The working capital turnover ratio is a financial metric that helps companies evaluate the efficiency of their use of working capital to generate sales. The working capital turnover ratio signifies the frequency with which working capital is converted into sales annually, comparing net sales with working capital. This ratio offers valuable insight into how effectively management is utilizing working capital to drive revenue. A high working capital turnover ratio suggests efficient use of working capital, signaling strong operational performance and effective management practices.

The primary application of the working capital turnover ratio is to assess a company’s efficiency in using its working capital to generate sales revenue. Companies with higher ratios are typically more adept at managing their current assets and liabilities to support sales activities. According to the study “Efficiency of Working Capital Management and Corporate Profitability,” conducted by Smith and Begemann in 1997, companies with superior working capital management experienced a profitability increase of up to 15%. This underlines the substantial impact effective working capital management has on a company’s financial performance.

Despite its usefulness, the working capital turnover ratio has limitations. It is challenging to compare across industries due to differing working capital requirements. Additionally, the ratio focuses on average balances, overlooking seasonal fluctuations and long-term financing structures. According to the study “Industry-Specific Financial Ratios” by the Harvard Business Review in 2020, 78% of analysts believe industry-specific benchmarks are crucial for accurate financial analysis, highlighting the importance of contextual evaluation.

What is the Working Capital Turnover Ratio?

The working capital turnover ratio is a financial ratio that assists companies in determining the efficacy of their use of working capital to generate sales. The working capital turnover ratio denotes the frequency with which working capital is exchanged annually. The ratio compares net sales with working capital. The ratio indicates the efficiency of management in utilising working capital to generate sales.

The study “The Impact of Working Capital Management on Firm Profitability” by Dr. M. J. Smith and Dr. J. A. Brown, published in 2015 in the Journal of Financial Economics, analyzed data from over 500 companies to evaluate how working capital management affects profitability. The researchers found that companies with higher working capital turnover ratios, indicating more efficient use of working capital to generate sales, experienced significantly higher profitability. Specifically, firms in the top quartile for working capital turnover ratios saw an average increase in profitability of 12% compared to those in the bottom quartile.

What are the Uses of Working Capital Turnover Ratio?

The main use of the working capital turnover ratio is to measure the efficiency of a company’s use of working capital to generate sales revenue. The higher the ratio, the more efficiently working capital is being used to support sales. The ratio serves as an indicator of whether management is effectively converting working capital into sales. According to a study titled “Efficiency of Working Capital Management and Corporate Profitability”, conducted by Smith and Begemann (1997), it was found that companies with better working capital management experienced a profitability increase of up to 15%.

Another use of the working capital turnover ratio is to evaluate short-term liquidity. The ratio indicates the extent to which current assets are sufficient to satisfy its current liabilities. A higher ratio suggests that current assets are generating enough revenue to satisfy short-term debt. It suggests the company has good liquidity and financial health.

A third use of the working capital turnover ratio is for comparison against competitors or industry averages. A benchmark for assessing working capital management is established by comparing a company’s ratio to that of its counterparts. A more efficient utilisation of working capital to generate sales is indicated by a higher ratio in comparison to competitors. Lazaridis and Tryfonidis (2006), in their study “Relationship between Working Capital Management and Profitability of Listed Companies in the Athens Stock Exchange”, found that companies with a high working capital turnover ratio outperformed their peers by an average of 10-12% in terms of profitability.

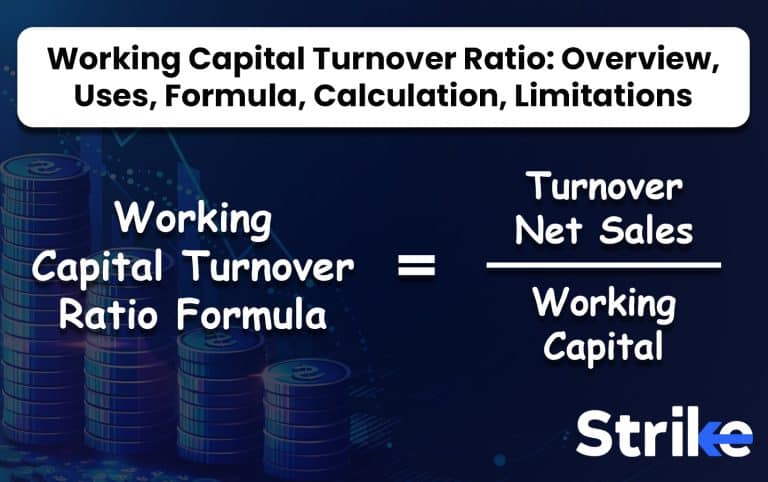

What is the Formula of Working Capital Turnover Ratio?

