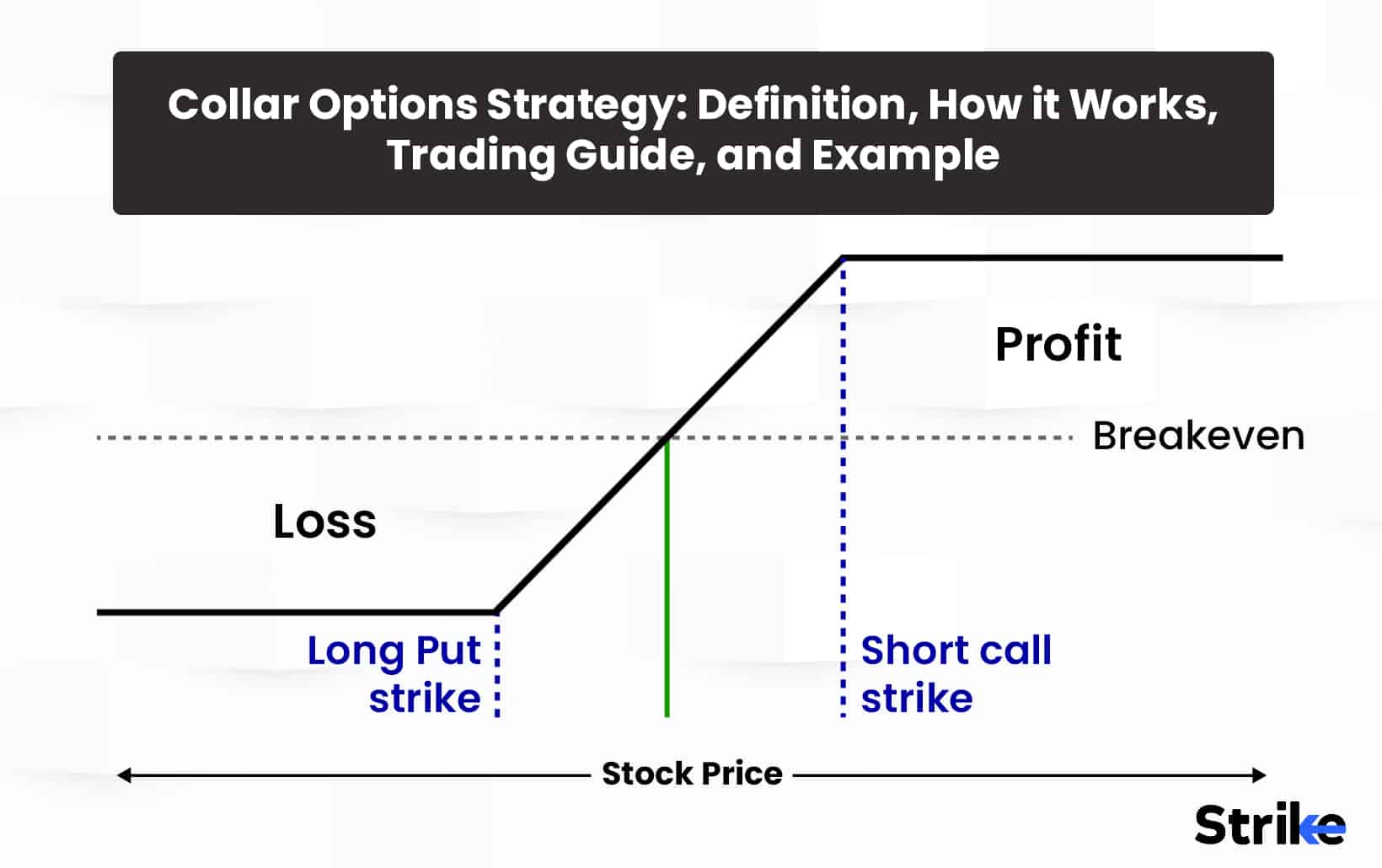

The collar options strategy is a common risk management approach that combines put and call options to create a range within which the underlying asset can trade. The collar limits profits in favour of downside protection around the investor’s target price. If the stock remains within the collar range, the options expire worthless, and the position is exited at no net cost.

But if the stock breaches either boundary, one of the options is triggered to initiate a profit or loss. The strategy aims to generate income from premium sales while setting a floor and cap on potential returns. This intro will explain how collar trades work, provide construction tips, and analyze an example.

What is the Collar Options Strategy?

The collar options strategy, also known as a protective collar, is a risk management strategy that uses options to limit both upside and downside risk on an underlying asset. It involves holding shares of the underlying asset, such as a stock, while simultaneously buying a put option and selling a call option on that same stock.

A collar strategy protects against losses while allowing for some upside until the short call strike price. It entails buying protective puts and selling covered calls against a long stock position. The main goal is to lock in some gains and protect against excessive losses.

The puts act like insurance and limit the downside. To offset the cost of the protective puts, the investor simultaneously sells out-of-the-money call options above the current market price.

The strike prices of the put and call are chosen so that the premium received from writing the call approximately offsets the premium paid for the put. This results in a net zero or low-cost collar.

The investor sometimes sells the stock at the put strike price if the stock price falls below the put strike at expiration, causing the puts to expire in the money. The puts act as downside insurance to limit losses.

