Calendar Spread: Overview, Example, Uses, Trading Guide, P&L, Risks

Calendar spreads emerged in India during the 1990s following market liberalization but gained popularity after the NSE introduced options trading in 2001. Calendar Spread strategy involves simultaneously buying and selling options of the same type and strike price but with different expiration dates.

Indian derivatives market volume has grown exponentially, with NSE recording over ₹300 trillion in monthly options turnover by 2024. Nearly 18% of retail traders employ calendar spreads to capitalize on time decay while minimizing directional risk.

SEBI data reveals these strategies perform best during periods of moderate volatility, with typical returns ranging from 8-12% in stable market conditions. Traders increasingly adopt calendar spreads to navigate the market’s characteristic volatility.

What is a Calendar Spread?

A calendar spread involves simultaneously purchasing and selling options of identical strike prices but different expiration dates. Calendar Spread strategy is employed when traders buy longer-term options while selling shorter-term ones of the same type (calls or puts).

This strategy capitalizes on time decay differentials between the two contracts. The longer-dated option decays more slowly than the shorter-dated one, creating potential profit as expiration approaches.

Calendar spreads work effectively in range-bound markets where price movements remain limited. Traders use this strategy to generate income while maintaining a defined risk profile. The position benefits from decreasing implied volatility in the near-term option relative to the longer-term option.

How Does a Calendar Spread Work?

