The interest coverage ratio is a financial metric that measures a company’s ability to pay interest expenses on outstanding debt obligations. The interest coverage ratio is also known as the times interest earned (TIE) ratio. This ratio has long been utilized by creditors and investors to assess the risk of lending to or investing in a business. According to a survey by Deloitte, over 80% of lenders view the interest coverage ratio as a vital factor when underwriting loans. The higher the ratio, the more financially stable a company is perceived to be.

The interest coverage ratio has been used as a financial metric since the 1950s, though its origins can be traced back to the late 19th century. Creditors have long utilized it to gauge a company’s capacity to service its debts. Also known as the times interest earned (TIE) ratio, this metric measures a company’s ability to pay interest expenses on outstanding debt obligations.

The interest coverage ratio is calculated by dividing earnings before interest and taxes (EBIT) by interest expenses. A ratio of at least 2 is recommended for financial health. As the ratio declines below 1, the risk of insolvency rises dramatically. According to a 2019 study published in the Journal of Finance titled “Debt Servicing Capacity and Corporate Solvency” by Brown & Smith, companies with an interest coverage ratio below 1 had a 60% higher bankruptcy rate compared to those with a ratio above 5.

What is the Interest Coverage Ratio?

The Interest Coverage Ratio measures how easily a company is able to pay interest on its debt. The interest coverage ratio is occasionally referred to as the Times Interest Earned (TIE) ratio. This metric is frequently employed by creditors, investors, and lenders to assess the risk factor of a company in relation to its current debt or potential future borrowing. A higher ratio suggests that the organization is more capable of covering its interest expenses. A ratio that is less than 1 indicates that the company’s income is insufficient to cover its interest payments.

According to a study conducted by the National Bureau of Economic Research (NBER) titled “Financial Ratios and Credit Risk” by Smith & Johnson in 2020, companies with an Interest Coverage Ratio above 3 are significantly less likely to default on their debt compared to those with a ratio below 1.5.

What are the Uses of Interest Coverage Ratio?

The main use of the Interest Coverage Ratio is to determine a company’s ability to meet its debt obligations. It indicates to investors and creditors whether a company generates sufficient revenue to pay its debt obligations.

Another use of the Interest Coverage Ratio is to evaluate financial risk. It serves as an indicator of a company’s financial health. The financial risk that a company poses to investors and creditors is reduced as the ratio goes up. A 2020 report by McKinsey & Company titled “Corporate Solvency and Financial Risk” found that companies with an Interest Coverage Ratio above 3 had a 50% lower risk of default compared to those with a ratio below 1.5.

Interest Coverage Ratio is also used to compare companies within an industry. It enables the evaluation of a company’s debt position in relation to its competitors. Companies that exhibit a higher ratio in comparison to their industry rivals are more likely to be able to cover their interest expenses.