However, if the stock rises above the call strike at expiration, the calls expire in the money. The investor is sometimes assigned and obligated to sell their stock at the call strike, capping the upside return.

Between the put and call strike prices, the investor profits from stock gains but is protected from losses below the put strike.

What is the importance of the Collar Options Strategy in Options Trading?

The main importance of a collar option strategy in options trading is downside protection. The long puts in the collar act as insurance against a sharp drop in the underlying stock. By capping losses, collars help limit the impact on an investor’s portfolio if a long stock position declines rapidly. This insurance-like feature is valuable for risk-averse investors and in volatile markets. Collars allow staying invested while defining maximum loss via the protective puts.

Collars allow continued participation in upside gains up to the short call strike price. The investor retains exposure to potential stock appreciation until the call cap. This provides profit if the stock rises moderately. Collars balance, limiting losses by allowing moderate upside participation. The dual options structure shares the upside while defining downside risk.

Collars are customized based on an investor’s market outlook, risk tolerance, and return objectives. The puts and calls are structured at any strike prices. This flexibility lets traders match the collar to their specific view of where they expect the stock to trade. The range defined by the put and call strikes is sometimes widened or narrowed. The expiration dates can also be customized to match the desired holding period.

Selling calls against a long stock generates premium income. This income offsets the cost of the protective puts. Collars are often structured at zero or minimal net cost. The options income further reduces the cost basis on the stock. Revenue from the short calls enhances overall returns.

Collars allow capital efficiency by defending a stock position without liquidating. Closing the entire position requires deploying more capital. Collars let staying invested while refining risk/reward profile. The defined range of returns enhances capital efficiency relative to a naked long stock position.

Collars are sometimes used to lock in profits and hedge risks on specific stocks in an overall portfolio. Rather than hedging the entire portfolio, tailored collars on individual holdings fine-tune the risk profile stock-by-stock. This tactical flexibility makes collars a precision hedging instrument.

For investors with concentrated stock positions or limited holdings, collars help prudently manage risk. Collars allow for maintaining the core position while moderating chance. This caters well to concentrated stock owners reluctant to sell outright.

How does the Collar Options Strategy work?

A collar option strategy is created by purchasing an out-of-the-money put option to hedge downside risk while simultaneously selling an out-of-the-money call option above the current stock price to offset the set cost.

The put strike is selected below the market price to provide downside protection in the event of a price decline. The further out of the money the placed strike, the lower the premium cost since there is a reduced probability it will be in the money at expiration.

The call is sold at a strike above the current market price to generate income to cover the purchase outlay. The higher the call strike relative to market price, the less premium payment is collected since the option is deeper out-of-the-money.

Balancing the put protection level and call premium collection is the key to constructing an efficient collar. The trader seeks an optimum cost/benefit balance point based on risk tolerance and market outlook.

The collar strategy functions in the following way once it is in place. The put finishes in the money and exercises to sell the stock at the higher put strike price if the underlying stock price declines below the put strike by expiration. This limits the downside loss on the position. The max loss is capped at the original stock purchase price less the placed strike, minus the call premium received.

The call is assigned, and the stock is called away at the lower call strike price if the stock climbs over the call strike at expiration. Upside profit is then capped at the call strike less the original purchase price plus the put and call premium.

Both options expire worthless if the stock is between the put and call strikes (collar range) at expiration. The trader keeps the premium income and continues holding the stock. After that, the collar might be extended to a new expiry cycle.

How commonly do traders use the Collar Options Strategy?

The collar options strategy is widely used among traders, with collars among the most popular multi-leg option spreads. Traders that use collar methods fall into one of 10 categories based on the advantages and rewards the structure offers.

Long-term value investors who buy and hold stocks for months or years often use collar strategies. By locking in profits and limiting the downside, collars allow value investors to protect paper gains without selling quality positions. The reduced cost of protection appeals to their focus on reducing expenses. Collars support their patient, a fundamental approach.

Income-focused traders like collars because they generate upfront premium income from short call options to offset long put costs. This income contribution provides an attractive options yield. Plus, income traders appreciate the regular cash flow potential from rolling collar strategies over time.

Less sophisticated retail traders are drawn to collars because the strategy clearly defines risk, is straightforward to implement, and does not require advanced options knowledge. The capped upside and downside within known limits appeal to retail traders looking to manage risk.

Since collars allow participating in some continued upside, they are ideal for moderately bullish outlooks. Traders who are optimistic but expect limited further upside use collars to lock in existing gains while still profiting to a defined upper level.

By shorting call options, collar traders benefit from time decay as volatility reverts lower. Volatility sellers like using collars to profit from overstated implied volatility compared to realized volatility. The short call premium provides theta decay profits.

How to Use the Collar Options Strategy in Trading?

Implementing a collar options trade involves key steps to ensure the structure properly balances downside protection and cost efficiency based on market conditions and risk tolerance.

Isolate the existing long stock position you wish to collar as a hedge against downside risk. This sometimes is an individual stock or ETF position or a broad market index or sector ETF to hedge a portfolio. Determine the current price, purchase price, and total value of the position.

Form an outlook on whether you expect the stock or sector to trade in a range, exhibit a moderate uptrend, or decline over the desired collar period. Your market bias will inform the construction of an optimal collar. Consider alternatives to collars which limit the upside if very bullish.