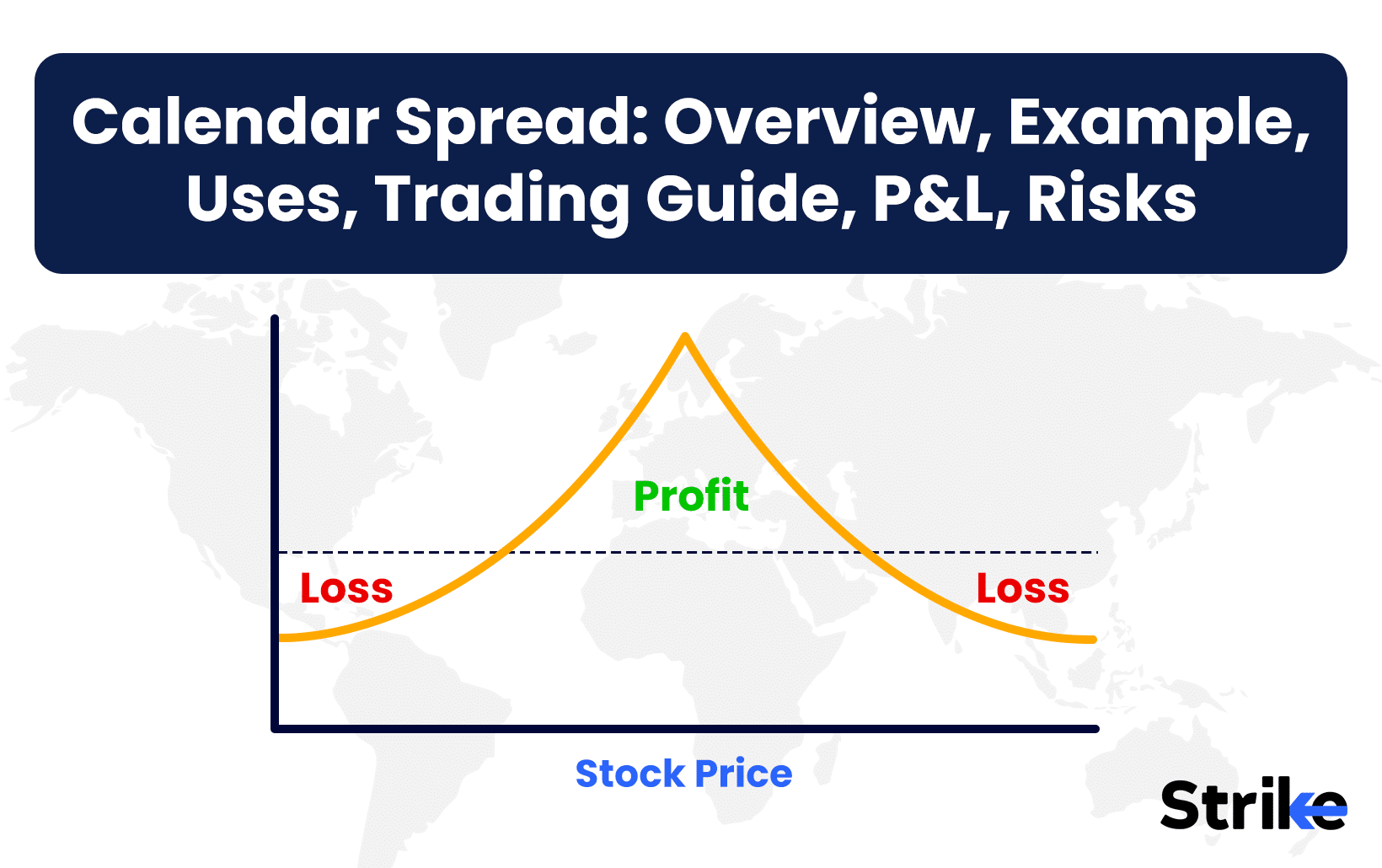

Calendar spreads work by exploiting the fundamental principle that options decay at different rates. Calendar spreads capitalize on the accelerated time decay (theta) of near-term options compared to longer-dated options, creating profit potential as expiration approaches. Look at the below image.

In the image, the profit potential is highest when the stock price stays close to the strike price at expiration of the short-term option. The green area represents potential profit, while the red areas indicate potential loss if the stock price moves significantly away from the strike price. Breakeven points occur at specific stock price levels. This strategy benefits from time decay in the short-term option while the long-term option retains its value.

Debit calendar spreads occur when traders pay a net premium, typically by buying longer-term options and selling shorter-term ones. This setup profits when the short option expires worthless while the long option retains value. Credit calendar spreads work oppositely—traders receive net premium upfront but face potentially higher risk.

Volatility impacts calendar spreads significantly. Rising implied volatility generally benefits the position by increasing the longer-term option’s value more than the shorter-term one. Traders profit when implied volatility increases after establishing the position or when it decreases more rapidly in the near-term option.

Why Use a Calendar Spread Strategy?

Traders use calender spread because it provides a way to profit from time decay differences between options contracts while maintaining a defined risk profile through strategic positioning of near-term and longer-dated options. Look at the image below.

In this chart, you will be able to see that the calendar spread’s profit potential (highlighted in yellow) is maximized when the Nifty index remains near the strike price of 18,697. The profit zone narrows as the index moves further away, with losses increasing on both sides, shown in the gray areas. This reflects the defined risk profile of the strategy.

The curved lines illustrate how the time decay differences between the near-term and longer-term options impact profitability. The strategy thrives in scenarios of minimal price movement, leveraging the faster time decay of the sold short-term option versus the purchased long-term option.

This strategic advantage allows traders to profit from deteriorating time value in the short-term option while preserving value in the longer-dated option. The trader collects premium from the rapidly decaying short option while holding a longer-dated option with slower decay.

Calendar spreads also benefit from volatility shifts. Rising implied volatility typically increases the spread’s value, as longer-term options gain more from volatility spikes than shorter-term options.

The defined risk nature of calendar spreads appeals to conservative traders. The maximum loss remains limited to the initial net debit paid, offering superior risk management compared to naked options or directional stock positions.

Many professional traders utilize calendar spreads during sideways or low-volatility market conditions to generate income while maintaining limited downside exposure.

When to Use a Calendar Spread?

Calendar spreads are best used during sideways or range-bound markets where prices trade near the selected strike price like in the below chart.

Traders implement this strategy once technical analysis indicates a consolidation phase after significant market movements.

The ideal setup occurs during periods of low implied volatility expected to increase. Low volatility reduces entry costs while subsequent volatility expansion enhances the spread’s value. Market environments preceding major announcements or economic data releases often present these conditions.

Implied volatility skew between expirations creates additional opportunities. The spread becomes particularly attractive when near-term options trade at lower implied volatility compared to longer-dated options, creating favorable pricing inefficiencies.

These spreads excel for traders with neutral short-term outlooks but expectations of future directional movement. The strategy serves as a superior alternative to cash-secured puts or covered calls during choppy market phases.

Risk-averse investors favor calendar spreads for defined-risk exposure with limited capital requirements. The maximum loss equals the initial debit paid, providing clear risk parameters.

Traders with moderate account sizes benefit from calendar spreads as capital-efficient alternatives to more complex strategies. The position requires less margin than iron condors or butterfly spreads while offering comparable risk-reward profiles.

Professional options traders often layer multiple calendar spreads across different strike prices to create position redundancy and maximize probability of profit during uncertain market conditions.

How Option Greeks Affects Calendar Spread?

Option Greeks affect calendar spreads by influencing their profitability, risk, and behavior under different market conditions, requiring traders to monitor and manage delta, theta, vega, gamma, and rho to optimize performance and minimize risks.