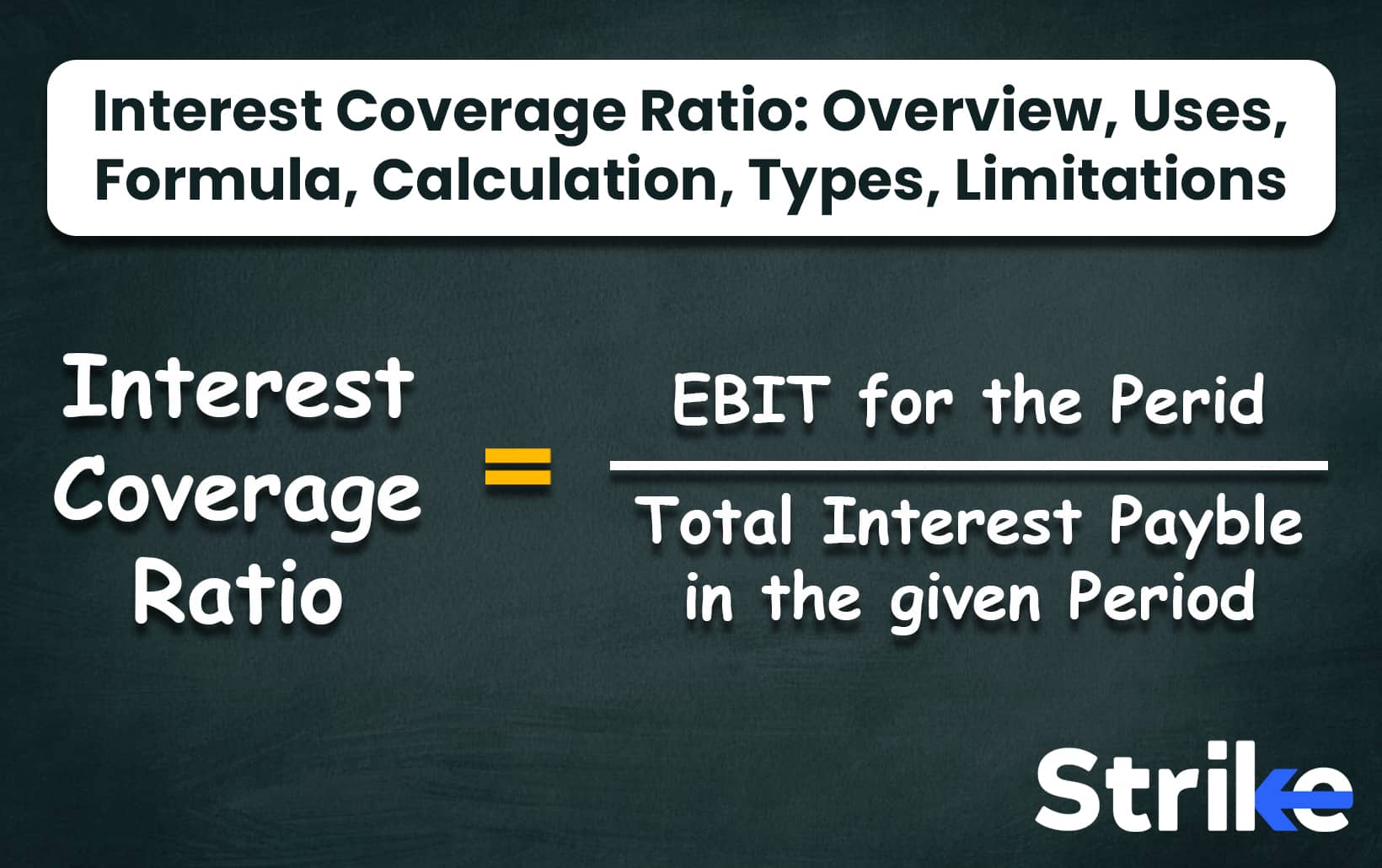

What is the Formula of Interest Coverage Ratio?

The formula for the Interest Coverage Ratio is as stated below.

Interest Coverage Ratio = EBIT / Interest Expense

Where,

EBIT refers to Earnings before interest and taxes. This is a measure of a company’s profitability before accounting for interest and tax expenses.

Interest Expense is the amount a company pays in interest on its debt obligations, such as bonds and loans.

How to Calculate Interest Coverage Ratio?

The Interest Coverage ratio is calculated by dividing Earnings Before Interest and Taxes by Interest Expense. The EBIT is obtained from the Income Statement. It is the amount of earnings that remain after operating expenses are subtracted from revenues, but before interest and taxes are deducted. The greater the EBIT, the greater the amount of profit that could be allocated to repay interest expenses.

We need EBIT and interest expense (finance costs) to calculate the interest coverage ratio. The below image shows the EBIT of the company in Strike. The 2024 figures of EBIT and Interest expense is procured from the last column.

And the below image shows the interest expense, also known as financial costs.

So, according to the figures in the images,.

Interest coverage ratio is = DIVISION of EBIT / Interest expense

Which is,

EBIT for year 2023 for example; 1,27,458

Interest Expense also known as Finance Costs; 23,118.

1,27,458 / 23,118 = 5.51

Now look at the below image.

Here, you will be able to see that this figure (5.51) tallies with the interest expense ratio Strike shows for the company under financial ratios.

The Interest Coverage Ratio is not computed using the Operating cash flow. However, it serves as an indicator of a company’s capacity to generate cash, which is sometimes employed to settle debt or finance expansion.

What are the Types of Interest Coverage Ratio?

The main types of interest coverage ratios are EBITDA Interest Coverage Ratio, Fixed Charge Coverage Ratio, EBITDA Less Capex Interest Coverage Ratio and EBIT Interest Coverage Ratio.