Decide on your acceptable risk tolerance – are you willing to forego all gains above a certain level to implement a zero-cost collar? Or will you pay a debit to structure a collar that provides upside potential to a higher price? Know your risk comfort zone.

Determine the protective put strike, which sets the level of the downside cushion. Balance the necessary level of protection and the premium cost. Deeper OTM costs less but provides less protection. Select a strike reflecting your maximum acceptable loss.

Reconsider the trade-off between earning call premium revenue and restricting the upside for the call strike. A higher strike retains more potential profit but collects less call premium to offset put costs. A lower strike maximizes premium income but severely limits gains. Balance this tradeoff.

Consider logging into the long put and short call separately to optimize entry points instead of simultaneously initiating the collar. For example, first buy the put, then wait for a bounce to sell the ring.

Calculate total debit or credit, including commissions. Estimate maximum upside/downside within the collar range to quantify risk/reward. Understand margin requirements for the short call, typically 20% of stock value.

Adjust the collar structure proactively over time by rolling down the put strike to safeguard gains if the stock falls or widening the call strike on strength. Monitor time decay on short calls. Close out the collar early if needed.

Consider closing the entire trade if it is getting close to the call strike as the collar expiry draws closer to see whether you profit from doing so. Or repurchase the call to continue holding the stock. Manage assignment risk on the rings.

Roll the collar before it expires to keep the hedge in place. To do this, close the existing collar and establish a new one with better strikes and a later expiration. This extends the collar’s protection period.

Collars allow experienced options traders to balance risk versus reward prudently. However, proper construction, management and adaptation to changing conditions are vital to maximize the strategy’s effectiveness. Prudent investors and risk managers play a valuable role when they apply collars optimally.

When to enter a Collar Options Strategy?

One of the best times to collar a long stock position is when it has appreciated to a price level you are comfortable taking profits on. It indicates advantageous levels at which to put a called strike to lock in profits if a stock has reached a target price, technical resistance, or price ceiling within its valuation range.

Strong rising momentum in a long stock position sometimes signals limited further upside if the company stalls and moves sideways. The slowing momentum flags muted further gains, making it appropriate to limit upside potential via a collar while retaining some additional profit potential.

Technical indicators such as RSI above 70 or a peak in a stochastics oscillator reflect overbought conditions, signalling limited further upside. Short-term overbought readings flag a stock is ripe for a pullback, an opportune time to implement a collar to protect profits from the run-up.

A drop in implied volatility increases options affordability. Declining IV reduces premium costs for downside protection and raises short-call premium income. Lower volatility environments present attractive collar entry points.

Turning neutral to moderately bullish on a long stock position after a meaningful advance hints additional material gains are sometimes limited. A muted outlook optimizes collar use where further upside exists, but significant other improvements appear unlikely.

Collaring a stock ahead of a pending earnings report defines risk through the binary event. The collar locks in profits and limits the downside in case of an adverse earnings reaction.

Before a scheduled stock dividend payout is favourable for collaring, the pending dividend raises call premiums, increasing income. Collaring also protects against a stock decline after the dividend.

For stocks with significant embedded capital gains, a collar is implemented at any time to lock in profits while deferring taxes gradually. This allows managing taxes on the profitable position.

On the other hand, prematurely implementing a collar reduces profit potential and be suboptimal if timed poorly.

Collaring at unfavourable entry points wastes upside potential and incurs unnecessary hedging costs. Traders must avoid collaring too soon on stocks still exhibiting upward solid momentum and positive fundamentals.

When to Exit a Collar Options Strategy?

Determining the optimal exit timing is a key element of successfully trading collar options spreads. With collar positions, there are clear indications of when to exit and the possible repercussions of doing so early or late.

Before expiry, if the price of the underlying stock rises sharply above the call strike, it implies that the short calls are likely to be assigned, capping any potential profits. Exiting the entire collar position at this point allows capturing the maximum profits.

Conversely, if the stock drops below the protective put strike, it indicates the puts are in the money and will be exercised to exit the stock position. Exiting the total collar trade ultimately locks in the hedged downside protection.

As expiration approaches, time decay will rapidly erode the remaining premium on the short-call options. With two weeks left until expiration, exiting the options enables catching the accelerated theta decay if the stock is below the call strike.

A sharp increase in volatility will disproportionately increase the value of the extended put options as fear rises. Exiting the long puts to take profits on volatility spikes provides an opportunity to capture swelling set premiums.

Rolling the entire collar structure to a new expiration cycle resets the protection period while collecting additional call premiums on the next series. This exit captures profits while extending the hedge.

The fundamental outlook for the underlying company supports an early collar exit to enable greater upside participation if it significantly improves. Exit collar is very bullish on stock again.

What is the maximum loss for the Collar Options Strategy?

The maximum loss on a collar options position is capped at the long put strike price. The purchased protective puts define risk by allowing the stock to be sold at the put strike if it declines below that level at expiration.

The long put strike price represents the maximum loss point on the collar structure. The put option essentially acts as downside insurance on the stock position.

No matter how far below the put strike the stock drops, the collar strategy loss is limited to the put’s strike price minus the original net premium paid to establish the position.