- Delta: Calendar spreads typically maintain near-neutral delta at inception, especially when established at-the-money. The position’s delta fluctuates as the underlying price moves away from the strike price.

Price movements create positive delta (bullish exposure) when the underlying trades below the strike and negative delta (bearish exposure) when trading above. This characteristic requires active management to maintain the intended market neutrality.

Traders monitor delta shifts closely, adjusting positions by adding complementary options once the overall delta exceeds their risk parameters.

- Theta: Theta represents the primary profit engine in calendar spreads. The shorter-term option experiences accelerated time decay compared to the longer-dated option, creating positive theta for the overall position.

This theta differential peaks approximately 30-45 days before the near-term expiration. Calendar spread profitability increases daily as this time decay differential works in the trader’s favor. Maximizing theta requires positioning the strike price at or near the current market price.

- Vega: Calendar spreads maintain positive vega exposure, meaning the position benefits from increasing implied volatility. The longer-dated option carries higher vega sensitivity than the shorter-term option, creating a net positive vega position.

Volatility expansion enhances spread value while volatility contraction reduces profitability. Traders implementing calendar spreads during low-volatility environments stand to profit from subsequent volatility increases.

- Gamma & Rho: Gamma impacts calendar spreads most significantly near the first option’s expiration date. The position experiences increasing gamma risk as expiration approaches, making the spread more sensitive to price swings. This necessitates closer monitoring and potential adjustments.

Rho affects calendar spreads minimally in short-term positions but becomes relevant for longer-duration calendar spreads spanning several months, as interest rate changes influence longer-dated option pricing more substantially than shorter-term options.

Understanding and managing the combined effects of Option Greeks is crucial for maximizing calendar spread profitability, particularly in volatile or low-interest-rate environments where strategic adjustments significantly enhance returns.

How to Trade using Calendar Spread?

To effectively trade calendar spreads, traders must focus on profiting from time decay and anticipated changes in volatility. Below are the steps to execute a calendar spread effectively.

1. Select an Underlying Stock

It is very important to understand that the stock in which a calendar spread is supposed to be traded needs to experience range-bound to mildly trendy moves near the strike price of importance.

One-sided directional moves are unexpected. That strike price could be a potential target price expectation of the stock, where the stock is likely to go. Additionally, the stock must experience an expected rise in volatility.

Traders should look for situations where implied volatility (IV) is currently low but is expected to increase due to upcoming events such as earnings announcements, RBI policy announcements, or global news. The far-expiry leg of the spread benefits the most due to its higher vega exposure.

2. Choose Strike Prices and Expiration Dates

This step defines the trade’s risk and reward. There are three possible moves a trader could expect in the chosen stock when executing a calendar spread. If the trader thinks the stock will continue to range around the last traded price (LTP), then an at-the-money (ATM) strike price is chosen to maximize benefit from time decay, expected volatility rise, and a proper consolidative price range.

Suppose the trader performs technical analysis and determines that the stock price may experience a mild trend or has potential to reach a specific price point above or below the current market price, an out-of-the-money (OTM) strike price is selected. This ensures the peak of the tent (payoff profitability) will be at the selected strike price. Deep in-the-money (ITM) or deep OTM strikes should be avoided as they offer poor risk-to-reward ratios.

In options trading, deep ITM options are often too expensive, while deep OTM options tend to have low premiums and poor sensitivity to volatility. Managing a calendar spread within options trading requires patience and careful observation of price movements, time decay of the current expiry, and shifts in implied volatility.

3. Enter the Trade and Manage the Position

In this example, a calendar spread is assumed to be set up with an expectation of mildly bullish to range-bound momentum. One critical condition to make this trade setup safe from risk is an expected rise in volatility. Volatility must rise to offset any time decay effect on the farther hedge (as in this case, a monthly hedge buy).

The vega of the monthly option helps gain some premium price, while the theta of the current expiry begins to affect the decaying premium. An unnatural gap-down opening, a strong bullish candlestick pattern, the presence of strong support, and an IV rise are four primary reasons for certifying Nifty as a suitable trade candidate.

4. Close or Adjust the Trade

In a situation where the calendar spread becomes profitable before expiry due to a rise in volatility, it is essential to consider booking profits, especially if the risk-to-reward target is met. If volatility does not rise, the value of the far-month option (bought as a hedge) will gradually decay.

This time decay erodes profitability, particularly if the short leg has already expired or lost most of its value. If the trade starts to lose money because the price moves outside the expected range, the trader must evaluate whether to exit the position or adjust it. The peak of profitability lies at the strike price where the near-expiry option expires worthless, while the far-expiry option retains time and volatility value.