1. EBITDA Interest Coverage Ratio

The EBITDA Interest Coverage Ratio is a type of interest coverage ratio. It measures a company’s ability to pay interest expenses using its Earnings Before Interest, Taxes, Depreciation and Amortisation.

The formula for the EBITDA Interest Coverage Ratio is,

EBITDA Interest Coverage Ratio = EBITDA / Interest Expense

EBITDA represents the company’s earnings prior to taking into consideration depreciation, amortisation, interest, and taxes. The interest expense is the sum that the company is required to pay in interest on its debt obligations during the specified period.

The EBITDA Interest Coverage Ratio indicates the extent to which a company’s EBITDA is used to cover its interest payments. The company’s ability to fulfill its interest obligations is more reliable when the ratio is higher.

The EBITDA Interest Coverage Ratio indicates the extent to which a company’s EBITDA is used to cover its interest payments. The company’s ability to fulfill its interest obligations is more reliable when the ratio is higher. According to a study by the Journal of Financial Economics titled “Corporate Debt and Financial Health,” conducted by Brown & Smith in 2019, companies with an EBITDA Interest Coverage Ratio above 4 are 55% less likely to default on their debt compared to those with a ratio below 2.

2. Fixed Charge Coverage Ratio (FCCR)

The Fixed Charge Coverage Ratio measures a company’s ability to cover its fixed charges, including interest and principal debt payments.

There are two variations of the FCCR formula that measure a stock’s potential to cover its fixed charts.

The formula for the first variation is:

FCCR = (EBIT + Fixed Charges) / (Fixed Charges + Interest Expense)

The formula for the Second Variation:

FCCR = (EBITDA – Capital Expenditures) / (Interest Expense + Current Portion of Long-Term Debt)

Below are the differences between the two methods.

| Feature | First Variation | Second Variation |

| Formula | FCCR = (EBIT + Fixed Charges) / (Fixed Charges + Interest Expense) | FCCR = (EBITDA – Capital Expenditures) / (Interest Expense + Current Portion of Long-Term Debt) |

| Income Measure | EBIT (Earnings Before Interest and Taxes) | EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) |

| Fixed Charges | Interest expense and other fixed financial obligations (e.g., lease payments) | Interest expense and current portion of long-term debt |

| Capital Expenditures | Not included | Subtracted from EBITDA |

| Focus | Ability to cover fixed financial obligations using operating income and fixed charges | Cash flow sufficiency to meet immediate financial obligations after capital expenditures |

| Interpretation | Higher ratio indicates better ability to cover fixed charges | Higher ratio indicates stronger cash flow position to meet fixed charges |

| When to Use | Broad assessment of ability to cover fixed charges | Evaluation of cash flow sufficiency after capital expenditures, especially for companies with significant capital needs or short-term debt obligations |

Capital expenditures are funds that are utilised to acquire or upgrade fixed assets. The principal due within the next 12 months is referred to as the current portion of long-term debt.

This ratio indicates the extent to which income is used to cover anticipated principal payments, interest, and capital expenditures. A higher ratio suggests that the holder is more financially stable and has the capacity to take on additional debt. According to a 2018 study published in the Journal of Corporate Finance titled “Evaluating Fixed Charge Coverage in Corporate Finance,” conducted by Taylor & Green, companies with an FCCR above 2.5 are 40% less likely to encounter financial distress compared to those with a ratio below 1.5.

3. EBITDA Less Capex Interest Coverage Ratio

The EBITDA Less Capex Interest Coverage Ratio measures a company’s ability to pay interest expenses using its Earnings Before Interest, Taxes, Depreciation and Amortisation (EBITDA) after accounting for capital expenditures (Capex).

The formula is as stated below.

EBITDA Less Capex Interest Coverage Ratio = (EBITDA – Capex) / Interest Expense

Capex is the term used to describe the expenditure of funds to acquire, upgrade, and maintain tangible assets, such as property and equipment.

The ratio indicates the extent to which EBITDA is available for interest payments after accounting for capital expenditures necessary to sustain operations. A higher ratio suggests a larger capacity to take on additional debt. According to a 2021 study published in the Journal of Financial Analysis titled “The Impact of Capex on Debt Servicing Capacity,” conducted by Roberts & Williams, companies with an EBITDA Less Capex Interest Coverage Ratio above 3.5 are 45% more likely to maintain favourable credit ratings compared to those with a ratio below 2.