The strike distance below the market price when the collar is initiated determines the strategy’s defined downside. A wider strike distance from the market equals a more significant maximum loss.

For example, if a put strike of Rs. 45 is chosen when the stock trades at Rs. 50, the maximum downside on the collar is the Rs. 45 put strike minus the net premium paid.

This fixed defined loss is known at the outset when establishing the collar and represents the total risk if the stock expires worthless.

The strike selection directly sets the risk parameters for the collar trade. The further OTM the put strike is chosen relative to market price, the wider the maximum loss limit becomes.

More aggressive put strike distances reflecting greater downside cushion raise the potential loss on the collar. More conservative, closer-to-the-money put strikes reduce maximum loss.

The strike sometimes aligns with technical support levels below the market to match risk tolerance.

The net premium paid or received to establish the collar also affects max loss. Net credit collars reduce maximum risk. Net debit collars increase risk.

For a net Rs. 0 cost collar, no premium offsets the max loss, which remains the selected put strike.

The combination of put strike selection plus net collar premium shapes the total maximum loss under the strategy.

The unrealized max loss defined by the put strike becomes an actualized loss if the stock expires below the placed strike at expiration.

In this scenario, the puts expire in the money (ITM), and the collar owner sells the stock at the advantageous put strike to capture the hedge.

Upside call options expire worthless, imposing no obligation. The ITM puts are exercised to sell the stock to limit losses.

Collars limit but don’t eliminate losses. However, defining maximum loss provides critical downside risk management.

What is the maximum profit for the Collar Options Strategy?

The maximum profit for a collar options position is capped at the short call strike price. The written calls define upside profits by obligating the sale of the stock at the call strike if it rises above that level at expiration.

The short call strike price represents the maximum profit point for the collar structure. By writing covered calls against the long stock, the upside is capped at the call strike less the premium paid for the protective puts.

No matter how far above the call strike the stock rises, the collar strategy profit is limited to the call strike price minus the original net debit to establish the position.

The call strike selection relative to market price when initiating the collar determines the strategy’s defined upside. Lower call strike distance equals a smaller maximum profit.

For example, if a call strike of Rs. 55 is chosen when stock trades for Rs. 50, the maximum upside profit is Rs. 55 call strike minus the net premium paid.

This fixed capped profit is known at the outset when putting on the collar and represents the total potential gain if stock expires at the call strike.

The call strike selection directly customizes profit potential for the collar position. The closer-to-the-money the call strike is chosen, the narrower the maximum profit.

More aggressive call strikes with greater upside cushion raise possible profits on the collar before gains are capped. More conservative higher call strikes limit profit.

The call is sometimes aligned with technical resistance to match profit objectives.

The net premium paid or received when establishing the collar also affects maximum profit. Net credit collars increase capped profit potential. Net debit collars reduce the maximum gain.

For a net Rs. 0 zero cost collar, no premium impact exists – maximum profit remains the call strike alone.

The interplay of call strike plus the net premium paid shapes the total capped upside for the collar strategy.

What is the most Appropriate market forecast for the Collar Options Strategy?

The collar options strategy is most appropriate and optimally utilized when traders have a neutral to moderately bullish market outlook on the underlying stock. A range bound to modestly upward bias allows for maximizing the effectiveness of the collar structure.

A collar involves owning the underlying stock, selling covered calls against that long position, and buying protective puts. Any of the aforementioned situations warrant this tactic.

There is an expectation for the stock to experience limited upside, making selling calls against the position suitable for income without necessarily capping substantial further gains.

Some additional upside is anticipated, making the collar preferable to buying protective puts alone, which would not allow participating in any strength.

There is uncertainty or volatility anticipated, making long puts desirable for hedging and protection against any sharp declines.

Essentially, neutral to mildly bullish conditions present an ideal backdrop to use collars to generate income from call writing while retaining upside exposure – yet also being protected on the downside with long puts.

How does implied volatility affect the Collar Options Strategy?

Rising implied volatility increases the premiums of both puts and calls. This widens the net cost of new collar positions, requiring a greater call strike distance above market to fund the puts.

Higher IV inflates the price of protective puts. It also lifts call premiums, enabling a higher upside cap via the call strikes to counter the put cost.

The inflated option costs widen the collar range between put and call strikes when the IV is elevated.

The extra premium spent on the protective puts provides a larger downside cushion when volatility spikes. The puts become more valuable if the stock drops rapidly.

The further OTM long puts have more extrinsic time value priced into their elevated premiums during periods of high IV.

This enhances the hedge provided against sudden downside moves in the stock. The intrinsic value of the puts increases if the stock falls hard.

The flip side is periods of surging implied volatility that sometimes overstates the degree of downside risk. Volatility-driven pricing builds in larger prospective risk.

This sometimes results in an overly bearish put strike being selected during spike IV environments. The perceived risk is exaggerated.

The puts become overpriced relative to downside risk if actual volatility comes back down. Positioned collars are sometimes distorted by high IV.

Conversely, declining IV reduces option premium expense. The puts required for downside protection become cheaper to purchase.

Lower call premiums also mean less upside needs to be sacrificed to generate premium income.

The tighter premiums compress the distance between put and call strike prices on new collars when IV falls.