In the example, the breakeven points are 22,016 and 23,050. If Nifty expires and closes below 22,016, the position will start incurring losses. Similarly, if Nifty expires and closes above 23,050, it will also start incurring losses. The position will yield maximum profit if Nifty manages to expire and close at the strike price sold, which in this case is 23,500.

This strategy works best when the underlying stock is expected to stay range-bound or move mildly towards the strike price, with an anticipated rise in implied volatility.

What is the Maximum Profit & Loss on a Calendar Spread?

The maximum profit of a calendar spread occurs when the underlying asset price is exactly at the strike price of both options at the expiration of the near-term option. At this point, the near-term option expires worthless while the longer-term option retains time value, creating optimal profit potential. This maximum profit equals the remaining value of the far-dated option minus the initial net debit paid for the spread.

The maximum loss of a calendar spread is limited to the net premium paid to establish the position. This loss materializes in extreme price movements where both options move deeply in or out of the money, eliminating the time value advantage of the longer-term option.

Breakeven points exist where the value of the remaining longer-term option equals the initial debit paid. Many traders calculate these points using options pricing models rather than simple formulas due to the time value complexities involved.

What are the Risks of Calendar Spread?

The risks of calendar spreads are volatility risk, direction risk, time decay mismatch, early assignment risk, liquidity risk, execution slippage, and capital risk.

| Risk | Description | Impact |

| Implied Volatility Changes | A sudden decrease in implied volatility erodes the time value premium of the longer-dated option more than the near-term option. Conversely, increases in volatility enhance the time premium differential between contracts. | Decrease in implied volatility damages profitability, while increases generally benefit the spread. |

| Early Assignment Risk | The short option may be assigned early, particularly with in-the-money options approaching ex-dividend dates. Counterparties exercise options to capture dividend payments. | Disrupts the strategy, incurs additional transaction costs, and eliminates the time decay advantage. |

| Capital at Risk | The maximum risk is the net debit paid to establish the position. Market conditions can sometimes cause both options to lose value simultaneously. | Loss of initial investment if both options lose value, especially during large price movements away from the strike price. |

| Large Price Movements | Significant price movements away from the strike price reduce the effectiveness of the spread. | Severely diminishes profitability by reducing the spread’s intended benefit. |

| Liquidity Constraints | Thinly traded options series can lead to difficulty in executing trades. | Bid-ask spreads may widen during market stress, increasing execution slippage and transaction costs. |

| Execution Slippage | Slippage occurs when there are delays or inefficiencies in executing entry or exit trades. | Negatively affects profitability, especially in volatile markets, where precise timing is critical. |

Is Calendar Spread Strategy Profitable?

Yes, calendar spread strategies deliver profits in specific market conditions. Traders experience optimal results during periods of moderate volatility and sideways price action. The profit mechanism relies on a time decay differential between the short-term and long-term options.

Maximum profitability occurs as the underlying price remains near the strike price at expiration of the near-term option. Many traders enhance results by selecting strikes with higher implied volatility in the near-term contracts.

Historical performance data demonstrates calendar spreads typically generate modest but consistent returns during non-trending markets. Success depends heavily on precise timing, strike selection, and volatility forecasting rather than simply predicting price direction.

Is Calendar Spread Bullish or Bearish?

Calendar spreads maintain a neutral directional bias near expiration of the front-month option. The strategy benefits most from the underlying asset trading close to the strike price as the near-term option expires. Traders modify the directional bias by selecting different strike prices relative to the current price.

Using strikes below the current price creates a bullish bias, while strikes above current price establish a bearish tilt. Many professional traders utilize calendar spreads to capitalize on volatility differentials rather than directional moves. The position transforms into a more directionally bullish trade after expiration of the front-month option, leaving only the long back-month option.

What are Alternatives to Calendar Spread Strategy?

The main alternatives to calender spread are diagonal spreads, iron condors, and vertical spreads.

Diagonal Spreads combine elements of calendar and vertical spreads, using different strikes across different expiration dates. This modification creates stronger directional bias while maintaining exposure to time decay differentials.

Iron Condors excel in sideways markets by selling both call and put credit spreads simultaneously. These strategies generate income through premium collection rather than exploiting time decay differentials.

Vertical Spreads provide more directional exposure than calendar spreads. Bull call spreads and bear put spreads target upward or downward price movements specifically. The simplified structure focuses purely on price direction rather than volatility changes or time decay optimization.

Each alternative offers distinct risk-reward profiles, addressing specific market forecasts beyond the traditional calendar spread approach.

Share

No Comments Yet