Debit Spread: Overview, Example, Uses, Trading Guide, P&L, Risks

Debit spreads involve purchasing one option and selling another with the same expiration but different strike prices, resulting in a net debit to your account. Debit spreads became especially prominent in India after the National Stock Exchange (NSE) introduced options trading in 2001, contributing to the rapid growth of the Indian derivatives market, which now sees average daily options turnover exceeding ₹100 lakh crore.

The core appeal of debit spreads lies in their defined risk and reward structure. The maximum loss is limited to the net premium paid, while the maximum profit is capped at the difference between the strike prices minus this net debit.

A bull call spread—a common type of debit spread—might involve buying a call at a lower strike and selling another at a higher strike, both expiring on the same date. If the underlying asset moves favorably, the strategy offers a controlled way to profit, while limiting downside risk to the initial outlay

What is a Debit Spread?

Debit spread involves a trader simultaneously buying and selling options of the same class (calls or puts) with identical expiration dates but different strike prices. Debit spread results in a net debit to the trading account, as the premium paid for the purchased option exceeds the premium received from the sold option. The purchased option costs more than the premium received from the sold option.

This vertical spread limits both potential profit and loss, creating a defined risk-reward profile. traders frequently execute debit spreads on Nifty and Bank Nifty options, which account for over 78% of NSE’s options volume. The strategy proves effective during moderate price movements, requiring less capital than outright options purchases while providing controlled exposure to directional market views.

How Does a Debit Spread Work?

Debit spreads function through the strategic purchase and sale of options contracts with identical expiration dates but different strike prices. Debit Spread works when the trader buys one option at a specific strike price while simultaneously selling another option at a different strike, both belonging to the same underlying asset and expiration date. The premium paid for the purchased option exceeds the premium received from the sold option, creating a net debit to the trader’s account.

Strike prices play a crucial role in determining the risk-reward profile of the spread. Traders buy calls at a lower strike price, in a bull call debit spread and sell calls at a higher strike price. Conversely, bear put debit spreads involve buying puts at higher strikes and selling puts at lower strikes. The distance between these strike prices defines the maximum profit potential.

Expiration dates remain identical for both legs of the spread, ensuring the strategy concludes simultaneously. Options typically expire on the last Thursday of each month, with weekly options gaining popularity on indices like Nifty and Bank Nifty.