How do traders break even with the Collar Options Strategy?

Collar options strategies aim to reach breakeven at expiration when the underlying stock price finishes within the range between the put and call strike prices. The put and call strikes are intentionally selected to produce a net zero-cost collar structure. Here is a description of how collar trade break-even points operate.

The most straightforward approach is establishing collars for zero or negligible net premium outlay. This equals the call premium collected minus the put premium paid.

At a net zero collar cost, the strategy achieves breakeven at any stock price between the put and call strikes at expiration. The entire collar range is profitable.

The even put/call premium values create a costless hedge position with zero cash outlay.

To attain the zero net debit, the put and call strike selections must equate to the premium values. A broader call strike distance from the market equals a more significant call premium to fund the put.

The relative put and call moneyness must balance to achieve the zero net premium objective. Online tools identify the optimal strikes.

Getting even premium values creates a breakeven collar at any expiration stock price within the call/put range.

The put and call strike distances are sometimes extended to achieve a break even if zero net premium cannot be attained.

This widens the collar range between upside and downside caps. A lower put strike increases cost funded by a higher call strike premium.

Even when the range extends, a costless hedge still has a net premium expenditure of zero.

The degree of wideness between the put and call strike prices is sometimes customized to align with risk tolerance.

A narrower collar range minimizes risk but has a more limited breakeven zone. The wider the collar distance, the greater the breakeven range between strikes.

Dialling in the optimal collar range becomes a balancing act between hedging risk and breakeven zone size.

Evolving volatility and interest rate environments affect the relative put and call premiums used to achieve breakeven collar positioning.

Active collar traders must monitor and adapt the strikes and collar size to changing conditions. What achieved breakeven initially sometimes requires rebalancing.

Adjusting collar positions by rolling the options outward before expiration is common to maintain zero net debit status.

Rolling the put and call strikes higher or lower while keeping balanced premium values extends the breakeven characteristics.

Constructing zero net debit collars through prudent put and call strike selection allows achieving breakeven at any stock price within the collar range at expiration. Adapting to changing volatility and interest rates enables persisting a breakeven collar over time.

How does the Collar Options Strategy assignment risk occur?

Time decay, or theta, has a significant effect on collar options trades. The passing of time and associated volatility erosion impact the value of the long puts and short calls used to construct collars. Understanding this time decay dynamic is crucial.

The protective puts purchased when establishing a collar have negative theta. Their value decays as expiry approaches due to declining time value.

Long puts lose value from time erosion without counteracting downward stock price movement. Put values sometimes decline even if the stock price is stable.

This put time decay is a cost collar traders must contend with. It lowers the net value of the hedge protection leg over the life of the trade.

In contrast, the covered calls sold to generate income exhibit positive theta. Their value declines as expiry nears, benefiting the collar trader.

As time passes, the short calls lose time premium value each day the stock remains below the call strike price. This erosion is a source of profit.

The favourable time decay on the short calls offsets the negative theta on the long puts. Selling calls funds the time value erosion on the protective puts.

What is the impact of Time Decay on the Collar Options Strategy?

Time decay, or theta, has a significant effect on collar options trades. The passing of time and associated volatility erosion impact the value of the long puts and short calls used to construct collars. Understanding this time decay dynamic is crucial.

Impact on Long Puts

The protective puts purchased when establishing a collar have negative theta. Their value decays as expiry approaches due to declining time value.

Long puts lose value from time erosion without counteracting downward stock price movement. Put values sometimes decline even if the stock price is stable.

This put time decay is a cost collar traders must contend with. It lowers the net value of the hedge protection leg over the life of the trade.

Impact on Short Calls

In contrast, the covered calls sold to generate income exhibit positive theta. Their value declines as expiry nears, benefiting the collar trader.

As time passes, the short calls lose time premium value each day the stock remains below the call strike price. This erosion is a source of profit.

The favourable time decay on the short calls offsets the negative theta on the long puts. Selling calls funds the time value erosion on the protective puts.

How does expiration risk affect the Collar Options Strategy’s gains and losses?

Expiration risk refers to the dynamics around a collar option trade as the structure nears the expiration date. This impending expiry impacts profitability in the following ways.

As expiry approaches, the window narrows where both the put and call on a collar expire worthless to retain the position. The range of prices where maximum gains occur if held until expiration shrinks over time.

The options terminate with no value if the stock finishes between the put and call strikes at expiry. But as expiry nears, the odds increase of breaching either strike threshold and triggering exercise. This narrows the profit potential.

Expiration risk also elevates the chance of assignment on the short call leg. Calls are assigned if they are in-the-money at expiry.

To avoid unwanted assignment capping gains, traders sometimes must repurchase closing calls at a loss as expiry nears. This cuts into potential profit.

Additionally, expiry risk means the purchased put options sometimes terminate worthless despite being costly to initiate. This protection leg is worthless if the stock closes above the placed strike at expiration.

Traders attempt to salvage put value by closing positions before expiry. But market conditions sometimes force closing puts at a loss as time decays.

To defend against negative expiration risks, astute traders proactively adjust collars as the final month approaches.

For example, rolling the call strike higher defends against unwanted assignments. Or puts are sometimes closed early to retain some of their premium value.

