A calendar call is an options strategy that involves buying a longer-term call option while simultaneously selling a shorter-term call option with the same strike price but closer expiration. A calendar call aims to profit from volatility declines and time decay of the short-term call.

Traders purchase an ATM or slightly OTM call expiring several months out. They then write a call on the same stock or index with a nearer expiration date, usually within 4-6 weeks. As the short call expires first, it loses value faster than the long call due to theta decay. This benefits the overall position if the underlying asset moves sideways or modestly higher.

Some benefits of calendar calls include lower capital requirements compared to long-term calls alone. Time decay aids profits if volatility is low to moderate. Break-even points cover a wider price range. However, risks include unlimited losses if the stock skyrockets past the long call’s strike. Vega exposure increases if implied volatility spikes. Short calls may also be assigned early, tying up capital.

What is a Calendar Call?

A calendar call in stocks is an options trading strategy that utilizes two call options on the same underlying stock but with different expiration dates. A calendar Call involves purchasing one soon-to-expire in-the-money call and writing one longer-dated out-of-the-money call at the same strike price, creating a horizontal spread positioned to benefit as the front month call premium experiences a faster rate of time decay the closer it gets to expiration.

Executing a calendar call involves establishing two positions simultaneously – a short-term call and a longer-dated call. The nearer expiration call, known as the front Month, provides current exposure to the asset’s movements. Meanwhile, the back Month or further dated call acts as a hedge that limits risk if the stock price declines before the front month expires. This dual position structure is what gives the strategy its name, as the two expirations are separated by time or “spaced across the calendar.”

One benefit of the calendar call is that it allows for capitalizing on the expected upward movement of a stock over the near to medium term while mitigating downside risk through the Hedge of the second call. Time decay should cause the front month call to lose value faster than the back Month as expiration approaches if priced appropriately relative to implied volatility. This would result in cost basis reduction or even potential profit realization if the stock price remains range-bound or rises modestly.

However, there are some risks to be mindful of as well. Premium spent on both calls means the position requires more cash outlay upfront compared to a single long call. Furthermore, if the underlying asset moves sharply higher beyond expectations, the strategy will severely underperform a simple long call since gains are capped between the strike prices. Time decay also works against the position if the stock price fails to rise or declines substantially, eating away at the intrinsic value of both calls simultaneously.

From a theoretical pricing perspective, a calendar call resembles a horizontal calendar spread due to its dual-long call position structure. However, in practical application, it essentially acts as a temporary synthetic long stock position with upside participation capped between the strikes and protection below the lower strike via the back-month call. The key determinants of profitability revolve around the interplay between time decay outpacing any rise in implied volatility as well as proper timing relative to earnings reports or other market-moving events.

What is the Purpose of Calendar Calls?

The purpose of employing a calendar call strategy is to generate income through the systematic exploitation of options’ time decay while participating in upside stock movement. By establishing both a short-term and longer-dated long call position, the trader attempts to benefit from the faster rate of premium erosion in the front Month relative to the back Month as expiration approaches.

A calendar call structure generates positive returns in sideways or modestly rising stock environments, with downside protection also built in from the second call leg if conceived and implemented astutely. Rather than adopting a straightforward long call and hoping for a significant rally, the calendar call tactic introduces an insightful monetization element through judicious option selection. By spacing the two call expirations across consecutive months or quarters, the trader capitalizes on the unequal speeds at which theta, or time value, leeches away from options of varying maturities. Near-dated calls experience a Swiffer premium burn as the expiration clock ticks down more hastily, whereas longer-term calls see their rates of decay gradually taper off.

Skilled calendar call practitioners pinpoint this asymmetrical time dynamic between the front and back month options, astutely wagering the nearer-dated leg will depreciate faster than implied. The front call disappears into worthlessness ahead of schedule, while the subsequent call retains value if a stock trades range bound as anticipated. The result is the strategy booking an intrinsic profit just through the passage of time without needing a sustained rally. Even modest advances boost realized gains as long as moves remain within the strikes.

Meanwhile, the back month call acts as a price floor and buffer. Should adverse news send the stock tumbling before the first expiration, this hedge leg dampens losses via its continued intrinsic worth. The dual long call configuration, therefore, achieves two purposes – extracting premium decay profits while curbing downside exposure through protective put-like qualities conferred by the second option leg. Notable challenges occur if the market mood abruptly shifts or volatility spikes; hence, options with staggered maturities are selected judiciously.