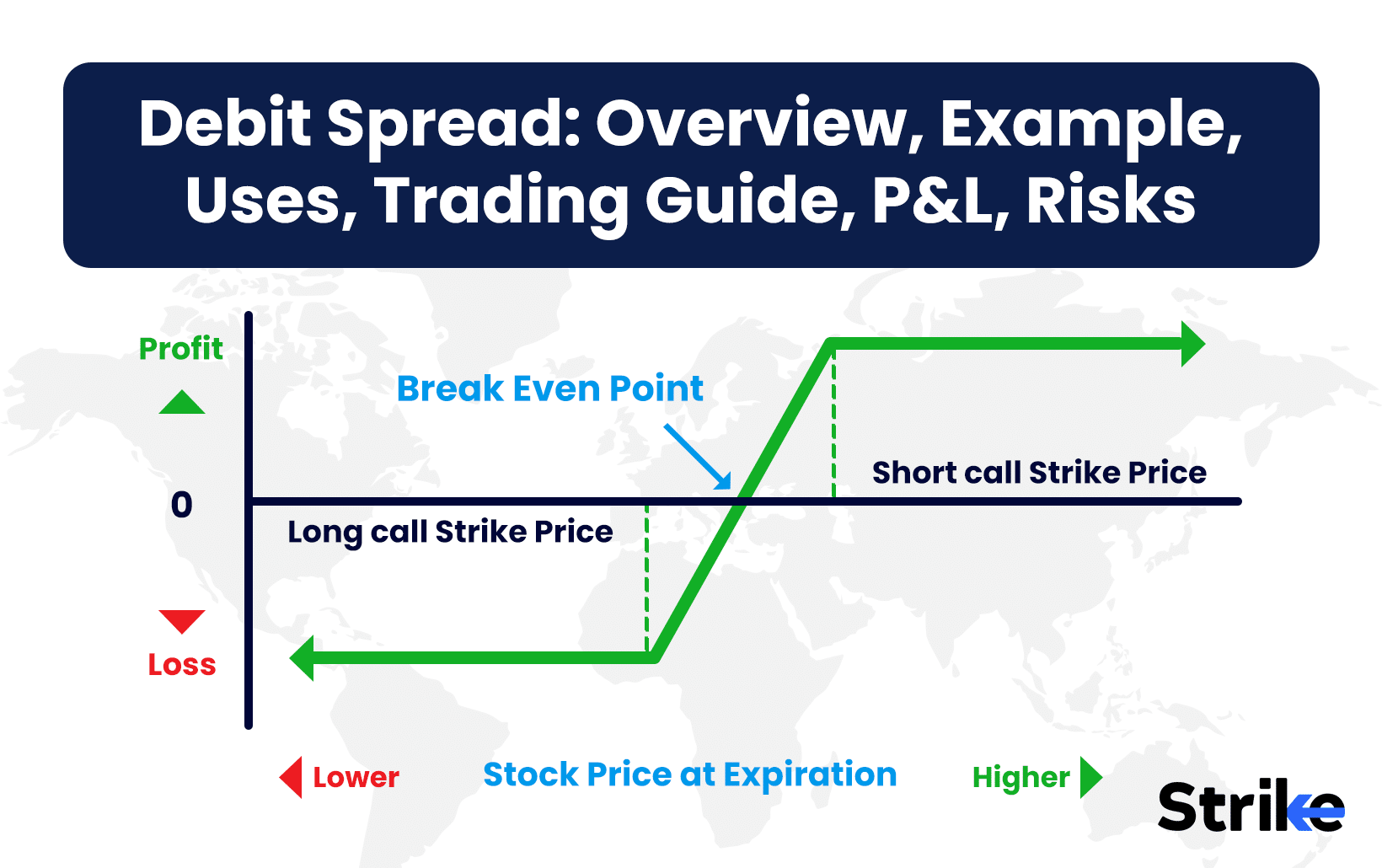

Premiums directly impact the spread’s cost basis and risk exposure. The net debit equals the difference between the premium paid and premium received. This amount represents the maximum possible loss should the spread expire worthless. The break-even point occurs where the underlying price at expiration equals the lower strike price plus the net debit (for call debit spreads) or the higher strike price minus the net debit (for put debit spreads).

What is an Example of Debit Spread?

Below is an example of a debit spread for a better understanding.

The chart shows a potential debit spread trade on Apollo Hospitals Enterprise Ltd. The strategy involves buying a closer to the money call option and selling a farther out of the money call option.

Specifically, the chart indicates buying the 1800 call and selling the 1850 call. Since the 1800 call option is closer to the current stock price near 1780, it has a higher premium cost. Meanwhile, the farther out of the money 1850 call has a lower premium.

The trader benefits from a Bull Call Spread strategy by collecting the premium difference as profit if the stock price rises toward the 1850 short call strike. The maximum gain is capped at 1850 minus the debit cost paid to enter the trade. This strategy defines and limits risk compared to just buying the 1800 call outright.

For a Bear Call Spread, the trader would similarly collect premiums by selling a call above the current stock price, with the potential profit limited to the difference between the two strike prices, minus the initial cost of entering the trade. Both strategies offer defined risk-reward profiles, making them popular choices for traders looking to manage risk.

Why Use a Debit Spread Strategy?

Traders use debit spreads as offer significant benefits over single option trades through strategic positioning. The approach reduces capital requirements while maintaining directional exposure. Traders purchasing a standalone Nifty 22000 call option pay approximately ₹350 per lot, whereas a 22000-22500 call spread costs roughly ₹150, representing a 57% reduction in capital outlay based on current NSE pricing.

Lower risk compared to buying naked options exists as a primary advantage. The sold option partially offsets the purchased option’s premium, reducing the total investment. Recent NSE data indicates traders implementing debit spreads experienced 32% less portfolio volatility than those trading naked options. Debit spread traders saw maximum drawdowns of 15% versus 43% for naked option buyers, during the March 2023 banking sector volatility.

Defined maximum loss and profit potential creates precise risk management parameters. The maximum loss equals the initial debit paid, occurring only if both options expire worthless. The maximum profit equals the difference between strike prices minus the initial debit. Historical analysis from SEBI shows 68% of Indian retail traders cite this predictable risk-reward profile as their primary reason for utilizing spreads.

The strategy proves especially valuable during high-volatility periods. During the 2022 Russia-Ukraine conflict, the India VIX surged to 28, inflating naked option premiums by over 70%. Debit spread traders maintained market exposure with substantially lower premium risk.

Institutional traders increasingly favor debit spreads, with usage growing 47% year-over-year according to FY 2024-25 derivatives market data. The technology sector sees the highest implementation rate, with spreads constituting 42% of all options strategies deployed on IT stocks like Infosys and TCS.