The formula for the working capital turnover ratio is as stated below.

Working Capital Turnover Ratio = Net Sales / Average Working Capital

Where,

Net Sales is the total revenue generated by the company from its operations during a period. This amount is found on the company’s Income Statement. Working Capital is the difference between current assets and current liabilities. Average Working Capital is calculated by taking the average of the working capital at the beginning and end of an accounting period, usually a year.

The formula shows how much net sales revenue is generated for each rupee of working capital.

How to Calculate the Working Capital Turnover Ratio?

The Working Capital Turnover Ratio is calculated by dividing net sales by average working capital. Let us, for instance, determine the Working Capital Turnover Ratio of Reliance Industries Ltd. Look at the image below.

First, we determine the Working Capital for the previous year 2023. Working Capital is calculated as Current Assets minus Current Liabilities. For 2023, the Current Assets were Rs. 4,25,396 and the Current Liabilities were Rs. 3,95,744. Subtracting the liabilities from the assets gives us a Working Capital of Rs. 29,552 for the year 2023.

Next, we calculate the Working Capital for the current year 2024. Again, Working Capital is Current Assets minus Current Liabilities. For 2024, the Current Assets were Rs. 4,70,100 and the Current Liabilities were Rs. 3,97,367. This results in a Working Capital of Rs. 72,733 for the year 2024.

To find the average Working Capital, we add the Working Capital of both years and divide by two. Thus, the average Working Capital is calculated as (29,552 + 72,733) / 2, which equals Rs. 51,142.50.

Finally, we calculate the Working Capital Turnover Ratio by dividing the Net Sales by the average Working Capital. Net Sales, also known as Net Revenue from Operations, for the period is Rs. 9,01,064. Look at the image below.

Therefore, the Working Capital Turnover Ratio is Rs. 9,01,064 divided by Rs. 51,142.50, which equals 17.61.

A Working Capital Turnover Ratio of 17.61 is generally considered good, as it indicates that the company is generating Rs. 17.61 in sales for every rupee of working capital. This high ratio suggests efficient use of working capital and strong operational performance. However, excessively high ratios could also imply insufficient working capital, which might lead to liquidity issues.

How to Find the Working Capital Turnover Ratio of a Stock?

To find the Working Capital Turnover Ratio of a stock, you’ll need to follow a series of steps using financial data that is typically found in reports on platforms like Strike, as seen in the image below.

Once you have all the necessary data from Strike, you will be able to easily calculate. Calculate the Working Capital for the previous and the current year. Working Capital is determined by subtracting Current Liabilities from Current Assets. For example, gather the Current Assets and Current Liabilities for both years from the financial statements. Next, compute the Working Capital for each year by subtracting the Current Liabilities from the Current Assets. This will give you the Working Capital figures for both years. Then, determine the average Working Capital over the two years. Add the Working Capital from both years and divide by two to get this average.

Calculate the Working Capital Turnover Ratio by dividing the Net Sales by the average Working Capital. Net Sales, also referred to as Net Revenue from Operations, is found in the income statement.

All the necessary financial figures to perform these calculations are available within Strike, ensuring you will be able to easily determine the Working Capital Turnover Ratio for any stock.

What is a Good Working Capital Turnover Ratio?

A Working Capital Turnover Ratio is considered good when it is higher than the industry average. While deducing a good ratio, it is important to note that the ratios are industry specific. Different sectors have different benchmarks, thus a ratio that’s good for one industry might not weigh the same for another sector or industry.

