell Options Contracts.

Make sure your brokerage account is approved for uncovered options writing. This requires a higher options trading level and capital balance.

Search the option chain to find contracts to potentially sell. Look for optimal strike prices and expirations that match your outlook.

Evaluate the proposed premium income from selling the option versus the maximum risk of being assigned. Determine suitable contracts.

Place the option sell order just like a regular stock order, indicating the option ticker, order type, quantity, and price.

Once the order fills, monitor your account positions frequently to see your open short options exposure and associated collateral requirements.

Watch the price direction of the underlying Asset closely. Prepare to buy back short options at a profit if the market moves favorably.

Be prepared for potential assignment per the terms of the contract if holding short options through expiration. You may need to sell or buy shares of the stock.

Actively manage short-option positions using buy-to-close orders, rolling tactics, spreads, and other techniques to generate income and avoid big losses.

Use stop-orders to close out short option positions at a reasonable loss amount if the underlying price moves adversely. Define and limit risk.

Develop a trading plan detailing when you will buy-to-close or roll short options positions depending on profit targets, loss limits, time decay, and upcoming events.

Regularly review your short options exposure in the context of your overall portfolio and risk parameters. Reduce positions if over-concentrated.

The above steps are the standard way to purchase or sell an option. Follow the same to ensure maximum results.

What trading strategies are best for Put Options?

The most common and effective strategies for trading put options include buying long puts, protective puts to hedge risks, bear put spreads, married puts, collars around a stock position, put back spreads, put ratio spreads, calendar/diagonal spreads, straddle/strangle combinations, synthetic short stock, and various multi-leg put credit or debit spreads. Below are more details about them.

One of the most basic put option strategies is simply buying long puts to speculate on a downward move in the underlying Asset or hedge an existing long position. Long puts provide powerful leveraged returns if the asset price drops below the strike price. The risk is limited to the known premium paid. Traders buy puts if they expect declining prices.

Buying long puts to protect an existing long stock position is known as a protective put strategy. The long puts lock in the ability to sell shares at the strike price, limiting potential losses if the stock price drops. Protective puts also allow continued upside participation if the stock rises. This hedging strategy defines the maximum downside risk.

A bear put spread entails selling a put option at a higher strike price while simultaneously buying a put at a lower strike. This defines and caps risk while allowing modest profits if the underlying asset declines. Traders use bear put spreads when expecting a mild-to-moderate downward move.

Married puts involve owning puts and being long the underlying stock at the same time. This allows continued upside exposure to the stock, while the long puts provide downside protection in case the share price falls. The put premium paid reduces the breakeven point of the stock.

A collar pairs long puts and short calls around the current market price of the underlying Asset. Typically, at-the-money puts are purchased to hedge the downside, while out-of-the-money calls are sold to offset the put premium cost. Collars are used to lock in gains after a rise in the stock.

Put Backspreads strategy sells short-term put options at one strike and buys longer-term puts at a lower strike. Put-back spreads aim to profit from a large downward move in the underlying Asset over time. Traders implement this when expecting a big decline beyond a recent support level.

A put ratio spread involves selling multiple put option contracts against each long put purchased at a different strike price. This creates a net credit received. Put ratio spreads to profit from sideways or upward moves in the underlying. They benefit from time decay on the short puts.

A put calendar spread sells near-term put options and buys longer-term puts at the same strike. This takes advantage of time decay on the short-term puts for profit. Traders use this strategy when expecting the underlying Asset to have a brief dip and then recover.

Buying a long straddle or strangle combines long puts and calls to profit from a significant move up or down. Straddles use the same strike price, while strangles use different strikes. Traders use this strategy when anticipating volatility expansion ahead of a major event.

A synthetic short stock position combines buying at-the-money puts and selling at-the-money calls with equal delta values. This mimics being short the stock but with defined risk from the options. Traders implement this when seeking limited-risk bearish exposure.

There are many types of put spread strategies – bear call spreads, back spreads, ratios, diagonals, etc. These combine multiple bought and sold puts to form a spread trade with capped downside risk. Spreads allow complex options trading with lower capital requirements.

Traders will be able to utilize puts across diverse market environments by mastering these strategies.

Why would you buy a Put Option?