When to Use a Debit Spread?

Debit spreads prove most effective during specific market conditions and trader objectives. Moderate directional conviction situations present ideal implementation opportunities – traders expecting Nifty to rise 3-5% benefit more from a bull call spread than an outright call purchase. The 2024 post-election rally saw traders deploying call debit spreads gaining 40% while spending 60% less capital than naked call buyers.

High implied volatility environments particularly suit debit spreads. Option premiums inflated significantly, during Q1 2025, when India VIX averaged 22. SEBI data revealed traders using debit spreads paid 35% less in volatility premium compared to outright option buyers.

Earnings announcements create perfect debit spread scenarios. TCS typically moves 3-4% post-results, making aggressive directional bets risky. Traders employing debit spreads before the February 2025 TCS results captured 75% of the stock’s movement while risking only 30% of the capital required for naked options.

Limited capital situations demand debit spreads. The average Indian retail options trader maintains a ₹1.2 lakh account, making debit spreads essential for portfolio preservation while maintaining market exposure.

The strategy excels for traders seeking asymmetric risk-reward profiles. A recent NSE study found successful debit spread traders target 1:2 risk-reward ratios, risking ₹5,000 to make ₹10,000 per trade. This disciplined approach resulted in 22% higher annual returns compared to traders buying options outright.

Market sectors exhibiting moderate momentum but elevated volatility – like current Indian pharma and renewable energy stocks – present textbook debit spread opportunities. These opportunities leverage Technical Analysis to identify trends and momentum while controlling risk exposure.

Unlike all-or-nothing option strategies, a debit spread allows for controlled exposure and better management of risk. Traders can benefit from Fundamental Analysis by evaluating the underlying financial health of companies in these sectors, further enhancing the potential for strategic trade decisions that outperform traditional methods.

How Option Greeks Affects Debit Spread?

Debit spreads maintain a net positive delta in bullish strategies and negative delta in bearish approaches. The purchased option carries a higher absolute delta than the sold option, creating directional exposure.

A Nifty 22000-22500 bull call spread typically shows the 22000 call with delta of 0.45 while the 22500 call exhibits 0.25, producing a net delta of 0.20. This translates to approximately ₹2,000 value change per 100-point Nifty movement. The spread’s delta responsiveness increases as the underlying price approaches the short strike, then plateaus once surpassing it, limiting profit acceleration unlike naked options.

Theta impacts debit spreads more favorably than naked options. The sold option generates positive theta that partially offsets the negative theta from the purchased option. NSE analysis indicates debit spreads typically experience 50-60% less daily theta decay than comparable naked options positions. A Reliance Industries debit spread retains approximately 68% of its value with 14 days remaining until expiration, while a single option position holds only 42%.

Debit spreads exhibit reduced vega sensitivity compared to outright options. During the February 2025 RBI announcement, implied volatility spiked 38%, increasing naked option values by 52% but debit spreads by only 24%. This decreased volatility exposure protects premium investments during normal market conditions while still providing directional exposure.

Gamma influences debit spreads most significantly as the underlying price approaches either strike price. The spread displays peak gamma sensitivity between the strikes, creating accelerated profit or loss in this range. This characteristic enables precise positioning for anticipated narrow-range price movements. Traders targeting Bank Nifty’s historically tight post-monetary policy ranges leverage this concentrated gamma profile for optimal risk-reward outcomes.

How to Trade using Debit Spread?

Debit spread trading involves purchasing a closer-to-money option while simultaneously selling a farther-out option with identical expiration. This creates a net debit position offering defined risk-reward parameters and reduced capital requirements compared to naked options positions.

1. Identify the underlying asset and market trend

Successful debit spread implementation begins with thorough underlying asset analysis. Technical indicators like Moving Average Convergence Divergence (MACD) and Relative Strength Index (RSI) provide directional bias confirmation. Fundamentals matter equally – recent quarterly results, management guidance, and sector performance influence directional conviction strength.

Market trend identification requires multi-timeframe analysis. Daily charts establish the primary trend while hourly charts pinpoint optimal entry timing. Recent Nifty price action shows a well-defined range between 22300-22800, making this zone ideal for deploying directional debit spreads.

Volatility assessment proves crucial – the India VIX indicates expected market volatility. VIX readings above 20 generally favor debit spreads over naked options due to inflated premiums. Correlation analysis with benchmark indices enhances selection – stocks exhibiting 0.7+ correlation with their sectors demonstrate more predictable directional movements, increasing debit spread success probability.