For seasoned options practitioners, calendar calls provide an intriguing middle-ground approach. Compared to speculative directional plays, they impose disciplined profit objectives and risk management. Yet unlike simple covered calls, these structures allow retained upside participation past the front strikes if bullish theses materialize significantly. By preciously calibrating option deltas, gammas, and expirations to complement the trader’s market views, calendar calls represent a versatile income-generation vehicle in varying environments.

How does Calendar Call work?

A calendar call strategy involves distinct steps and components that work together like the gears of a machine. At its core, a calendar call is implemented using the following five key elements. They are given below.

Front Month Call: This is the nearer-dated long call option purchased that provides current exposure to upside stock movement. It is akin to an engine piston that combusts premium value through relentless theta burn as expiration approaches.

Back Month Call: The second and longer-dated long call acts as a protective hedge against downside risk. It functions similarly to connecting rods transmitting power from the crankshaft to keep the engine running steadily.

Strike Prices: The call options are intentionally selected at different strike prices, usually with the front Month above the back Month. This establishes zones of potential profit and loss that guide strategic calibration.

Option Expirations: Spacing the front and back call expirations one to several months apart is pivotal, as their rates of time decay necessarily diverge further out in time. This asymmetrical relationship gains.

Implied Volatility: The strategy profits most when implied volatility embedded in the front month premium erodes more rapidly than realized while remaining steady in the back Month.

Proper implementation involves selecting an underlying stock viewed as having stable near-term prospects without impending news-driven volatility. The front-month call is purchased at a higher in-the-money strike to benefit quickly from time decay. Concurrently, an out-of-the-money back month call acts as the protective Hedge.

As expiration approaches, theta steadily chips away at the front call premium. But its decline outpaces that of the back Month due to their differing maturities. This widening value differential cultivates profits, even if the stock trades sideways within the strikes.

Upon expiration, the front Month expires worthless, while the subsequent call retains intrinsic worth. Profits crystallize from the successful exploitation of disproportionate time decay. The downside is limited to strikes, with protection to the back Month helping withstand declines.

What is the strategy of Calendar Call?

The strategy behind implementing a successful calendar call rests upon the trader leveraging the asymmetric nature of options’ time decay across different expiration periods. By establishing dual long calls with staggered maturities, a calendar call aims to benefit from these uneven rates at which implied volatility erodes.

A primary strategic consideration involves selecting an underlying stock expected to trade within a stable, consolidating range over the near term. Candid selections encompass those stuck within resistance overhead or buoyed by solid support below. Names exhibiting low volatility with muted catalysts are preferable to avoid sharp, unexpected moves.

While structuring the position, the front-month call is typically purchased one to four weeks from expiration. This leg is selected further in the money to inherently gain from theta burn. Meanwhile, the back month call acts as a hedge two to six months out. It sits slightly out-of-the-money to preserve downside protection and retard decay. Strikes are consciously spaced, usually with the front above the back, setting well-defined profit and loss boundaries. The gap cannot be too vast, lest gains prove trivial or insignificant to risk unlimited exposure.

Allowing for buffers above and below current pricing cushions the trade. Ongoing management dictates rolling positions forward in a timely manner once the strategy achieves its objectives. For example, profits crystallize as the front Month expires worthless versus the live back leg. Rolling maintains upside participation while resetting exposure. Careful sizing limits overall risk to a small percentage of capital to survive potential whipsaws. Outright losses occur if volatility spikes abruptly between expiration periods. Monthly expiration avoids concentrated event risk.

What are the key components of a Calendar Call?

The key components of a calendar call strategy are establishing long call option positions on the same underlying asset with staggered expiration dates and different strike prices and systematically rolling the nearer-dated leg to maintain the staggered structure and extract gains from the time decay effects. The foundational piece is selecting an appropriate underlying stock or ETF. Candid choices exhibit low to moderate historical volatility, with technical chart levels serving as support and resistance. Names lacking significant short-term catalysts present less event risk.

Integral to the construct are the front and back call options themselves. The front Month represents the nearer-dated leg purchased one to four weeks from expiration. It provides immediate upside participation while inherently suffering accelerated theta burn. Complementing this is the back month call, constituting the second protective leg. Situated two to six months farther out, it preserves liquidity to Hedge against unexpected declines or allow trade adjustments. Its decay progresses more gently over a longer duration.

Strikes are strategically chosen, typically with the front located above the back. This delineates the maximum profit zone and forms a price range where the trade realizes gains systematically. Strikes cannot be excessively far apart to forfeit profits or leave leverage unchecked. Option expiration scheduling underpins profit extraction. Spanning calendar quarters or months separates the front and back leg life cycles sufficiently for their time decay curves to diverge prominently. This drives performance as implied volatility falters versus realized levels.