An investor would buy a put option if they expected the price of the underlying security to decline. Buying puts allows investors to profit from falling prices without having to short-sell the Asset directly. Puts provide leveraged return potential if the security drops sharply compared to the option premium paid. Speculators buy puts to capitalize on anticipated downward moves.

Investors also buy puts to hedge downside risk in existing holdings. For example, an investor who owns 100 shares of XYZ stock trading at Rs.50 could buy one XYZ 50 put option contract. This locks in the right to sell their shares at Rs.50, even if the stock drops below that price. This limits potential losses in the stock position to the known premium paid for option protection.

Some traders buy puts as part of certain spread strategies designed to generate income. For example, a put credit spread sells a put option and buys a lower strike put. This brings in more premium income than standalone writing but requires buying protection puts to limit risk. The long puts define maximum losses.

Puts allow taking a leveraged bearish position with a smaller capital outlay compared to shorting the stock. For example, considering XYZ stock is Rs.50, shorting 100 shares requires Rs.5000. But buying one Rs.50 put option contract only costs Rs.500. The put offers exposure to a 10% price drop with less upfront investment.

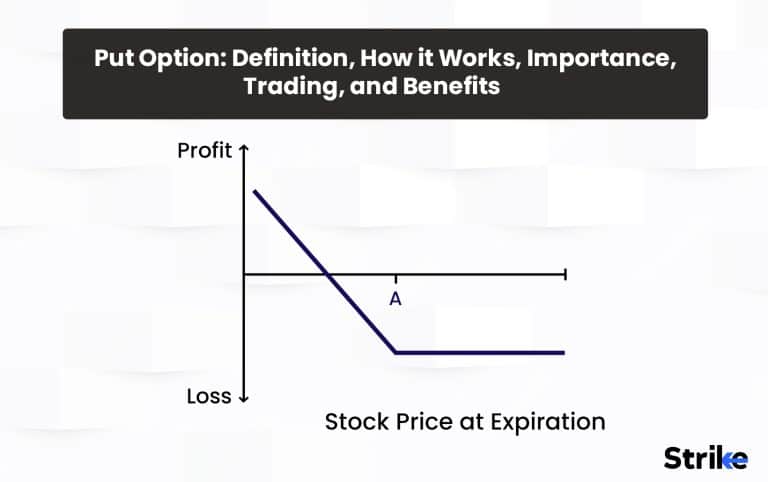

What is the payoff profile for the buyer of a Put Option?

The maximum potential loss for the put buyer is limited to the premium paid to purchase the option. The most the put buyer can lose is what they initially paid for the option contract, even if the underlying Asset becomes worthless,

The potential profit for the buyer is uncapped. It is determined by the strike price set in the option contract minus the market price of the underlying Asset when exercised.

For example, say an investor buys a put option with a strike price of Rs.50 for a premium of Rs.2 per share.

The put expires worthless, and the investor loses the Rs.2 premium paid if the price of the underlying is above Rs.50 at expiration.

The put buyer can exercise to sell the Asset at Rs.50 rather than the market price of Rs.40 if the price of the underlying is Rs.40 at expiration. This captures the Rs.10 per share of intrinsic value minus the Rs.2 premium cost for a net profit of Rs.8 per share.

The breakeven point for the put buyer is the strike price minus the premium paid. Below this level, profits begin.

So the put buyer’s payoff at expiration is,

Profit = Strike Price – Underlying Price – Premium

- Losses are capped at the premium paid

- Profits are uncapped below the breakeven point

The buyer benefits from declining prices in the underlying Asset. Their payoff is asymmetric, with small, limited losses if the put expires worthless and large potential gains if asset prices drop substantially below the strike price at expiration.

Why would you sell a Put Option?

Selling puts collects premium income upfront, which the investor keeps regardless of whether the option expires in the money or out of the money. The premium provides a cushion against potential losses if the stock price declines.

An investor who wants to buy a stock at a lower price can sell puts. The investor gets assigned and buys the stock at the strike price if the puts expire in the money. The investor pockets the premium if not. This allows the investor to potentially buy the stock at a discount.

Selling puts expresses a bullish view of the underlying stock. The seller is betting the stock which will stay above the strike price, allowing them to keep the full premium. They are obligated to buy the stock if it drops below the strike. Owning a stock and selling puts on that same stock is a way to hedge against potential declines in the stock price. The put premium can offset some losses if the stock price drops.