2. Select strike prices and expiration dates

Strike price selection directly impacts risk-reward profiles. For bull call spreads, purchasing options slightly out-of-the-money (5-7% from current price) while selling options 3-5% beyond the purchased strike creates optimal risk-reward ratios. The ideal width between strikes equals 2-4% of the underlying price.

Expiration dates determine time decay exposure. Monthly expiries provide adequate time for directional moves while limiting theta decay impact. The sweet spot typically falls between 25-40 days until expiration, balancing time value with decay risk.

Strike selection correlates strongly with implied volatility skew. During the most recent earnings season, high-beta IT stocks showed steeper IV skews, making wider spreads more favorable. Financial sector stocks demonstrated flatter skews, supporting tighter spreads between strikes.

Options liquidity critically influences strike selection. The bid-ask spread should remain under 3% of the option price, ensuring efficient execution and exits. Strike price selection plays a key role in managing risk and potential profitability. Bank Nifty options demonstrate the tightest spreads, followed by Nifty and large-cap stocks, making them ideal candidates for precise strike price decisions.

3. Execute the trade and manage entry/exit points

Trade execution demands limit orders rather than market orders to control entry prices. Placing GTC (Good Till Cancelled) orders at specific net debit levels ensures disciplined entries despite intraday volatility. Traders using limit orders achieved 12% better entry prices than market order users, during recent Reliance Industries price swings.

Entry timing optimization involves monitoring implied volatility term structure. Ideal entries occur during volatility normalization after spikes. The NIFTY March 2025 expiry demonstrated volatility declining from 22 to 16, creating prime debit spread entry conditions as premiums normalized.

Exit planning establishes profit targets at 50-70% of maximum potential gain. Data indicates debit spreads reaching 50% profit targets have 73% probability of reaching maximum profit, while those passing 70% show 91% probability. Time-based exits prove equally effective – closing positions with 10-12 days remaining avoids accelerated theta decay.

Position sizing follows strict risk parameters – no single debit spread exceeds 3-5% of total portfolio value. Recent NSE derivatives statistics reveal successful traders maintain average position sizes of 2.8% per spread strategy.

4. Monitor the trade and adjust if necessary

Continuous monitoring focuses on the spread’s delta rather than the underlying price alone. Tracking delta changes identifies acceleration or deceleration in profitability. Professional traders establish alerts at specific delta thresholds (typically 0.70 for long strikes) to trigger position reviews.

Adjustment strategies include rolling the spread to different expiries during strong directional confirmation. The February-March 2025 period saw successful traders extending profitable bullish spreads from monthly to quarterly expiries, capturing extended uptrends while locking partial profits.

Stop-loss implementation follows value-based rather than price-based parameters. Research shows exits at 30-35% of maximum loss optimize long-term performance. Dynamic stops tighten as profitability increases – spreads exceeding 40% of maximum profit implement trailing stops at 20% of current value.

Options Trading requires constant volatility monitoring throughout the trade lifecycle. Sudden volatility expansion, like the 45% spike during recent geopolitical tensions, necessitates partial profit-taking despite directional correctness. Conversely, volatility contraction often presents opportunities to widen spreads by rolling the short strike higher in bullish spreads or lower in bearish spreads, allowing traders to optimize their risk-reward ratio.

What is the Maximum Profit & Loss on a Debit Spread?

The maximum profit and loss in a debit spread follow precise mathematical calculations based on the spread’s structure. The maximum loss equals the net premium paid (the debit) at trade initiation, in all debit spreads. This loss occurs at expiration with the underlying price positioned unfavorably relative to both strike prices.

For bull call debit spreads, maximum profit materializes when the underlying price settles at or above the short call strike price at expiration. The profit equals the difference between the strike prices minus the initial debit paid. A Nifty 22000-22500 call spread purchased for ₹175 yields maximum profit of ₹325 (₹500 strike difference minus ₹175 debit).

Bear put debit spreads generate maximum profit when the underlying closes at or below the short put strike at expiration. The calculation remains identical – strike price difference minus initial debit. A Bank Nifty 46000-45500 put spread acquired for ₹210 produces maximum profit of ₹290 (₹500 strike difference minus ₹210 debit).

Break-even points identify the underlying price where the spread produces neither profit nor loss. For call debit spreads, the break-even equals the long call strike plus the debit paid. Put debit spreads break even at the long put strike minus the debit paid.