Ongoing trade management consists of rolling the position forward methodically. Once the front Month expires, closing this leg while establishing a new front month simultaneously preserves the second leg hedge. Rolling preserves the position’s asymmetric structure. Proper position sizing confines maximum risk to a small percentage of an investor’s portfolio. Outright losses occur if volatility spikes abruptly between expirations against expectations. With diversification, calendars withstand occasional short-term directional surprises.

Judicious timing of entry and rolling determines success. Initiation during low volatility environments and avoiding impending single-stock catalysts optimizes outcomes. Rolling proactively limits the downside during macroeconomic uncertainty.

1.Short Call

A short call refers to an options trading position where an investor writes or sells a call contract, taking on the obligation to deliver the underlying asset if assigned exercise. In the context of a calendar call strategy, short calls are not typically utilized. This is because the calendar call structure seeks to benefit from declines in the premium of long calls while retaining upside participation potential through multiple expiration periods.

However, in some advanced variations, traders employ short calls to augment the basic calendar call configuration. One purpose would be to generate additional income through the collection of the premium received upon initiating the short-call position. For example, an investor with an established long calendar call could identify implied volatility as being especially rich in the front Month. They will then write calls against their position to capture this inflated extrinsic value. The short calls would be struck above the calendar call’s front strikes, creating credits that boost the overall position’s profit potential. The premium adds “icing” to realized gains if the underlying asset fails to breach the elevated short strikes by expiration. But the risks are asymmetric – unlimited losses could occur if a sharp, unexpected rally ensues. Protection thus remains essential in the form of the long back month call leg.

Another potential purpose involves tactically balancing upside participation versus harvesting theta decay. Somewhat hedging the long calls via short calls could theoretically optimize returns in sideways markets by reducing dependence on significant stock price movements. This appeals to traders wanting somewhat wider breakeven thresholds around their analysis.

2.Long Call

A long-call option contract gives the buyer the right, but not the obligation, to purchase the underlying asset at a predetermined strike price by a specified expiration date. In calendar call strategies, establishing dual long call positions is integral to capitalizing on options time decay dynamics.

The primary purpose of utilizing long calls in a calendar call is to profit from the declining extrinsic value, or time premium, of the options as expiration approaches. Known as theta decay, this natural erosion in an option’s price accelerates significantly the closer it gets to expiry if no major price movements occur in the underlying asset.

By structuring the strategy with staggered long calls that expire at different points in time, an options trader systematically extracts gains as theta disproportionately impacts each leg. The front-month call, being nearer to expiry, experiences a Swiffer burn in premium, which the trader aims to monetize against the steadier decay of the further dated back-month call.

Key to this approach is the front call, which provides immediate upside participation to benefit from any stock price appreciation within its strike range. Importantly, its rate of theta decay fuels profit potential as premium is quickly chipped away through the natural passage of calendar days. This combustible front leg acts as the engine driving returns.

Simultaneously, establishing the protective back month-long call is pivotal. Situated months later, it retains robust time value while also limiting potential downside exposure through its strike. This leg cushions against losses by retaining intrinsic worth if the underlying pulls back. Its steady premium preservation hedges the overall capital at risk.

When to use a Calendar Call?

Calendar call strategies offer options traders a nuanced toolkit for multiple market environments. A prudent assessment of the underlying situation helps determine optimal deployment. Six key scenarios conducive to calendars include the following.

Range Bound Markets

Calendars extract income from the consolidation when a stock finds itself trapped within a tight price band, supported below and encountering resistance overhead. The strategy systematically monetizes theta differences, with gains accruing simply from time decay as volatility remains subdued.

Extended Uptrends

In strong bull markets, calendars provide a means for participating while also taking some “profits off the table.” The protective back leg curbs the risk of short-term turbulence, while gains from front-month premium reductions lock in a portion. Upside remains if the surge continues.

Periodic Volatility

During periods where single-stock gyrations intensify temporarily, a calendar spreads exposure across multiple weeks or months. This dilutes concentrated volatility effects that could whipsaw options with a single expiration.

Earnings Announcements

Prior to informative quarterly reports, calendars short the front expiration to avoid event risk while retaining upside views long-term via subsequent expirations. Profits bank if shares hold steady until uncertainty passes.

Consolidating Sectors

Calendars capitalize on rotations between constituents when an industry moves sideways after an extended run. Expired premium supplements portfolio returns as positions systematically roll down the volatility surface.

Low Implied Volatility

Environments where implied volatility embedded in options prices diverges meaningfully from eventual stock movements, present prime scenarios for calendars. The strategy thrives on such dislocations between implicit and realized volatility.