What is the payoff profile for the seller of a Put Option?

The maximum profit for the put seller is limited to the premium received for selling the put. The seller gets to keep this premium regardless of whether the option is exercised or expires worthless.

The maximum loss for the put seller is theoretically unlimited. This would occur if the stock price went to zero. The put seller would be obligated to buy the stock at the strike price, even if the shares are worthless.

The breakeven point for the put seller is the strike price minus the premium received. For example, Consider selling a 50 put for Rs.2 premium, your breakeven is Rs.48 (Rs.50 strike – Rs.2 premium). You will at least break even as long as the stock stays above Rs.48,

The stock drops below the strike price, which implies the put seller begins losing money. They are obligated to buy the stock at a higher strike price. The losses increase the further below the strike price of the stock drops. The premium, however, cushions the losses to some extent. For example, consider the stock drops to Rs.40, then the loss would be Rs.10 per share. But the Rs.2 premium reduces that loss to Rs.8.

Where to trade a Put Option?

The main way most individual investors trade stock put options is on public exchanges like the Chicago Board Options Exchange (CBOE) or the NYSE American Options Market. Here, option contracts on equities, ETFs, and stock indexes are listed with fixed strike prices, expirations, and uniform specifications. Trading exchange-listed puts provides transparency and liquidity.

Major stock broker platforms give access to exchange-traded equity, index, and ETF put options. Traders easily look up option chains, place trades online, and manage positions. Puts bought on an exchange are guaranteed for settlement by the Options Clearing Corporation (OCC).

Over-the-counter (OTC) options are traded directly between two parties rather than on an exchange. This allows customization in the strike price, expiration date, contract size, and terms. OTC offers flexibility for specialized options trading. Banks and institutions deal in OTC options markets.

For retail traders, brokers facilitate OTC put trades based on the client’s objectives. OTC puts typically have wider spreads and less liquidity than exchange-traded options. But they are tailored to align with specific views and risk profiles.

Put option contracts are also widely available on futures markets like the Chicago Mercantile Exchange (CME) and ICE Futures. These puts have futures contracts like commodities, currencies, interest rates, and indexes as their underlying assets. The futures options markets offer deep liquidity in derivatives trading.

There are a growing number of cryptocurrency options platforms that provide puts enabling speculative trading or hedging of crypto assets like Bitcoin, Ethereum, etc. These platforms often share similarities with the Stock Market in terms of trading dynamics and risk management. Unlike the traditional Stock Market, these are typically OTC markets operated by digital currency exchanges and brokers.

When to trade a Put Option?

Let us look at four possible scenarios when you would want to trade a put option.

You think the price of the underlying Asset will go down. Buying a put option gives you the right to sell the Asset at a specified price, allowing you to profit if the price goes down. This is one of the main reasons to buy a put; you are betting on the price declining.

You want to hedge against potential losses on an asset you already own. Buying puts allows you to limit your downside if you own a stock and are worried the price may drop. The put limits your losses if the stock price falls below the strike price.

You want to use puts to generate income. Selling (writing) put options collects premium income upfront. The tradeoff is that you are obligated to buy the Asset at the strike price if assigned. Selling puts can generate income if you are willing to buy the Asset at a discounted price.

You are using puts as part of an options strategy like a spread or a straddle. Complex option trades utilize various put and call option combinations to create strategies with defined risk or reward.

How much is the price of a Put Option?

The price of a put option is known as the premium. Let us look at a few factors on which the premium price depends.

Strike price: The strike price is the price at which you can sell the underlying Asset if you exercise the put option. A lower strike price tends to have a higher premium.

Time to expiration: Puts with a longer time until expiration has higher premiums than those expiring soon. More time means a higher chance that the stock will fall below the strike price.

Volatility: Higher implied volatility of the underlying stock results in higher put premiums. There is more uncertainty priced into the option.

The price of the underlying: Puts tend to increase in value as the price of the underlying stock declines relative to the strike price. The intrinsic value component of the option becomes greater.

Interest rates: Rising interest rates tend to slightly increase premiums.

Dividends: Puts on stocks with higher dividends tend to have lower premiums. Dividends reduce expectations of downward moves in the stock price.