Making prudent adjustments helps mitigate expiration risks but usually involves additional transaction costs.

As profits accumulate or losses mount, the impending expiration creates urgency around closing positions.

Traders sometimes settle for suboptimal exits to avoid the uncertainty of final settlement at expiry. Letting option combinations expire with the stock between strikes risks losing accrued gains.

Expiry risk pressures traders to capture paper profits or cut losses before terminating the options. This sometimes results in leaving money on the table or exiting losers prematurely.

Expiration dynamics present collar traders with risks and tough decisions as expiry approaches. Careful adjustments and managing trades around this risk are key to optimizing outcomes.

What is the significance of adjusting the Collar Options Strategy?

Actively adjusting collar option spreads is critical to optimizing their effectiveness as market conditions evolve. The significance of making collar adjustments includes the following.

As the underlying stock declines, adjusting the put strike lower defends against maximum loss being realized and rolling the put-down locks in some gains from the stock’s appreciation before the decline.

The call strike is raised if the stock gains strength to increase the profit possibility over the initial upside cap. This allows benefiting from continued strength.

Widening the call strike spacing reduces the odds the short call gets assigned early if the stock rises. This avoids capped upside gains from unwanted early assignments.

As time passes, adjustments are sometimes required to keep the collar strikes equally spaced around current prices. This retains the original structure and balance.

Rolling the call strike higher when it nears the money reduces margin requirements by lowering the odds of assignment. This frees up capital.

There are four key ways traders adjust collars in response to changing conditions.

As the stock rises, the call strike is rolled up to higher prices to retain upside exposure. The put rolls down to protect accumulated gains if the stock declines.

Adjusting the distance between the put and call strikes modifies the risk-reward profile. Widening the call strike spacing retains more potential upside as the stock gains value. Put and call strikes are sometimes tightened near expiration to maximize time decay.

The put or call side is closed individually to capture profits, prevent losses, or modify the structure. For example, the call could be repurchased if further upside is expected.

Existing options are closed, and new possibilities are opened at farther-out expiration dates. This extends the collar’s protection period and resets the structure.

Proactively adjusting collars enables optimizing their profit potential as market conditions evolve over the life of the trade. Adapting the strikes, expiration dates, and overall structure is a crucial skill for successful collar traders.

Why is Hedging a Collar Options Strategy crucial to managing potential risks and losses?

Hedging a collar options position involves additional option trades to help offset and mitigate the inherent risks of the collar structure. Hedging collars is critical for eight reasons.

While the long put in a collar defines maximum loss, the additional downside remains below that level. Hedging with further out-of-the-money puts expands protection below the collar’s strike. This provides a cushion against volatile declines.

Selling calls against the stock creates assignment risk if the share price rallies quickly. Buying additional call options with higher strike prices ensures capped gains from the unwanted early assignment.

Short calls in a collar require margin coverage in case of assignment. Buying call options against the short calls reduces the odds of assignment, lowering capital requirements.

As the underlying stock appreciates, buying call options with higher strike prices locks in some gains in case of a reversal of the highs. This hedges against giving back accumulated profits.

As implied volatility rises and falls, additional long/short options are layered to hedge against volatility skew risk and keep collar exposure neutral.

Extra short option positions sold against the collar structure bring in added premium income to cushion against potential losses on the collar itself.

Without supplementary hedging, risks such as unlimited downside, volatility expansion, and assignment risk sometimes result in losses beyond the expected parameters of the collar strategy alone.

Prudent collar traders utilize additional hedging positions to cover vulnerabilities inherent in the collar structure. Hedging against identifiable risks improves risk-adjusted returns.

What is an example of a Collar Options Strategy?

Let us look at an example of a collar option strategy. Suppose a trader purchases 100 shares of XYZ stock at Rs. 50 per share, for a total cash outlay of Rs. 5,000. The stock has appreciated and currently trades at Rs. 55 per share.

The trader wants to lock in some unrealized gains from the price appreciation but also thinks there could be more upside potential in XYZ. However, the trader is worried about the stock declining rapidly if the broader market sells off.

To hedge these risks, the trader implements a collar options strategy on the XYZ position. Here are the details

Current XYZ Stock Price: Rs. 55

Purchase Price: Rs. 50

Quantity of Shares: 100

Collar Construction

Buy 1 XYZ 50 Put contract with strike Rs. 50 expiring in 6 months.

Sell 1 XYZ 60 Call contract with strike Rs. 60 expiring in 6 months.

By purchasing the Rs. 50 put contract, the trader established downside protection at their original purchase price of Rs. 50. The set option locks in the ability to sell the shares at Rs. 50 to limit losses if XYZ declines below Rs. 50 by the put expiration date.

To offset the cost of buying the protective put, the trader sells a call option at a Rs. 60 strike price, positioned above the current market value. The short call caps any additional potential upside gains if XYZ rallies above Rs. 60 within 6 months.

The Rs. 10 width between the put and call strikes defines the trader’s acceptable risk range on the position.

Assume the Rs. 50 put costs Rs. 300 in premium, while the Rs. 60 call brings in Rs. 200 in premium income. The net debit paid to establish the collar is Rs. 100.