The versatile calendar call framework proves ideally suited for skilled options practitioners navigating varied conditions. Thoughtful application matched to environment-specific objectives optimizes chances for risk-measured performance.

How does implied volatility affect Calendar Call?

Implied volatility is critical for calendar call strategies, as the goal is for the implied volatility priced into the front-month call to decay faster than any increases in realized volatility, allowing the strategy to profit from the divergence between the two. For calendar calls to perform optimally, implied volatility embedded in the front-month call needs to decline more rapidly than any increase witnessed in actual stock movements by expiration. Put simply, if implied volatility underestimates subsequent volatility, the strategy wins. But if implied volatility overestimates realized volatility, calendars face headwinds.

This dynamic arises because changes in implied volatility bid up or down the price of an option disproportionately depending on its time to expiration. Near-dated options bouncing higher on a volatility surge suffer immense premium inflation. Meanwhile, those farther out gradually appreciate less intensely since they have longer to revert.

By establishing a front call with high embedded implied volatility ready to deflate against a back call less reactive to changes, the calendar trader leverages this asymmetry. Front premium erodes at an accelerated clip — cultivating profits from the theta decay differential versus the back leg, if implied, proves too rich initially, and the underlying behaves tamely.

However, implied volatility holding steady or increasing between expirations works against calendars. Amid higher volatility environments, both positions decay in concert, eliminating opportunities. Unexpected volatility spikes threaten losses by inflating the front call exponentially versus stable appreciation of the back leg. For this reason, calendars thrive during periods of low volatility where premiums embed a complacency discount to subsequent movements. Range Bound, consolidating markets provide the ideal implied-versus-realized volatility dislocations calendars prey upon. By carefully timing entries and avoiding single-stock news catalysts, traders optimize the odds of realizing such situations.

What precautions should traders take when using Calendar Call spreads?

The sophisticated nature of leveraging options with different expiration dates and calendar call spreads necessitates prudent risk management. Traders should take precautions such as position sizing, volatility assessment, event monitoring, appropriate strike selection, ongoing management, flexibility to make adjustments, defined exit planning, and diversification when employing calendar call spreads to manage risk and optimize performance over time.

Limit total position size to a minimal percentage of overall portfolio value to survive potential adverse moves. Never over-leverage calendars, as losses accumulate rapidly if implied volatility spikes sharply between expirations. Thoroughly evaluate the base level of implied volatility priced into options. Avoid entrada when options embed extreme “fear” assumptions, increasing downside risk if volatility simply reverts over time.

Remain cognizant of upcoming single-stock catalysts like earnings reports that could influence volatility. Do not maintain exposure across such informational releases prone to sharp reactions, positive or negative. Consider potential profit/loss breakeven thresholds around existing price levels. Select appropriate strike widths to neither forfeit gains potentials nor assume unchecked leverage if volatility increases moderately.

Roll positions proactively as expiration approaches to lock in realized gains and reset to optimized entry levels. Never maintain exposure indolently across unpredictable macroeconomic influences. Require flexibility to adapt structure by selectively closing legs if implied volatility proves stickier than expected or if underlying trends emerge. Avoid attachment to untenable views in defiance of market signals.

Predetermine circumstances triggering orderly exits, be it target profit thresholds attained, trailing stop-losses breached, or shifts in underlying technical/fundamental thesis. Execute resolutely to preserve profits.

Complement individual Calendar plays with positions spanning multiple underlying assets and expiration months to alleviate concentrated exposure influences from any single name.

How to set up a Call Calendar?

The 12 key steps to properly set up a calendar call spread strategy to benefit from time decay effects by establishing offsetting long call option positions with staggered expiration dates. They are given below.

Selecting the Underlying Asset

Carefully choose a stock, ETF, or index expected to trade within a defined range for the trade duration. Stable, low-volatility names lacking imminent catalysts work best.

Determine Entry Months

Pick the front and back month expirations, spacing 1-6 months apart. Further separations let theta differentials emerge more prominently between expirations.

Set Front Month Strike

Select an in-the-money call slightly above the current price to benefit quickly from premium erosion. Higher strikes balance gains vs costs.

Choose Back Month Strike

Set a lower out-of-the-money back month call strike, providing a downside cushion without excessive time premium.

Establish Position

Simultaneously purchase the front and back month call legs, ideally as a calendar spread to capitalize on pricing relationships.

Determine Sizing

Limit total position to a small percentage of the portfolio based on expected volume and gains. Manage risk prudently.

Set Profit/Loss Targets

Define profitable and stop loss thresholds to systematically extract gains or limit the downside if directionally incorrect.