Out-of-the-money put options, as a rough estimate, trade for 5-10% of the underlying stock price. And at-the-money put costs about 10-20% of the stock price. Deep in the money puts trade closer to the intrinsic value.

What are the factors that determine the price of Put Option?

The key factors that determine the price of the Put option are strike price, volatility, time remaining, price of the underlying Asset, interest rates, dividends, days to expiration, and supply/demand dynamics.

1. Strike Price

– The strike price is the price at which the put option allows you to sell the underlying Asset.

– Puts with lower strike prices have higher premiums; else is equal. This is because there is a greater likelihood the asset price will fall below a lower strike at expiration.

2. Time to Expiration

– Longer time until expiration equates to higher put premiums. More time allows a greater chance that the stock moves below the strike.

– Time value erosion accelerates as expiration approaches and the put premium declines.

3. Volatility

– Implied volatility is a measure of the expected price fluctuation of the underlying Asset.

– Higher implied volatility leads to higher put premiums. The pit has more value due to the greater downside risk.

– Low implied volatility reduces put values since large price declines are viewed as less probable.

4. Price of the Underlying

– The price of the underlying stock relative to the strike price impacts the put value.

– The put becomes more valuable due to its higher intrinsic value when the stock price declines further below the strike.

– The put solely has a time value and no intrinsic value when the stock price is above the strike.

5. Interest Rates

– Rising interest rates tend to increase option premiums slightly.

– This is because higher interest rates reduce the present value of the strike price paid in the future at expiration or exercise.

6. Dividends

– Puts on stocks with higher dividend payouts will tend to have lower premiums.

– Dividends reduce the expectations of sharp downward moves in the stock price.

7. Days to Expiration

– Puts with more days until expiration have a higher time value and premiums.

– Time value decays rapidly in the last 30-60 days, meaning premiums decline as expiration nears.

8. Supply and Demand

– The laws of supply and demand impact option prices. Increased demand for puts raises premiums.

– Lack of open interest and volume in a put can lower its liquidity and premium.

Options pricing models quantify how these variables interact to determine the fair market value of a put option.

When does the Put Option expire?

A put option expires on the third Friday of the expiration month stated in the options contract. This is usually the month following the trade date of the option.

How is the Put Option value calculated?

Below is a step-by-step guide on how to calculate the value of a put option.

First, Determine the Intrinsic Value

The intrinsic value is the difference between the strike price and the underlying Asset’s price, if positive.

– Compare the strike price to the asset price.

– Intrinsic value = Strike price – Asset price, if the asset price is below the strike price.

– Intrinsic value = 0 if the asset price is above the strike price.

Second, Estimate the Time Value

The time value represents the chance of the Asset falling below the strike. It depends on time to expiry and volatility.

– Time value is higher for longer expiries since there is more time for the Asset to fall.

– Time value increases with higher volatility as there is more uncertainty in price.

– Use an option pricing model to quantify time value based on the above.

Third Account for Interest Rates

Higher interest rates increase the value slightly.

– Higher rates reduce the present value of the strike price paid at expiry.

– Using a pricing model, estimate the impact of interest rates on time value.

Fourth, Consider Dividend Impact

Puts on high-dividend stocks have lower values.

– Dividends reduce expectations of downward price moves.

– Use a pricing model to adjust for dividends.

Fifth Factor in Early Exercise Possibility

Deep- In the money, puts are exercised before expiry.

– Modify the remaining time value if early exercise is optimal.

Sixth, Apply Supply and Demand

Imbalances between buyers and sellers can impact premiums.

– More buyers than sellers lift premiums above fair value.

– Insufficient demand can lower premiums.

How can investors profit from a falling asset price with Put Options?

One method is simply buying put options on the Asset if they believe prices will fall below the strike price. The put options gain intrinsic value as the underlying price declines, which is realized as a profit when sold. Buying puts limits the maximum loss to just the premium paid if prices move against the investor’s downside view.

Another approach combines short-selling the Asset with buying put options as a hedge. The short position gains profit if prices fall as expected, which helps offset the cost of buying the protective put options. The put options limit the potential loss on the short side if the asset price instead rallies unexpectedly. Investors also use put credit spreads, selling a higher strike put and buying a lower strike put. The short put position gains value as prices fall, while the long put protects against unlimited losses.