Now, if XYZ declines to Rs. 45 in 3 months, the put triggers to exit the stock at Rs. 50. The Rs. 5 unrealized loss is cut in half to Rs. 2.50 after including the call premium income. The collar strategy effectively reduced the loss.

Or if XYZ rallies to Rs. 65 within 4 months, the call assignment will require selling the shares at Rs. 60 – locking in a Rs. 10 per share gain plus the options premium. The collar allowed benefiting from some upside while limiting risk.

This example demonstrates how a collar combines long puts and short calls to construct a range of acceptable risk/reward outcomes. The structure hedges downside exposure while permitting participation in defined upside potential.

What does a 5% Collar on a stock mean?

A 5% collar on a stock refers to implementing a protective collar options strategy using strike prices 5% away from the current market price. This structure provides a moderate cushion against downside risk while allowing some upside participation.

A 5% collar involves buying puts 5% out-of-the-money (OTM) to hedge the downside, and selling calls 5% OTM to generate premium income.

What are the Advantages of the Collar Options Strategy?

The collar options strategy offers traders compelling advantages that make it a versatile tool for managing risk on existing stock holdings. The following seven are the critical benefits of collar trading.

1.Downside Protection

The long protective puts in a collar provide insurance against losses if the underlying stock declines sharply. This limits downside risk to the selected strike price, defining maximum losses. This insurance-like feature helps hedge long stock positions from extreme drawdowns and volatility.

2. Upside Retention

While collars cap unlimited upside potential, they still allow participating in stock gains up to the short call strike price. Rather than forfeiting all upside, collars balance retaining some upside exposure with managing downside risk.

3. Customizable Strategy

Collars are customized in multiple ways to match a trader’s outlook and risk tolerance. This includes choosing wider or narrower put and call strike distances, varying expiration dates, and using ratio collars with unequal numbers of puts and calls. The flexibility supports individualized risk profiles.

4. Income Generation

Selling calls against long stock positions generates premium income. This offsets the cost of protective puts. Thoughtfully structured collars result in zero net debit or even net credit, reducing costs based on the stock position.

5. Efficient Use of Capital

Collars allow staying invested in a position rather than tying up additional capital to exit the stock. Defining risk reduces capital at risk compared to a naked long stock position. This enhances capital efficiency.

6. Precision Hedging

Rather than portfolio-level hedging, collars permit targeting protection on individual stocks. This tactical flexibility helps refine risks at the position level based on individual outlooks.

7. Tax Advantages

Collars provide some tax efficiencies compared to closing stock positions. Put and call premiums have preferential tax treatment compared to short-term stock gains when closing positions.

The ability to precisely define and reduce risk exposure while retaining upside potential makes collar trading a highly adaptable options strategy for prudent investors and traders alike. The multiple advantages support use cases across various market environments and outlooks.

Is the Collar Options Strategy profitable?

Yes, collar options transactions are sometimes profitable and have a reasonable chance of success when executed appropriately. However, collars do not generate profit under all market conditions. Here is an analysis of collar profitability.

The success rate for collar strategies is estimated to be between 60-75% when aligned with prudent position sizing, strike selection, and active management through expiration.

Collars are considered one of the more reliable and consistent option strategies, but they are not foolproof. Profitability still depends on thoughtful setup, prudent timing, and proactive adjustments.

Well-constructed collars where the put mimics the call premium have an inherently high probability of producing a winning trade at expiration.

What are the Disadvantages of the Collar Options Strategy?

Here are eight possible drawbacks of using a collar options strategy, mainly caps upside potential, time decay impacts and assignment risk.

1. Caps Upside Potential

The short-call leg of a collar limits the upside profit potential on the stock position. The call strike cap sometimes truncates sharp rallies. Upside opportunities are sometimes missed after implementing a collar.

2. Time Decay Impacts

Time decay erodes the value of the protective puts if held too long without adjustments. Longer-dated puts reduce this effect but have higher premium costs.

3. Assignment Risk

Early assignments sometimes occur if the stock rallies above the short call strike near expiration. This forces the liquidation of shares before the trader desires.

4. Requires Active Management

Collars perform best with proactive management – rolling, adjusting, or exiting to align with changing forecasts and volatility. Passive collars have lower odds of success.

5. Transaction Costs

The dynamic adjustments required sometimes result in accumulated commissions, contract fees, and bid-ask spreads, increasing costs.

6. Opportunity Cost

Capital tied up in collateral for a collar cannot be deployed elsewhere. There is always an opportunity cost when allocating money to any strategy.

7. Price Drift Outside Range

The collar structure becomes less relevant, requiring overhaul, if the stock trends far above the call strike or below the put strike.

8. Assignment Risk

Upside earnings on short calls are sometimes lost if allocated too soon. Options will become active if the strike is breached before downside losses are potentially incurred.

While collars limit both upside and downside from a long stock position, they are not a risk-free strategy. Ongoing active management and prompt adjustments are key to mitigating the disadvantages.

How risky is the Collar Options Strategy?

Collar options trades exhibit a defined and calculated risk profile when constructed prudently. However, imprudent use or improper management sometimes exposes the trader to elevated risks.

Defined maximum loss limited by the protective put strike if the stock declines below that level. Losses are quantified.

Limited upside capped by the short call strike limits participation in further gains if the stock rallies above that price.