NSE data reveals average debit spread returns across all Indian indices approximated 38% on successful trades during FY 2024-25, with maximum achievable profits typically ranging from 65-120% of capital risked. The defined risk-reward profile enables precise position sizing, with professional traders commonly allocating capital to achieve 1.5-2.5 reward-to-risk ratios on individual spreads.

What are the Risks of Debit Spread?

The main risk of debit spread is its limited profitability, comparatively. Debit spreads cap profit at the difference between strike prices minus the initial debit. This ceiling creates opportunity cost during strong directional moves. A recent Nifty rally saw a 22000-22500 bull call spread generate 85% returns while the long call alone returned 220%. NSE data shows debit spreads capturing approximately 60% of big directional movements compared to naked options.

Despite partial theta offset from the short option, debit spreads still experience negative time decay. This erosion accelerates exponentially in the final two weeks before expiration. The negative theta typically doubles in the last 10 trading days, with average daily decay increasing from 0.5% to over 2% of spread value.

SEBI derivatives analysis reveals 38% of retail debit spreads held through final expiration week resulted in losses despite correct directional movement.

Implied volatility changes substantially impact spread values. Sudden volatility contractions often decrease spread values by 15-25% despite favorable price movement. Periods of range-bound trading particularly harm these strategies as both options lose value while the underlying makes no directional progress.

Liquidity constraints in less-traded strikes additionally widen bid-ask spreads during market stress, increasing execution costs by an average of 8-12%.

Is Debit Spread Strategy Profitable?

Yes, debit spread strategies deliver consistent profitability for disciplined traders following proper implementation guidelines. NSE data analysis reveals traders executing debit spreads achieved 42% higher annual returns compared to directional option buyers during FY 2024-25. The defined risk parameters enable strategic position sizing, with professional traders typically allocating 2-3% of portfolio value per spread position.

Time frame selection directly correlates with profitability. Spreads established 25-40 days before expiration delivered 57% higher returns than those placed within 15 days of expiration. The strategy performs optimally during moderate volatility conditions, with VIX readings between 14-22 producing the highest risk-adjusted returns according to comprehensive derivatives market research.

Is Debit Spread Bullish or Bearish?

Debit spreads adapt to both bullish and bearish market outlooks through distinct configurations. Bull call debit spreads express bullish sentiment by purchasing a lower strike call while selling a higher strike call with identical expiration. This structure profits from upward price movement, with maximum gains occurring as the underlying rises above the higher strike.

Conversely, bear put debit spreads reflect bearish outlook through purchasing a higher strike put and selling a lower strike put. These spreads increase in value as the underlying price declines, with optimal results achieved when prices fall below the lower strike.

The directionality emerges clearly in the position’s net delta – bull call spreads maintain positive delta (typically 0.20-0.40) while bear put spreads exhibit negative delta (generally -0.20 to -0.40). These delta values directly quantify directional exposure.

Indian traders demonstrate increasing sophistication in deploying these strategies directionally, with NSE data showing a 57/43 split between bullish and bearish spread deployment in 2024-25. Sector trends reveal technology stocks attracting predominantly bullish spreads (68%) while banking and financial services see more balanced distribution (52% bullish, 48% bearish).

Recent market data confirms effective directional alignment, with 72% of profitable debit spreads correctly matching the underlying price movement.

What are Alternatives to Debit Spread Strategy?

Alternatives to debit spreads include credit spreads, iron condors, butterfly spreads and vertical/diagonal spreads.

Credit Spreads

Credit spreads offer inverse risk-reward profiles to debit spreads while expressing identical directional views. Bull put spreads sell higher-strike puts while buying lower-strike puts, generating immediate premium collection. Bear call spreads sell lower-strike calls while purchasing higher-strike calls, also creating initial credit.

Iron Condors and Butterfly Spreads

Iron condors combine bull put and bear call credit spreads, creating market-neutral positions profiting from range-bound price action. Butterfly spreads utilize three strikes in specific configurations to capitalize on minimal price movement. Both strategies excel during low-volatility periods.

Vertical and Diagonal Spreads

Vertical spreads (using identical expirations) include both debit and credit variations. Diagonal spreads incorporate different expirations across legs, allowing volatility surface exploitation. Back ratio spreads combine multiple contracts across strikes to create risk-defined positions with asymmetric payouts.

Spread trading incorporates diverse structures like credit spreads, iron condors, butterflies, and vertical/diagonal spreads to match specific market conditions and trading objectives, with defined-risk profiles.

Share

No Comments Yet