Investors also pair put option purchases with call option writing to create collar positions. The call premiums help pay for the protective puts. Collars limit the profit potential on the upside but offer downside protection without needing to outlay large amounts of capital. Finally, buying puts while owning the Asset itself is called a married put position. This puts a hedge against falling prices while allowing investors to retain upside if prices rise. In summary, puts enable several strategies to target profits from declining asset prices.

How much can an investor make on a Put Option?

There is no limit to how much an investor will be able to make on a put option, but the maximum profit is capped. The maximum possible profit on a long put option is the strike price minus the premium paid if the underlying stock goes to zero. For example, a Rs.50 strike put purchased for Rs.2 has a maximum profit of Rs.50 – Rs.2 = Rs.48 per share if the stock expires worthless. Profits are capped in practice because stocks rarely go to zero.

Profits are made if the stock falls below the strike price by more than the premium paid. A Rs.2 put on a Rs.10 stock now at Rs.5 is worth Rs.5 intrinsic value plus time value for a gain of around Rs.3. In percentage terms, profits are very large due to put option leverage. For example, a 50% drop in a stock price could result in a 100-200% return on the put option. However, percentages depend on the amount of premium paid.

How much can an investor lose on a Put Option?

The investor’s maximum potential loss is defined and limited to the amount of premium paid for the options. The premium is lost if the options expire out of the money because the stock price remains above the strike price; the options are worthless. However, losses are unlimited when selling or writing naked put options. The investor is obligated to purchase the stock at the strike price if assigned on short puts, which could be far above the current market value. This could lead to significant losses if the stock has fallen sharply.

Investors sell cash-secured puts to limit losses when writing puts, which involves setting aside cash to potentially buy the assigned stock. Any loss would be capped by the cash held to buy the shares. Another method is selling puts against an existing short stock position, which simply closes out the short at the strike price if assigned. Using put debit or credit spreads also caps the maximum loss to the defined net debit or credit taken when opening the spread position. Finally, early assignment of puts before dividend dates sometimes leads to unexpected losses for option sellers.

How does the Put Option differ from a Call Option?

Let us look at five key points where a call option and a put option differ.

Purpose

The main difference is that call options give the holder the right to buy the underlying Asset at the strike price, whereas put options give the holder the right to sell the Asset at the strike price. Calls benefit from rising prices, while puts benefit from falling prices.

Payoff

The payoff profile is the opposite of calls and puts. The profit is unlimited with calls as the underlying price rises above the strike price. With puts, the profit is capped if the price goes to zero, but losses are limited to the premium paid.

For calls, any price above the strike results in a profit if exercised. For puts, prices below the strike are profitable if exercised.

Risk Profile

Buying calls risks the premium paid, while buying puts risks just the premium amount. However, short calls have unlimited loss potential as prices rise, whereas short puts have uncapped losses as prices fall below the strike.

Time Decay Impact

Time decay, or theta, has slightly different impacts on puts and calls. Time decay accelerates on puts as expiration nears since any in-the-money amount starts eroding. Calls tend to decay slower out-of-the-money but accelerate in-the-money.

Strike Price Selection

Puts often target out-of-the-money strike prices since the goal is for the stock to fall below the strike. Calls tend to use at-the-money or slightly out-of-the-money strikes since the goal is for the stock to rise.

Calls, or call options, benefit from rising prices, while puts benefit from falling prices. Their differing risk profiles, with call options favoring bullish markets and puts favoring bearish ones, and time decay behavior lead to divergent trading strategies as well.

What are the benefits of the Put Option?

Puts serve strategic roles ranging from protection to income generation to acquisition to portfolio management and risk control across a variety of contexts. Here are the 11 key advantages and benefits of using put options.

Downside Protection

Put options allow investors to limit the maximum loss on a long stock position to the premium paid for the puts. They provide downside protection without having to realize losses by selling the stock. Puts give the right to sell at the strike price, providing a hedge against falling prices.

Speculating on Declines

Puts provide leveraged performance if the trader’s bearish view on the stock is correct, with large percentage returns possible from sharp declines. Put options have defined, fixed risks, unlike short selling. Puts allow speculating on falling prices with capped losses.

Generating Income

Put options generate income through cash-secured put writing or naked put writing. The seller collects premiums upfront and may be assigned to buy the stock at the strike price. Income accrues as long as the stock remains range-bound.