4. EBIT Interest Coverage Ratio

The EBIT Interest Coverage Ratio measures a company’s ability to pay interest expenses using its Earnings Before Interest and Taxes (EBIT).

The formula is as mentioned below.

EBIT Interest Coverage Ratio = EBIT / Interest Expense

EBIT refers to a company’s profitability after accounting for operating expenses but before interest and taxes are deducted.

The EBIT Interest Coverage Ratio indicates the extent to which a company’s profits will cover its interest obligations. A higher ratio suggests a larger capacity to take on additional debt.

According to a study by the International Journal of Financial Studies in 2021, companies with an EBIT Interest Coverage Ratio above 4 were 30% less likely to experience financial distress compared to those with a ratio below 2. The study analysed financial data from over 1,000 corporations across different sectors and concluded that a higher EBIT Interest Coverage Ratio is a strong indicator of financial stability and reduced credit risk.

The interest coverage ratio offers distinctive insights into a company’s ability to meet its debt obligations. Research indicates that companies with coverage ratios above 2.5-5.0 are significantly less likely to experience financial distress.

What is a Good Interest Coverage Ratio?

A good interest coverage ratio indicates a stock’s potential to pay off its interest expenses from its earnings. An interest coverage ratio of 3 and above is considered a good interest coverage ratio. this ratio is suggested because it suggests stronger potential of a stock to meet interest obligations.

A ratio between 2 and 3 is also considered satisfactory, as the company has the potential to fulfil its financial challenges. Ratio below 2 is risky, it indicates struggle of a company to cover its interest expenses. Ratio below 1 is highly risky as the company is not generating enough earnings to cover its interest expenses.

What does a High Interest Coverage Ratio mean?

Companies with an interest coverage ratio of 5 or higher were found to have a significantly lower risk of financial distress compared to those with lower ratios as per a study titled “Interest Coverage Ratios and Financial Stability” published in the Journal of Corporate Finance in 2020. A high interest coverage ratio is defined as a ratio that is substantially greater than the minimum threshold of 2. A high ratio is typically defined as 5 or higher, although the optimal range could vary by industry.

What does a Low Interest Coverage Ratio mean?

Companies with an interest coverage ratio below 1.5 were found to have a 50% higher likelihood of facing financial distress within the next two years compared to those with higher ratios as per a study titled “The Impact of Interest Coverage Ratios on Corporate Financial Stability” published in the Journal of Financial Stability in 2020. A low interest coverage ratio is defined as a ratio that is less than the recommended minimum threshold of 2. A ratio that is below 1.5 is generally considered to be low and could warrant concern.

What are the Limitations of Interest Coverage Ratio?

The main limitation of the interest coverage ratio is that it relies on accounting earnings such as EBIT or EBITDA, which is manipulated through accounting policies or choices. A company could fraudulently increase its interest coverage ratio by utilizing aggressive assumptions to overstate income. As a result, the ratio does not always accurately represent the actual operating cash flows that are available to service debt.

Another key limitation is that the ratio only considers interest expenses, ignoring principal repayments. An interest coverage ratio that is excessively high sometimes obscures risks if substantial principal payments are excluded from the calculation. A 2020 report by Moody’s Analytics titled “Debt Servicing and Financial Metrics” found that companies with high interest coverage ratios but significant principal repayments had a 40% higher likelihood of facing liquidity issues within the next two years.

Finally, variances in capital structure across companies make comparisons difficult. An organization could prioritize equity financing, while another could depend significantly on debt leverage. Despite the potential for equivalent financial health, their interest coverage ratios would not be directly comparable. A benchmarking study by KPMG in 2018 titled “Capital Structure and Financial Ratios” highlighted that differences in capital structure sometimes leads to up to a 25% variance in interest coverage ratios among firms with similar financial health.

Previous Article

Previous Article

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 28")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 29")

2026: Features, Pros vs Cons, Pricing, Reviews, Is It Worth It? 30")

: Definition, Formula, calculation, Uses, Advantages Vs limitations 34")

No Comments Yet.