Roll the Position

As the front Month expires, close this leg while establishing a replacement front expiry to keep the Hedge and refresh exposure.

Monitor Volatility

Track implied vs. realized volatility trends. Close early if dislocations fail to materialize or uncertainty expands considerably, contrary to expectations.

Make Adjustments

Selectively close short-dated legs if underlying trends emerge, resetting further out to preserve delta exposure.

Rebalance Expirations

Consider adjusting back a month to later expirations as time passes if viewpoints prove durable, harvesting theta across dispersed periods.

Take Profits Promptly

Remove the entire position steadily upon factors provoking exit, like technical breaks, outsized volatility, or achieving strategic objectives.

By carefully following these 12 key steps to structure, maintain, and adjust the calendar call spread position, options traders systematically benefit from the time decay effects between staggered expiration months and effectively generate returns while managing downside risk.

How to use Calendar Call?

To effectively generate returns using a calendar call spread strategy, traders should carefully analyze market environments, select suitable underlying, establish staggered positions, monitor volatility discrepancies between expirations, roll positions proactively, take partial profits, recalibrate on adjustments, trim sizes gradually, and track performance over time. To effectively implement a calendar call spread strategy, it is important to carefully follow these 11 key steps.

Analyse the Market Environment

Carefully consider the prevailing level of implied volatility, underlying price trends, and support/resistance levels. Seek low-volatility markets suitable for harvesting theta.

Select the Underlying Asset

Choose a stable, low-beta stock or ETF with defined technical boundaries and an absence of short-term catalysts.

Establish the Front Month Position

Purchase an ATM call 1-4 weeks from expiration, benefiting quickly from gamma and theta decay.

Enter the Back Month Hedge

Buy a slight Otm call 2-6 months out to provide pricing support and limit downside exposure.

Manage the Position

Monitoring volatility and price action is key. Roll fronts forward and adjust back months to maintain optimal expirations relative to evolving views.

Roll the Calendar Proactively

As expirations approach, simultaneously close expiring fronts while establishing replacement months to roll down the volatility surface in small increments over time.

Take Partial Profits Along the Way

Remove partial positions that have doubled to harvest gains and recycle capital into new opportunities while letting the remaining legs compound.

Analyse Implied vs. Realised Vol

Ensure implied volatility is declining faster than realized, fueling premium erosion. Exit promptly if dislocations fail to occur between expirations.

Recalibrate Strikes on Adjustments

Widen or tighten back month strikes as needed upon rolls to preserve ideal risk/reward given updated support/resistance levels.

Scale-Out of Positions Gradually

Trim leg sizes progressively to market or achieve objectives rather than exiting positions abruptly and risking whipsaws or leaving profits unrealized.

Record Performance Metrics

Monitor accuracy, win rates, and risk/reward profiles over time to refine strategy. Sticking closely to objectives enhances quality decisions in the long run.

Done methodically and judiciously in accordance with market conditions and one’s risk tolerance, calendars offer a prudent vehicle for generating income from volatility differentials across defined periods. Ongoing refinement further optimizes skill over the long haul.

How to Adjust a Calendar Call?

To effectively manage risk, traders should proactively adjust calendar call positions by rolling fronts forward, widening or tightening back month strikes as needed, rebalancing expiration months, gradually scaling into new positions, and being willing to close out of positions that no longer fit the market environment.

Roll the Front Month Forward

As the front Month nears expiration, simultaneously close this leg and reestablish a replacement front month call to maintain downside protection from the back leg and preserve the calendar structure.

Widen or Tighten Back Month Strikes

Upon rolls, evaluate support/resistance and adjust the back month strike accordingly to ensure it still provides an appropriate pricing buffer given updated technical levels in the underlying.

Rebalance Expiration Months

Consider advancing the back Month to a later expiration if the view remains intact, capturing additional theta between periods by shifting the hedge leg further out of the term structure.

Spray Expiration Dates

Chop up exposure across multiple fronts and back months to dilute concentrated risks and accommodate uncertainty if implied volatility starts detaching markedly from reality.

Scale Into New Positions Gradually

While re-establishing positions via rolls, scale in incrementally over sessions to dollar cost average entry levels rather than risking all capital on a single price level vulnerable to whipsaws.

Flatten Strikes on Extended Trends

Should a breakout transpire, flatten the Calendar by tightening strikes on front and back legs to track the trend at a measured pace without making an outright directional bet.

Adjust Net Delta Exposure

Selectively close or roll short-dated fronts to alter aggregate position delta if underlying directionality strengthens counter to initial range assumptions.