Acquiring Stock

Investors wanting to buy a stock at a lower price sell puts below the market price to get paid to wait. If options expire worthless, the premium is kept. If assigned, shares are acquired at the strike price for an effective discounted purchase price.

Hedging Systemic Risks

Protective puts on indexes, sectors, or negatively correlated stocks hedge systemic risks like market crashes without selling assets. The cost is limited to put premiums. Puts allow riding out portfolio drawdowns.

Managing Concentrated Positions

Investors with concentrated stock positions buy puts to protect against the downside without diversifying and realizing taxable gains. Puts provide risk management without disrupting the core position.

Implementing Target Prices

Put backspreads allow establishing a target sale price on a stock by simultaneously buying closer-to-the-money puts and selling lower strike puts. Puts get exercised at the target exit price.

Exiting Stock Positions

Selling covered calls against a long stock position generates income. Buying protective puts creates a collar strategy that exits the position if the stock falls below the put strike price.

Creating Synthetic Positions

Combining puts and calls creates synthetic positions, replicating other instruments. Synthetic long stocks, shorts, and forward contracts are constructed without trading the actual assets.

Accessing Diversification

Purchasing puts on stocks, indexes, or ETFs provides access to diversification for portfolios that otherwise have restrictions or limitations on asset classes. Puts allow managing risk exposures.

Hedging Events or Opportunities

Put options allow for insulating portfolios from known events like elections, FOMC meetings, earnings releases, clinical trials, regulatory rulings, and product launches. Puts help manage transient risks.

The defined, capped downside risks make a leveraged instrument suitable for offensive and defensive financial strategies.

What are the risks of the Put Option?

Puts themselves have defined, capped risk. S, short put exposure poses uncapped losses. Time decay, volatility shifts, interest rate moves, and indirect leverage also contribute to the risks around puts. Here are 7 key risks to consider when trading or investing with put options.

Limited Time Horizon

Put options have an expiration date, after which they become worthless if unexercised. This pressures traders to be accurate on the timing, magnitude, and direction of anticipated price moves. The put option expires worthless if the expected decline does not occur prior to expiration despite being directionally correct.

Loss of Premium

Buyers of puts face losing the entire premium paid if the asset price remains above the strike price at expiration. The loss occurs if the drop is not sufficient enough for the puts to gain intrinsic value, even if the market declines. The maximum loss is limited to the premium paid.

Uncapped Losses

Unlike long puts, short put options have an uncapped downside if the trader is assigned and forced to purchase the underlying Asset above fair value. This poses unlimited loss if the price continues to fall below the strike price at which the stock is assigned.

Early Exercise

American-style puts are exercised by counterparties anytime prior to expiration. Early exercise could force traders out of positions before anticipating, depriving them of remaining time value.

Volatility Changes

Falling implied volatility negatively impacts put values, all else equal. Declining volatility reduces profits on long puts or increases losses on written puts as time value erodes.

Interest Rate Changes

Rising interest rates have a mildly negative impact on put values. The discounted present value of the strike price paid at expiry increases with higher interest rates. This factor dampens long-put profits somewhat.

Indirect Risks

Puts on leveraged ETFs or futures may experience losses exceeding the cap on losses of the underlying Asset due to the indirect nature of the option exposure. Indirect puts have embedded leverage risks.

Managing these directional, time decay, and external risks is key to successful put trading.

Are Put Options profitable?

Yes, Put options could certainly be profitable trading and investing instruments when used prudently, but they do come with risks like any leveraged derivative instrument.

Is buying a Put Option the same as Short Selling?

No, buying puts and short selling the underlying stock is not the same. Short selling has unlimited loss potential if the stock rises, whereas the loss on a long put is capped at the premium paid.

However, both put-buying and shorting benefit from a decline in the underlying stock price. Puts provide exposure to downside movement with defined and limited risks.

Can you buy a Put Option without owning the stock?

Yes, an investor does not need to own the underlying stock in order to purchase put option contracts on that stock.

One of the advantages of options is that they provide exposure and the ability to benefit from price moves without owning the Asset itself.

So, put options can certainly be traded speculatively without actually shorting or owning the stock itself.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 4")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 5")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 6")

: Overview, 10 Types of Indicators, Settings for Different Markets 7")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 10")

No Comments Yet.