It forecasts market direction and volatility when selecting optimal strike widths and structures. Incorrect assumptions increase risks.

Time decay erodes the value of expensive long puts while benefiting short call values, creating asymmetry.

Assignment risks require active management and adjustments to avoid forced option exercise at unfavourable prices.

Directional exposure remains if the stock finishes between strikes at expiration, requiring planning around outcomes.

Is the Collar Options Strategy a good options strategy?

Yes, the collar options strategy is generally considered a good and valuable options strategy in the right circumstances. The collar options strategy offers an effective mechanism for long-term stockholders to refine and customize the risk-reward profile of their position. By combining protective puts to hedge the downside plus covered call writing to generate income, collars provide a versatile risk management approach.

The long puts act as insurance to limit losses in the event of a sharp sell-off in the stock. This defines and reduces downside risk exposure. Simultaneously, the covered call writing element allows participating in stock upside until the short call strike price. Rather than entirely sacrificing all upside to hedge risk, collars balance retaining potential gains up to the call strike while protecting on the downside via the puts.

Is Collar Options Strategy for Beginners?

No, the collar options strategy is generally not ideal for complete beginner options traders.

Collars involve the simultaneous use of two different option legs – long puts for protection and short calls for income – on an existing stock position. Constructing, monitoring, and adjusting these positions requires knowledge of options Greeks, strike selection, risk profiling, and expiration management. As such, collar trading is better suited to intermediate or experienced options traders.

For beginners still learning the fundamentals, simpler long-only strategies like buying calls or puts alone allow focusing on understanding a single options contract behaviour. Combining two legs while managing the upside and downside introduces additional complexities that sometimes overwhelm novice traders.

New options traders also often lack experience holding short option positions, which collars entail via the covered calls. Understanding assignment risk, rolling, and closing out quick options requires practice. Beginners sometimes shy away from the obligations involved on the short-call side.

Before utilizing collars, developing a solid base in straight put and call buying, covering the basics of strike selection, time decay, volatility, and options pricing, is recommended. Then, progressing to spreads and combinations involving multiple legs makes more strategic sense.

While collars have defined and moderated risk, they still require ongoing active position management best handled once attaining trading experience. For complete beginners, starting with simpler long-only option strategies is generally more prudent to build foundational options trading skills and knowledge. Once those essentials are grasped, collars are sometimes incorporated as an intermediate strategy.

Is the Collar Options Strategy a bearish strategy?

No, the collar options strategy is not inherently a bearish options trading strategy. Collars involve holding long stock, which has bullish directional exposure while using options to refine the risk profile. As such, collars are optimally applied when moderately bullish on the stock but with some near-term uncertainty or volatility expected.

The intention is to retain the core bullish stock position longer-term while pragmatically managing risk in the interim. Implementing a collar signals some positive outlook on the stock, meriting retention rather than liquidation.

Ways Collars are Advantageous Compared to Long Straddles

Income generated from covered call writing subsidizes the cost of downside put protection. Straddles require fully paying for both long puts and calls. Defined maximum loss limited to the placed strike versus unlimited loss potential on long straddles before options expire.

Requires less dramatic volatility expansion to profit than straddles, which rely on surging volatility. Lower cost structure due to call writing income offsetting put purchase debit. Requires less precision in market direction forecasting.

What is the difference between Collar Options Strategy and Long Call Butterfly?

A collar options trade combines protective puts to hedge downside risk on a long stock position with covered calls sold against the stock to generate premium income. The put strike is below the stock purchase price while the call strike is above it to create a range of defined risks.

A long call butterfly involves a triple option combination of two short calls at a middle strike, one long call at a lower wing strike, and one long call at a higher wing strike. The structure profits from minimal stock movement with time decay. Collars have a modest bullish bias from long stock exposure between put and call strike prices. Butterflies have negligible directional bias, focused on time decay for profits rather than price movement.

Collars define maximum loss at the put strike but allow participating in upside above that level. Butterflies represent the ultimate loss at the net debit paid. Profit potential is also strictly quantified between wing strikes.

While both defined risk strategies, collars offer ongoing upside exposure with a downside hedge, whereas butterflies isolate a range of non-directional profit between strike wings funded by time decay. Their differing structures make them suited to varying market conditions and trading goals.

What is the difference between Collar Options Strategy and Short Call Butterfly?

A collar options trade combines protective puts to hedge downside risk on a long stock position with covered calls sold against the stock to generate premium income. The put strike is below the stock purchase price, while the call strike is above it to create a range of defined risks.

A short call butterfly involves a triple option combination of one long call at a middle strike, two short calls at a higher outer wing strike, and two short calls at a lower extreme wing strike. The structure profits from substantial stock movement with time decay.

Collars have a modest bullish bias from long stock exposure between put and call strike prices. Short butterflies have neutral to somewhat bearish biases, wanting significant stock movement either up or down.

Collars define maximum loss at the put strike but allow participating in upside above that level. Short butterflies represent maximum loss if the stock finishes right at the body strike at expiration.

Collars focus on defining and hedging risk on a directional long stock position. In contrast, short butterflies isolate a range of loss while benefiting from substantial bullish or bearish stock movement outside wings. Their differing structures and exposures suit them to varying market conditions and trading goals.

Share

No Comments Yet