Alter Position Sizing

Consider trimming sizes during periods of intensifying volatility to obey risk constraints and preserve profits already accumulated versus oversized potential drawdowns.

Close for Loss and Reevaluate

Acknowledge error by exiting positions, minimizing downside rather than stubbornly clinging to invalidated theses if volatility refuses to decline as anticipated and the range idea distorts.

Upon complete liquidations, recycle profits efficiently into new investment opportunities better aligned with updated market conditions revealed through consistent fundamental and technical reappraisals.

What are the advantages of using Calendar Call?

The Calendar calls spread strategy provides nine key advantages for options traders seeking to generate returns by exploiting time decay effects between staggered expiration months. They are given below.

Limited Downside Exposure

The long back month leg acts as a hedge, providing intrinsic value preservation even if the underlying pulls back sharply. This cushions losses versus naked calls.

Participation in Upside Moves

Should the underlying rally meaningfully beyond strikes, calendars still benefit via appreciation of both legs within their premium capture range limits.

Opportunity for Multiple Expiration Gains

By harvesting theta decay across staggered expirations, calendars offer avenues to systematically generate profits every Month through small but consistent volatility dislocations.

Implied Volatility Harvesting

Calendar trades enjoy what is frequently a one-way bleed in premiums as the market correction plays out when timed well into periods of rich option pricing.

Modest Capital Requirements

Calendars are capital efficient, requiring smaller outlays relative to deltas achieved within a price range versus buying outright calls with equivalent exposure.

Lower Margin Needs

Limited risk profiles mean calendars necessitate narrower collateral levels than naked call plays or spreads lacking hedging properties.

Income Generation

By methodically rolling positions over durations as theta premium is drained, calendars potentially throw off high annualized yields scaled prudently across underlying.

Volatility Agnostic

Absent extreme shocks, calendars hold the potential to profit regardless of whether actual volatility materializes as high, low, or between implied assumptions over the structure’s lifespan.

Flexibility

Advanced traders tactically incorporate short options to monetize additional levels or alter deltas through overlays, dynamically tailoring risk/reward mixes.

These strengths make calendars an attractive framework for systematic earnings via options decay in myriad environments when sizing remains prudent relative to an individual’s goals and risk guidelines.

What are the Disadvantages of Using Calendar Calls?

While the calendar call spread strategy provides advantages, options traders must also be aware of several potential disadvantages when utilizing this approach. Eight disadvantages are given below.

Capped Upside Potential

While retaining limited appreciation exposure beyond strikes, Calendar calls profit primarily from time decay, not directional stock movements. Steep rallies leave profits unrealized versus outright long calls.

Volatility Risks

Sharp spikes in implied or realized volatility quickly erase gains if they occur between expiration periods. Calendars require calm markets to extract consistent income from theta differentials.

Rolling Expenses

Frequent adjustments like rolling front legs incur additional trading fees and commissions that detract directly from profits. These costs compound over strategies with high turnover profiles.

Undefined Risk Parameters

Unlike defined-risk vertical spreads, calendars speculatively sell puts and expose capital to black swan moves far out of the expected range. Proper collateralization is paramount.

Mathematical Edge Pressure

As the options market efficiently prices in the calendar effect, the implied volatility skew narrows, reducing profitable dislocations for harvesting premiums via this method over the long run.

Dependent on Skillful Execution

Succeeding demands accurately timing entries relative to volatility regimes, exciting positions that distort versus plans, and keenly monitoring conditions inhibiting gains like event-driven surprises.

Concentration Peril

Maintaining sizable exposures within individual underlying increases vulnerability to stock-specific risks that singularly threaten broader portfolio performance if unraveling adversely.

Liquidity Constrained

Certain low-float stocks, ETFs, and infrequently traded options contracts limit the ability to implement, adjust, and close positions efficiently on demand, increasing transaction costs.

While offering benefits, calendar call traders are wise to remain cognizant of inherent limitations and risks described if pursuing these strategies prudently aligned with their skills and risk preferences over the long haul.

What are the examples of Calendar Calls?

Let’s imagine an options trader who believes the stock of Tech Giant Inc. (TGI) will remain range-bound between Rs. 120 and Rs.130 for the next six months. Currently trading at Rs.125, implied volatility is relatively low at 30%.

The trader establishes a long calendar call with the specifications which are given below.

Front Month Position = Buy 1 TGI June Rs.125 call for Rs.3 premium.

Back Month Hedge = Buy 1 TGI January Rs.122.50 call for Rs.5 premium.