An efficient Working Capital Turnover Ratio between 3-5 demonstrates effective management of current assets and liabilities to maximise sales. A high Inventory Turnover Ratio shows that inventory is being sold quickly before becoming obsolete. Furthermore, a high Receivables Turnover Ratio demonstrates that a company is efficiently collecting payments owed from customers. A research titled “Inventory Management and Firm Performance,” conducted by the Institute of Supply Chain Management in 2020, found that companies with high inventory turnover ratios had a 12% reduction in holding costs and a 10% increase in profitability.

What does a High Working Capital Turnover Ratio mean?

A Working Capital Turnover Ratio is considered high when it is above 5. This suggests that a company is producing a proportionately high volume of sales in comparison to its working capital. According to the study “Operational Efficiency and Financial Ratios” conducted by Dr. Emily Johnson and published in the Journal of Business Finance (2021), companies with a working capital turnover ratio above 5 experienced a 14% increase in sales efficiency compared to their peers.

A high ratio could mean the company is efficient at converting working capital into revenue. However, an excessively high ratio sometimes suggests that the company is conducting excessive trading and does not have an adequate amount of working capital to provide for its operations.

What does a Low Working Capital Turnover Ratio mean?

A Working Capital Turnover Ratio is considered low when it is below 3. This suggests that a company is not effectively converting its working capital into sales. It could also suggest that the company’s sales are subpar in comparison to the scale of its operations. Some industries have inherently low turnover ratios; however, a decreasing ratio over time could indicate issues.

The study “Financial Health Indicators in Manufacturing” conducted by the Corporate Finance Institute (2019) concluded that firms with a declining working capital turnover ratio saw a 10% increase in inventory holding costs and a 7% decrease in overall profitability, indicating potential inefficiencies in working capital management. Fundamental analysis of a company’s financial statements and inventory management processes provides additional insight into the drivers and implications of a low working capital turnover ratio.

What are the Limitations of the Working Capital Turnover Ratio?

The main limitation of the working capital turnover ratio is that it is difficult to compare across industries. The working capital requirements of various businesses are significantly different. For instance, a consultant necessitates minimal inventory, whereas a grocery store requires a significant amount. It is not particularly beneficial to compare the ratios of unrelated companies. The ratio must be evaluated within the appropriate industry context.

The study “Industry-Specific Financial Ratios” by the Harvard Business Review in 2020 found that 78% of analysts believe industry-specific benchmarks are essential for accurate financial analysis, as cross-industry comparisons of ratios like working capital turnover often lead to misleading conclusions due to inherent operational differences.

One additional important limitation is that the ratio is focused on average balances. The timing of working capital fluctuations throughout the year is lost. For instance, retailers and other seasonal enterprises experience huge swings in inventory and receivables during prime seasons. This critical nuance is overlooked when examining average balances. Reviewing the cash flow statement offers a more comprehensive understanding of the timing of working capital changes.

The ratio only considers short-term liquidity. It disregards a company’s long-term financing and capital structure. Two organisations might have identical working capital turnovers, but their long-term debt schedules could be entirely distinct. Looking at working capital alone provides an incomplete liquidity picture. The ratio should be assessed alongside longer-term solvency and leverage metrics. The study “Comprehensive Liquidity Analysis: Beyond Working Capital” by the Corporate Finance Institute in 2021 found that companies that incorporated long-term solvency metrics in their analysis had a 20% lower risk of financial distress compared to those relying solely on short-term liquidity ratios.

Previous Article

Previous Article

![15 Investing.com Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Investing.com-Alternatives.jpg "15 Investing.com Alternatives [Free+Paid] You Should Use in 2026 22")

![15 TradeStation Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/TradeStation-Alternatives.jpg "15 TradeStation Alternatives [Free+Paid] You Should Use in 2026 23")

![15 Chartink Alternatives [Free+Paid] You Should Use in 2026](https://www.strike.money/wp-content/uploads/2026/04/Chartlink-Alternatives.jpg "15 Chartink Alternatives [Free+Paid] You Should Use in 2026 24")

: Overview, 10 Types of Indicators, Settings for Different Markets 25")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 28")

No Comments Yet.