Net Debit to open the position = Rs.3 – Rs.5 = Rs.2

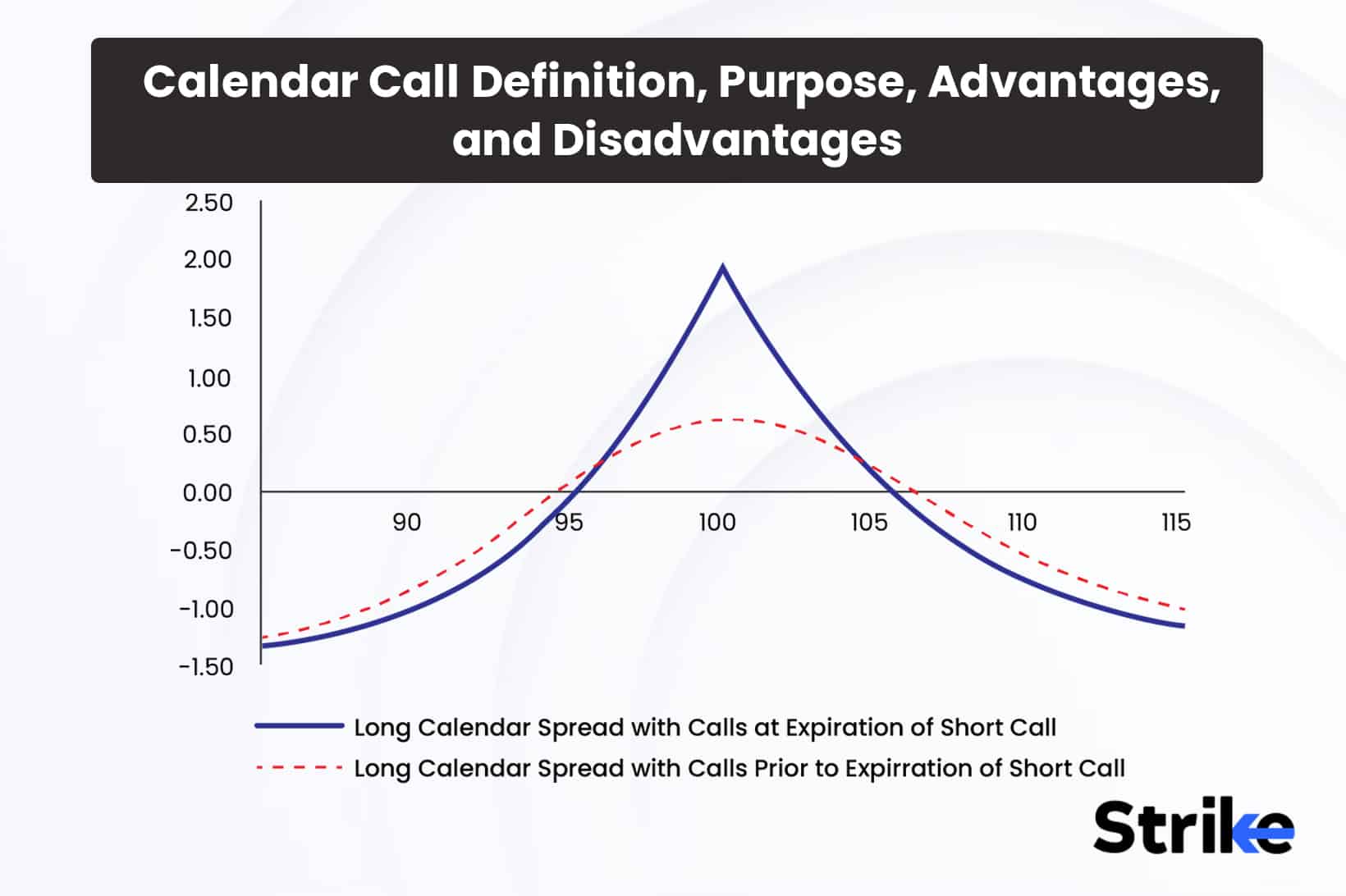

Over the next month, if TGI continues consolidating between Rs.120-130 without any volatility spikes, several outcomes could occur for the calendar call spread position, like the following.

The June call premium decays fully to Rs.1 as expiration nears. In this scenario, the trader would realize maximum gains of Rs.2 as the front leg expires worthless.

Implied volatility for TGI declined over the period to 25%, causing the June call premium to reduce to Rs.1.50 by expiration. Here, the trade generates a profitable outcome of Rs.0.50.

TGI could move higher within the range of Rs.128 by the June expiration. In this case, the position would be worth Rs.3 for the June call and Rs.6 for the protective January call, reflecting total realized gains of Rs.4.

As the June expiration approaches, the trader would follow protocol by closing the front leg and simultaneously purchasing a new June Rs.125 call to roll the position forward. This preserves the strategic structure and hedging properties of the Calendar spread by maintaining the further dated January call.

By systematically repeating this process of harvesting theta decay between the staggered expirations, the calendar call positions the trader to profit in an outright directionally neutral manner solely from volatile decay, capping the downside through the back-leg Hedge.

When to enter a Calendar Call?

One of the most important considerations for entering a calendar call is the level of implied volatility priced into the options on the underlying asset. Calendar spreads are best initiated when implied volatility is relatively low, as this presents the ideal environment for profits by harvesting declining volatility over time.

Looking for implied volatility in the bottom half of its 52-week range or even lower indicates options are embedding a complacency discount to expected price movements in the near future. Such low volatility regimes have historically proven conducive to calendar success since the embedded “fear” priced by implied volatility often exceeds eventually realised volatility.

Beyond implied volatility readings, additionally assessing technical chart levels helps to identify the quality of entry periods. Finding an underlying stock bouncing tightly between well-defined support and resistance control points increases the probability of a consolidating, range-bound market. Ranges supply the stable environment calendars require to profit reliably.

It is also prudent to analyze option volume and open interest trends. Spikes hint at increasing selling pressure, which could fuel declining prices and premiums. Entering premium thick volumes keeps traders from catching falling knives with poor liquidity. Fading such momentum allows buying options to be cheaper.

Fundamental developments should also be considered—avoid initiating during earnings weeks with high event risk. The aftermath of earnings or economic data exhibits heightened volatility that is counterproductive to calendars. Patience preserves capital for optimal opportunities.

When to exit Calendar Call?

Calendar call spreads should be excited when the underlying breaks out of its expected range, implied volatility spikes unexpectedly, position expirations are approaching, fundamental company news is pending, maximum profit targets are reached, ranges are widening markedly, or broader market corrections are unfolding.

A second exit scenario involves sharp unforeseen increases in implied volatility. Sudden “fear” spikes embedded between expiration periods swiftly inflate option premiums, overshadowing the strategy’s fundamental aim of harvesting declining volatility over time. It’s prudent to exit promptly before volatility bolts higher. Situations with expirations approaching also dictate timely exits. Proactively rolling positions lock in realized theta gains and reset the structure to fresh volatility levels. However, failure to exit incautiously risks givebacks as the premium vanishes into expiration without adjustment.

Fundamental company news likewise triggers prudent exits. Surprise earnings, M&A activity, and regulatory issues introduce event risk better avoided by removing exposure prior to the release. Post-announcement volatility surged adversely. Crossing profit targets also rationalizes exits. Upon doubling initial outlays, partially harvesting gains takes precedence over notions of further potential. What’s won is secured, freeing capital for new trades.

Range expansions widening the width between support and resistance testify to increasing uncertainty; rather than stubbornly insisting on still tighter expected boundaries, reducing sizes accommodates the unclear landscape. The market corrections are endangering the broader portfolio merit prioritizing preservation. Narrowing or closing positions prevents calendar drawdowns from compounding downward shocks.

Systematic presets like maximum time horizons or intra-month volatility spikes rounding out ranges also mandate timely reevaluations and exits consistent with the plan. Adhering to disciplined processes optimizes outcomes.

Is using Calendar Calls risky?

Yes, implementing calendar call spreads does carry certain risks when utilizing stocks as the underlying asset. While these strategies are designed to profit from options premium decay across expiration periods, unexpected volatility or market moves jeopardize those aims. A few key risks options traders should be aware of include:

What is the difference between Calendar Call and Vertical call?

Calendar call spreads involve two call options with different expiration dates but the same strike price. One leg expires soon, while a second leg expires later. They benefit from changing volatility between expiration periods. Vertical call spreads use two calls that expire at the same time but have different strike prices. The goal is to capitalize on the pricing relationship between the two strikes converging over time.

Calendar spreads have unlimited risk due to selling naked options. Verticals are defined as risk since both ends are covered. Risk is limited to the net premium paid. Calendars profit primarily from theta decay, limited to strike widths where the verticals profit depending on expiration pricing vs. strikes, allowing greater gains within the range. Calendars rely strongly on declining volatility materializing between expirations.

Verticals are less sensitive since both legs react similarly to implied vol changes at the same expiration. Calendars require frequent rolling to harvest gains and reset exposures. Verticals typically remain static until expiration for defined profit capture. Calendars exploit volatility term structure differences by holding multiple expirations. Verticals leverage a singular volatility surface for the expiration date used.

Previous Article

Previous Article

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 40")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 41")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 42")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 46")

No Comments Yet.